Indexed Universal Life Insurance (IUL) offers tax-free retirement income by combining life insurance protection with S&P 500-linked growth potential and a zero-loss floor. Everence Wealth helps families leverage Index Strategies to capture market upside while protecting principal from downside risk, creating a tax-exempt income stream that never triggers required minimum distributions or impacts Social Security taxation.

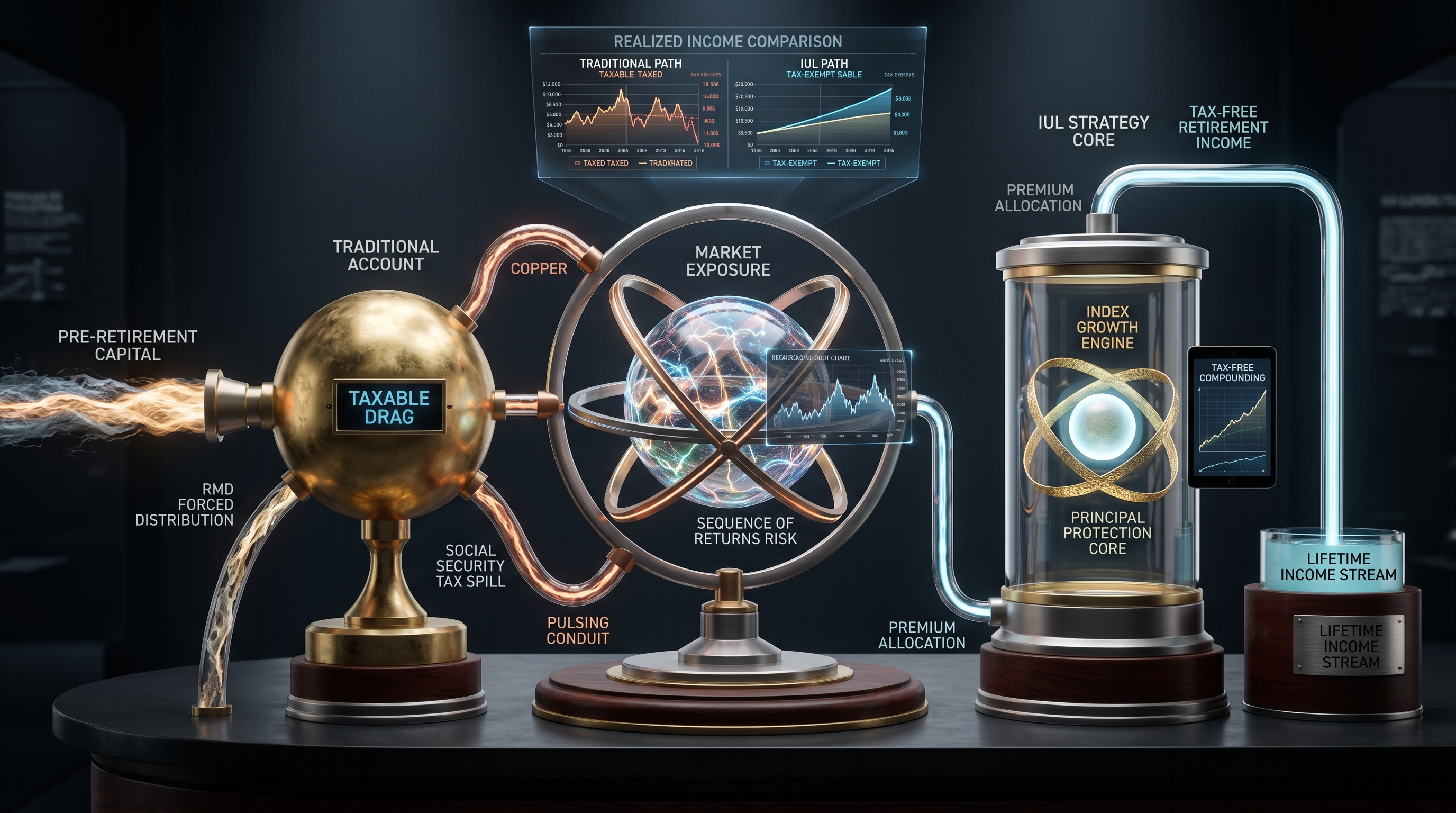

Most Americans approaching retirement discover a disturbing truth: the traditional retirement vehicles they've funded for decades come with tax obligations that erode their purchasing power precisely when they need it most. Required minimum distributions from 401(k)s and traditional IRAs force withdrawals whether you need the income or not, pushing retirees into higher tax brackets and triggering taxation on Social Security benefits. Meanwhile, market volatility in the years immediately before and after retirement—the "sequence of returns risk"—can devastate account values when recovery time has disappeared.

This dual threat of taxation and volatility has created what we call the Retirement Gap: the difference between what families expect their retirement accounts to deliver and what they actually receive after taxes, fees, and market corrections. We've seen portfolios that looked substantial on paper deliver disappointing real-world income because owners failed to account for the compounding impact of these three silent killers: fees, volatility, and taxes.

Index Strategies—properly structured Indexed Universal Life Insurance policies—address both challenges simultaneously by offering S&P 500-linked growth potential with downside protection and tax-free access to accumulated cash value. Rather than renting your wealth from Wall Street with ongoing management fees and full market exposure, Index Strategies allow you to participate in market growth while your principal remains protected from loss. You capture the upside. You're shielded from the downside. This is the foundation of the Zero is Your Hero framework.

What Is Indexed Universal Life Insurance and How Does It Function?

Indexed Universal Life Insurance is a permanent life insurance contract that links cash value growth to the performance of a market index—most commonly the S&P 500—while providing a guaranteed floor that prevents loss during market downturns. Unlike traditional universal life policies that credit a fixed interest rate, IUL policies allow policyholders to participate in index gains up to a specified cap rate, typically ranging from eight to twelve percent annually depending on carrier and policy design. The critical feature distinguishing Index Strategies from direct market investment is the zero-percent floor: when the S&P 500 declines, your cash value does not decrease.

The mechanics work through annual reset periods. Each year, your cash value is credited based on the index performance for that period, subject to the policy's cap rate. If the S&P 500 gains fifteen percent and your cap is ten percent, you receive a ten percent credit. If the index drops thirty percent, you receive zero percent credit—but you lose nothing. Your previous year's gains lock in and become your new baseline for the following year's growth calculation. This annual reset mechanism protects accumulated wealth from subsequent market corrections, allowing you to compound from a continually protected base rather than repeatedly recovering from losses.

The life insurance component provides a death benefit that passes income-tax-free to beneficiaries, but the retirement application focuses on accessing accumulated cash value during your lifetime. After the policy has been in force for sufficient time—typically ten to fifteen years depending on funding levels—you can access cash value through policy loans that are not classified as taxable income. These loans use your cash value as collateral while the full amount continues earning index credits, creating a double-compounding effect that traditional retirement accounts cannot replicate.

Premium flexibility distinguishes universal life products from whole life insurance. While whole life requires fixed premium payments, IUL policies allow you to adjust contributions within specified ranges, providing adaptability as your financial circumstances change. Overfunding strategies—contributing substantially more than the minimum required premium—accelerate cash value accumulation and maximize the policy's retirement income potential, subject to Modified Endowment Contract limits that preserve tax-advantaged treatment.

How Does S&P 500 Index Strategy Compare to Direct Market Investment?

The S&P 500 has historically delivered strong long-term returns—averaging approximately ten percent annually over extended periods—but with full exposure to market losses that can devastate retirement planning. Index Strategies track S&P 500 performance up to a cap rate, while a guaranteed floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss. This distinction becomes critical when analyzing actual retirement outcomes rather than idealized projections.

Consider the mathematical reality of market losses. If the S&P 500 drops thirty percent, a traditional investor loses thirty percent of their account value and requires a forty-three percent gain just to break even. That's not a thirty percent recovery—it's forty-three percent, because you're now working from a smaller base. An Index Strategy investor loses zero percent and captures the next market recovery from their full principal balance, compounding from a protected base. This is what we mean when we say Zero is Your Hero: your worst year is zero percent, not negative twenty, negative thirty, or negative fifty percent.

The cap rate represents the tradeoff for downside protection. While direct S&P 500 investors capture all upside during exceptional years—those rare periods when the index gains twenty, thirty, or even forty percent—Index Strategy participants receive credits only up to their policy's cap. However, historical analysis reveals that the S&P 500 rarely delivers consistent double-digit returns. Instead, it oscillates between dramatic gains and devastating losses, with the average obscuring significant volatility. Index Strategies smooth this volatility, trading extraordinary upside capture for elimination of downside risk.

Sequence of returns risk—the danger of experiencing market losses early in retirement when you're simultaneously withdrawing funds—represents one of the most underappreciated threats to retirement security. Two investors with identical average returns over twenty years can experience vastly different outcomes based solely on the order in which those returns occur. The investor who faces losses early while taking withdrawals depletes principal and never recovers. The Index Strategy investor maintains principal protection throughout the distribution phase, eliminating sequence risk entirely.

S&P 500 vs Index Strategy: Protected Participation

The S&P 500 has historically delivered strong long-term returns—but with full exposure to market losses. Index Strategies track S&P 500 performance up to a cap rate, while a guaranteed floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss. If the S&P 500 drops thirty percent, a traditional investor loses thirty percent and needs a forty-three percent gain just to break even. An Index Strategy investor loses zero percent and captures the next market recovery from their full principal—compounding from a protected base. Zero is Your Hero. This floor-and-cap mechanism transforms retirement planning from a volatility management exercise into a tax-efficient accumulation strategy with mathematical certainty around downside protection.

How Do Tax Benefits Position Index Strategies for Retirement Income?

The tax treatment of Indexed Universal Life Insurance creates advantages that compound dramatically over multi-decade retirement periods. Cash value growth within the policy accumulates tax-deferred—no annual capital gains taxation, no dividend taxation, no interest income reporting. This mirrors the tax-deferral of 401(k) and IRA accounts, but the similarity ends there. While qualified retirement plans eventually force taxable distributions through required minimum distributions beginning at age seventy-three, IUL policies have no required distribution age and no mandatory withdrawal requirements.

Policy loans—the primary method for accessing IUL cash value during retirement—are not classified as income by the IRS. You're technically borrowing against your death benefit using your cash value as collateral, and loans are not taxable events. This creates a tax-free income stream that preserves your adjusted gross income at levels that minimize Social Security benefit taxation, avoid Medicare premium surcharges, and maintain eligibility for tax credits and deductions that phase out at higher income levels. A married couple with two hundred thousand dollars in annual retirement needs could potentially satisfy this entirely through policy loans without reporting a single dollar as taxable income.

The Three Tax Buckets framework illustrates why this matters. Taxable accounts like brokerage accounts face annual taxation on dividends, interest, and realized capital gains. Tax-deferred accounts like 401(k)s and traditional IRAs postpone taxation but eventually force withdrawals taxed as ordinary income at potentially higher future rates. Tax-exempt accounts like Roth IRAs and properly structured Index Strategies provide access to accumulated funds without generating taxable income. Retirement income planning becomes a strategic withdrawal sequence exercise: which bucket do you tap first, and in what proportion, to minimize lifetime tax liability?

Most families overweight tax-deferred buckets because employer-sponsored plans default to 401(k) contributions. This creates a tax time bomb: substantial required minimum distributions in retirement that trigger taxation precisely when income flexibility matters most. Index Strategies provide tax bucket diversification, creating a source of retirement income that doesn't increase your tax bracket, doesn't affect Social Security taxation, and doesn't trigger the net investment income tax that affects high earners. This flexibility becomes invaluable during tax planning conversations: Do we convert traditional IRA funds to Roth? Do we realize capital gains this year? Do we accelerate or defer income? Having a tax-exempt income source creates options that purely tax-deferred portfolios cannot access.

What Role Does Life Insurance Protection Play in Retirement Planning?

While retirement income applications dominate Index Strategy discussions, the permanent life insurance protection provides estate planning and legacy benefits that term insurance and investment-only strategies cannot replicate. The death benefit pays income-tax-free to beneficiaries regardless of when death occurs, providing immediate liquidity to cover estate settlement costs, final expenses, and wealth transfer objectives. Unlike term policies that expire after twenty or thirty years, permanent coverage remains in force for life, assuming premium obligations are satisfied.

Human Life Value—your lifetime income-generating potential—represents your family's most valuable and most underinsured asset. If a forty-five-year-old professional earning two hundred thousand dollars annually works another twenty years, that's four million dollars in gross income that supports mortgage payments, college funding, lifestyle maintenance, and retirement contributions. If premature death eliminates this income stream, what replaces it? Term insurance provides temporary protection, but most families outlive their term policies and face prohibitively expensive premiums if they attempt to renew coverage in their sixties or seventies.

Index Strategies address this gap by combining permanent protection with cash value accumulation. The death benefit protects your family's financial security throughout your working years, while cash value builds the retirement income source you'll access if you live. This dual-purpose design eliminates the "rent versus own" debate that plagues term insurance discussions. Term insurance is renting protection: you pay premiums, receive coverage for a defined period, and build zero equity. Permanent insurance with cash value is owning protection: premiums build equity that you can access, borrow against, or surrender for cash value while maintaining a death benefit.

Living benefits—policy riders that provide access to death benefit funds while you're alive in the event of chronic, critical, or terminal illness—transform life insurance from a death-only product into a comprehensive risk management tool. If you're diagnosed with a qualifying condition, you can accelerate a portion of your death benefit to cover medical expenses, long-term care costs, or income replacement during treatment. This addresses the retirement wild card that most financial plans ignore: catastrophic health events that drain retirement accounts precisely when recovery capacity has disappeared.

How Should Index Strategies Be Funded for Maximum Retirement Benefit?

Policy funding strategy determines whether an Index Strategy functions as primarily insurance protection with modest cash value or as a tax-efficient retirement accumulation vehicle with substantial income potential. Minimum premium funding keeps the policy in force but limits cash value growth, making this approach suitable for those prioritizing death benefit protection over retirement income. Maximum funding—contributing the highest premium allowed without triggering Modified Endowment Contract status—accelerates cash value accumulation and maximizes retirement income potential.

The Modified Endowment Contract threshold represents the IRS limit on how much you can contribute to a life insurance policy while maintaining tax-advantaged loan treatment. Policies that exceed MEC limits become subject to last-in-first-out taxation on withdrawals and a ten percent early withdrawal penalty before age fifty-nine and a half—similar to IRA treatment. Proper policy design keeps contributions just below the MEC threshold, maximizing funding while preserving tax benefits. This requires annual testing and careful premium management, which is why working with an independent broker who understands IRS guidelines becomes essential.

Front-loading strategies concentrate contributions in early policy years to accelerate cash value growth and reduce the number of years until the policy becomes self-sustaining. Rather than spreading contributions evenly over thirty years, you might fully fund the policy over seven to ten years, allowing the accumulated cash value and annual index credits to cover future premium requirements without additional out-of-pocket contributions. This approach requires higher initial cash flow but creates hands-off retirement income sooner and maximizes the compounding period for your accumulated cash value.

Premium flexibility allows you to adjust funding as circumstances change. If you receive a bonus, inheritance, or windfall, you can make supplemental contributions up to the MEC limit. If you face temporary financial constraints, you can reduce premiums to the minimum required to keep the policy in force, or even skip premiums entirely by using accumulated cash value to cover the cost. This adaptability distinguishes universal life products from both whole life insurance and qualified retirement plans, where contribution rules are rigid and penalties apply for early withdrawals.

What Are the Costs, Fees, and Breakeven Considerations?

Transparency around costs separates independent broker guidance from captive agent sales tactics. Index Strategies carry internal expenses that include cost of insurance charges for the death benefit, administrative fees, and premium loads that cover distribution costs. These fees are deducted from premium payments and cash value, reducing the net amount available for index crediting. Understanding these costs and their impact on long-term performance becomes essential for making informed decisions about whether Index Strategies align with your retirement objectives.

Cost of insurance charges increase with age because mortality risk rises as you get older. This creates a long-term fee structure where early years carry relatively modest insurance costs, but later years—particularly after age sixty-five—see accelerating charges. Policy illustration software models these costs over the policy's lifetime, allowing you to evaluate whether projected index credits exceed total fees sufficiently to generate the cash value accumulation and retirement income you expect. This is why overfunding strategies work: higher early cash value generates index credits that outpace rising insurance costs.

Breakeven timelines—the point at which your accumulated cash value exceeds total premiums paid—typically range from ten to fifteen years depending on funding levels, index performance, and policy design. Unlike qualified retirement plans where contributions are immediately fully credited to your account, life insurance policies front-load certain costs, creating early years where cash value lags premiums. This is not a defect; it's a design feature reflecting the permanent death benefit protection that begins immediately. Families who treat Index Strategies as short-term investments will be disappointed. Those who implement them as multi-decade retirement and estate planning tools find the cost structure justified by the unique combination of benefits.

Fee comparison exercises between Index Strategies and actively managed investment accounts reveal interesting tradeoffs. A typical managed portfolio charges one to one and a half percent annually in advisory fees, plus underlying fund expenses that add another twenty to sixty basis points. Over thirty years, these fees compound dramatically. Using the Rule of 72, a one and a half percent annual fee drag cuts your ending account value by approximately thirty-seven percent compared to a no-fee alternative. Index Strategies consolidate costs into the insurance charges and cap rate structure, with no separate advisory fees, no transaction costs, and no tax drag from annual capital gains recognition. The total cost comparison becomes complex, but properly structured Index Strategies often deliver competitive net results while providing downside protection and tax-free access that managed accounts cannot replicate.

About Steven Rosenberg & Everence Wealth

Steven Rosenberg is an independent insurance broker and the founder of Everence Wealth, a San Francisco-based financial services firm specializing in tax-efficient Index Strategies and retirement income planning. Licensed to serve families across all fifty states, Steven operates with seventy-five-plus carrier partnerships, ensuring clients access wholesale-priced strategies without the conflicts of interest inherent in captive agent models. His expertise centers on bridging the Retirement Gap through S&P 500-linked growth strategies that protect principal while eliminating the three silent killers: fees, volatility, and taxes. Steven's educational frameworks—including Zero is Your Hero, the Three Tax Buckets, and Cash Flow > Net Worth—provide families with structured approaches to retirement planning that prioritize sustainable income over paper net worth. As an independent broker, Steven works exclusively in the client's best interest, with no allegiance to any insurance company, bank, or Wall Street institution. His practice focuses on stress-testing retirement strategies against real-world scenarios including market corrections, tax law changes, and longevity risk, helping clients build resilient financial plans that perform across multiple decades. Steven's analytical approach combines actuarial science, tax code expertise, and behavioral finance insights to deliver holistic wealth strategies that protect prosperity across generations.

Stress-Test Your Retirement Strategy with a Financial Needs Assessment

Understanding how Indexed Universal Life Insurance could fit into your retirement plan requires personalized analysis of your current tax exposure, retirement income gap, and long-term wealth transfer objectives. We offer a comprehensive Financial Needs Assessment that evaluates your existing retirement accounts, projects after-tax income availability, and identifies opportunities to diversify across all three tax buckets. This assessment includes side-by-side comparisons of Index Strategy scenarios versus your current approach, with detailed illustrations showing cash value accumulation, retirement income projections, and death benefit protection. As an independent broker with seventy-five-plus carrier partnerships, we design strategies around your objectives—not commission structures or product quotas. Schedule your Financial Needs Assessment today to discover whether Index Strategies can help you participate in S&P 500 growth while protecting your principal and accessing retirement income tax-free.

Schedule Your Financial Needs AssessmentThis content is for educational purposes only and does not constitute financial, tax, or legal advice. Index Strategy performance depends on multiple factors including premium funding levels, index performance, policy fees, and loan interest rates. Consult a licensed professional before making any financial decisions.