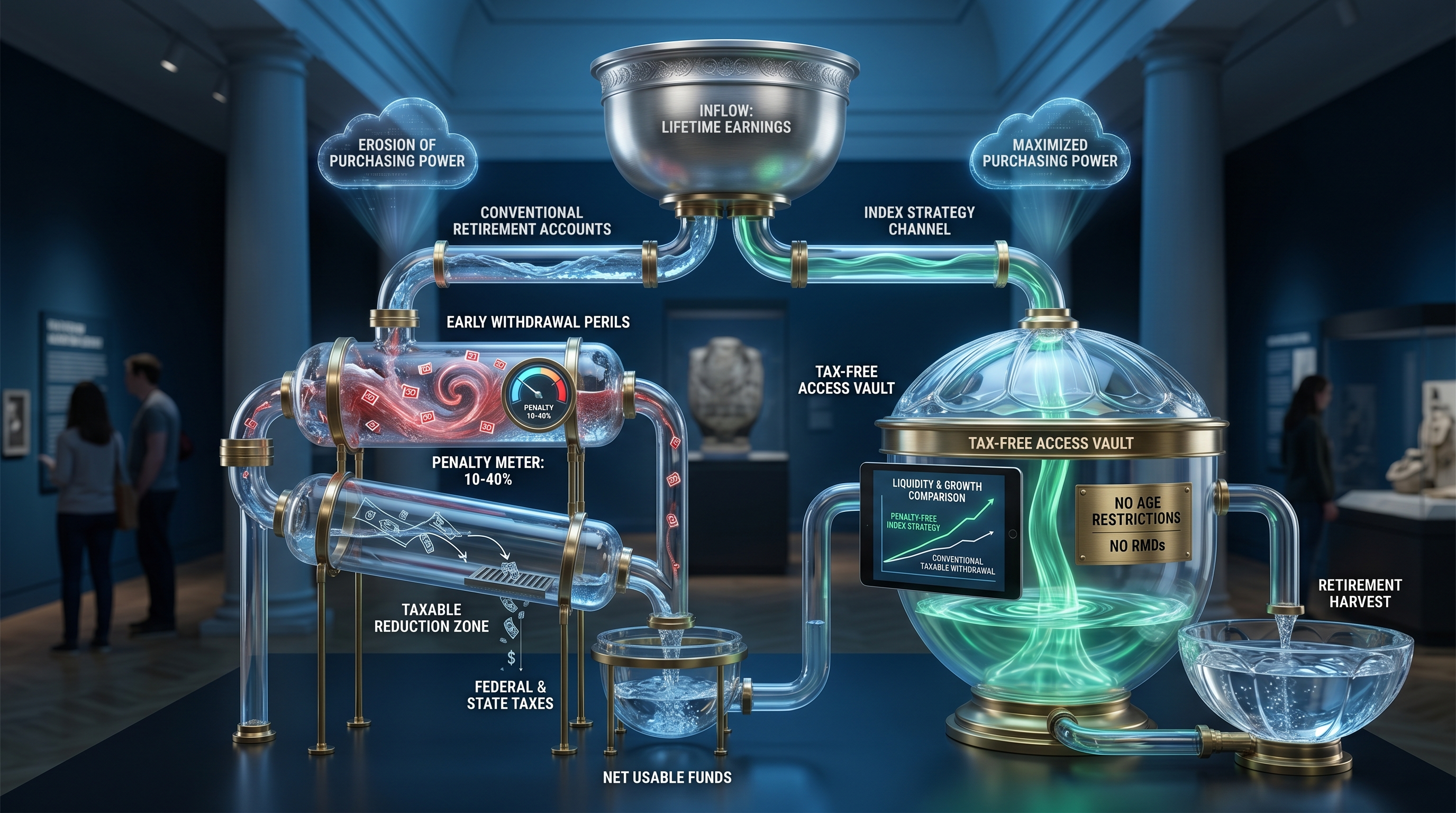

Retirement account early withdrawal penalties can cost 10-40% of your savings through IRS penalties, state taxes, and federal income taxes combined. However, Index Strategies offered by Everence Wealth provide tax-free policy loan access without penalties, age restrictions, or Required Minimum Distributions—a key advantage in the Three Tax Buckets framework for retirement income flexibility.

Most Americans believe their 401(k) or IRA balance represents their actual retirement wealth. But when you factor in early withdrawal penalties, federal taxes, state taxes, and the opportunity cost of compound growth on withdrawn funds, that $500,000 account might only deliver $300,000 of actual purchasing power if accessed before age 59½. We've seen clients forfeit decades of wealth accumulation to penalty structures they didn't fully understand when they started contributing.

The retirement account penalty system exists to discourage early access—but life doesn't always cooperate with IRS age thresholds. Medical emergencies, business opportunities, family crises, and unexpected expenses force millions of Americans to choose between financial penalties and financial survival. The challenge isn't just the immediate 10% early withdrawal penalty—it's the cascading tax consequences, the permanent loss of tax-advantaged space, and the compounding damage to long-term retirement security.

As an independent broker with access to 75+ carriers nationwide, we help families build retirement strategies that provide both growth potential and penalty-free liquidity through Index Strategies. These vehicles track S&P 500 performance with downside protection while offering tax-free policy loan access at any age—no penalties, no Required Minimum Distributions, and no permanent erosion of your wealth-building capacity. Let's examine exactly what retirement account penalties cost you and how strategic planning can eliminate these wealth destroyers entirely.

What Are Retirement Account Early Withdrawal Penalties and How Do They Work?

The IRS imposes a 10% early withdrawal penalty on distributions from qualified retirement accounts—including traditional IRAs, 401(k)s, 403(b)s, and similar vehicles—taken before age 59½. This penalty applies to the entire distribution amount and comes in addition to ordinary income taxes owed on the withdrawal. For someone in the 24% federal tax bracket living in California (13.3% state tax), a $50,000 early withdrawal could trigger $5,000 in penalties, $12,000 in federal taxes, and $6,650 in state taxes—leaving just $26,350 of actual usable funds from a $50,000 account withdrawal.

The penalty structure exists to preserve the tax-advantaged purpose of retirement accounts: encouraging long-term savings by imposing costs on early access. Congress designed these accounts with specific tax deferrals in exchange for restricted access until retirement age. When you withdraw early, you break that agreement, and the IRS collects both the deferred taxes and an additional penalty. This creates what we call a triple tax trap: you lose 10% to penalties, 15-37% to federal income taxes depending on your bracket, and potentially another 0-13.3% to state income taxes depending on where you live.

Beyond the immediate financial hit, early withdrawals create permanent damage to your retirement trajectory. The withdrawn funds lose all future tax-deferred compounding potential. A $50,000 withdrawal at age 45 doesn't just cost you $50,000—it costs you the $200,000+ that amount could have grown to by age 65 with S&P 500-linked returns. You've also permanently lost that contribution space; unlike a Roth IRA where you might replace principal, traditional retirement accounts don't allow you to "repay" an early withdrawal and restore your tax-advantaged capacity.

The penalty applies to the taxable portion of your distribution. For traditional IRAs and 401(k)s funded with pre-tax contributions, the entire distribution is both taxable and subject to penalty. For Roth IRAs, your contributions can be withdrawn anytime tax and penalty-free, but earnings withdrawn before age 59½ trigger both taxes and penalties. Roth conversions follow a five-year aging rule before penalty-free access. Understanding these nuances is critical—many people unknowingly trigger penalties by accessing the wrong funds at the wrong time from accounts they believed were penalty-free.

The True Cost: Calculating Total Withdrawal Impact Beyond the 10% Penalty

The 10% early withdrawal penalty is just the beginning of the actual cost. To understand the real financial impact, you must calculate the combined effect of federal income taxes, state income taxes, the 10% penalty, and the opportunity cost of lost compound growth. Let's examine a realistic scenario: A 45-year-old professional in California earning $120,000 annually needs $75,000 for a down payment on an investment property. They consider withdrawing from their traditional 401(k) with a $300,000 balance.

Here's the complete math: The $75,000 withdrawal adds to their taxable income, potentially pushing them into the 32% federal bracket (married filing jointly, $120,000 + $75,000 = $195,000 total income). Federal taxes consume approximately $24,000. California state taxes at 9.3% take another $6,975. The 10% early withdrawal penalty adds $7,500. Total taxes and penalties: $38,475. To net $75,000 after taxes and penalties, they must withdraw approximately $119,048 from the 401(k)—consuming 40% of their retirement savings to access what they actually needed. The effective cost rate isn't 10%—it's 58.7% when you compare the $119,048 withdrawn to the $75,000 received.

The opportunity cost compounds the damage exponentially. That $119,048 withdrawn at age 45 would have grown to approximately $476,192 by age 65 assuming historical S&P 500 returns of 7-8% annually after inflation. So the true cost of accessing $75,000 today is forfeiting nearly half a million dollars of future retirement security. This is why we emphasize Cash Flow > Net Worth in our planning framework—accessing trapped equity through penalties destroys more wealth than most people can mathematically afford, even when they believe they're making a sound investment with the withdrawn funds.

State tax impact varies dramatically by location, creating geographic wealth inequality in retirement planning. Residents of Texas, Florida, Nevada, and other no-income-tax states avoid the state tax layer entirely, reducing the total bite by 3-13.3% depending on the comparison state. A $100,000 early withdrawal costs a Texas resident approximately $42,000 in combined federal taxes and penalties, while the same withdrawal costs a California resident approximately $55,300—a $13,300 difference purely due to state tax policy. This geographic disparity is one reason high-tax-state residents increasingly explore Index Strategies as a tax-free alternative that eliminates state tax exposure on retirement income entirely.

IRS Exceptions to the 10% Early Withdrawal Penalty: What Qualifies and What Doesn't

The IRS provides specific exceptions to the 10% early withdrawal penalty, but these exceptions are narrower and more restrictive than most people realize. Qualifying for an exception eliminates the 10% penalty but does not eliminate the income taxes owed on the distribution—you still pay federal and state taxes on the full amount withdrawn. The most commonly used exceptions include: substantially equal periodic payments (SEPP/72(t) distributions), qualified medical expenses exceeding 7.5% of adjusted gross income, health insurance premiums while unemployed, qualified higher education expenses, first-time home purchases up to $10,000, IRS levy to satisfy tax debt, and total and permanent disability.

The SEPP exception under IRS Rule 72(t) allows penalty-free withdrawals before age 59½ if you commit to taking substantially equal periodic payments for at least five years or until you reach age 59½, whichever is longer. Once started, you cannot modify the payment schedule without triggering retroactive penalties on all distributions taken. This rigidity makes 72(t) distributions risky for anyone whose financial needs might change—if you start withdrawals at age 50, you're locked into that payment structure for 9½ years with no flexibility for emergencies or changed circumstances. We've seen clients trapped by 72(t) elections that made sense initially but became financially destructive when circumstances changed.

The first-time homebuyer exception allows up to $10,000 in penalty-free IRA withdrawals (not 401(k)s—those don't qualify) for a home purchase, but this $10,000 limit hasn't increased since the provision was created decades ago. In today's real estate market, $10,000 barely covers closing costs, let alone a down payment, making this exception far less useful than its name suggests. Additionally, "first-time" is defined as not having owned a home in the past two years—so even previous homeowners can qualify, but the $10,000 limit per lifetime makes it a one-time-use tool with minimal impact on actual home affordability.

Qualified higher education expenses offer penalty-free access for tuition, fees, books, supplies, and equipment for yourself, your spouse, children, or grandchildren. Room and board qualify only if the student is enrolled at least half-time. While this exception removes the 10% penalty, you still owe income taxes on the withdrawn amount, and you've permanently depleted retirement savings to fund education—often creating a situation where parents sacrifice their own retirement security to avoid student loans for their children. Financially, this trade-off rarely makes sense, as student loans offer flexible repayment terms, income-driven options, and potential forgiveness, while depleted retirement savings compound lost opportunity cost that can never be recovered.

S&P 500 vs Index Strategy: Accessing Growth Without Withdrawal Penalties

The S&P 500 has historically delivered strong long-term returns—but with full exposure to market losses and, when held in retirement accounts, severe early withdrawal penalties and eventual Required Minimum Distributions. Index Strategies track S&P 500 performance up to a cap rate, while a guaranteed floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss. But the critical advantage for liquidity planning is this: Index Strategies allow tax-free policy loan access at any age with zero penalties, no income taxes, and no impact on your principal's continued compound growth.

Here's the mathematical reality of recovery after losses that makes the zero floor so powerful: If the S&P 500 drops 30%, a traditional investor loses 30% and needs a 43% gain just to break even—a mathematical requirement that has taken years to achieve after major downturns like 2000-2002 and 2008-2009. An Index Strategy investor loses 0% and captures the next market recovery from their full principal. This is what we call Zero is Your Hero. Over a 30-year retirement, avoiding just two major drawdowns while participating in the recoveries dramatically compounds your ending wealth compared to full market exposure—even accounting for the cap rate limitations on upside participation.

The liquidity advantage eliminates the entire penalty discussion. Traditional 401(k) or IRA withdrawals before 59½ trigger 10% penalties plus income taxes. Index Strategy policy loans trigger zero penalties, zero income taxes, and zero Required Minimum Distributions at age 73. You borrow against your cash value at competitive rates (often 4-6%), maintain the full principal earning index-linked growth, and repay on your schedule—or never repay and have the loan balance deducted from the death benefit. This flexibility transforms retirement planning from a rigid age-gated system into a dynamic tool you control across all life stages.

For someone facing an emergency at age 50, the contrast is stark: withdrawing $50,000 from a 401(k) might cost $20,000+ in taxes and penalties, netting $30,000. Borrowing $50,000 from an Index Strategy cash value costs zero in taxes and penalties, provides the full $50,000, and allows your principal to continue compounding on the full balance. If that emergency resolves and you repay the loan, you've accessed liquidity with zero permanent damage to your wealth trajectory. Even if you never repay it, the loan simply reduces your eventual death benefit—but your retirement income continues unaffected because you're accessing wealth through loans, not liquidations.

S&P 500 vs Index Strategy: Protected Participation and Penalty-Free Access

Traditional S&P 500 exposure through 401(k)s and IRAs subjects you to full market volatility, early withdrawal penalties of 10% plus taxes, Required Minimum Distributions starting at age 73, and income taxes on every distribution. Index Strategies provide S&P 500-linked growth potential up to an annual cap rate (often 10-13%), a guaranteed 0% floor protecting you from market losses, tax-free policy loan access at any age with no penalties, and zero Required Minimum Distributions. The floor/cap tradeoff means you sacrifice unlimited upside potential in exchange for downside protection and liquidity flexibility. If the S&P 500 returns 25% in a strong year, you might capture 12% due to the cap. But if the S&P 500 drops 25% the next year, you lose nothing while traditional investors must recover a 33% gain just to return to break-even. Over full market cycles spanning accumulation and distribution phases, the protected base and penalty-free liquidity often deliver superior after-tax, after-penalty retirement outcomes compared to fully exposed alternatives—especially for families who value liquidity, tax efficiency, and protection equally with growth potential. This is the Zero is Your Hero framework applied to both market risk and penalty risk simultaneously.

The Three Tax Buckets and Penalty-Free Retirement Income Planning

Understanding retirement account penalties requires understanding the Three Tax Buckets framework—the foundation of tax-efficient retirement income planning. Every dollar you own lives in one of three buckets based on how it's taxed: Taxable (brokerage accounts, savings, CDs—taxed annually on interest, dividends, and capital gains), Tax-Deferred (401(k)s, traditional IRAs, 403(b)s—taxed on distributions, subject to RMDs, and penalized if accessed early), and Tax-Exempt (Roth IRAs, Roth 401(k)s, and Index Strategies—grow and distribute tax-free under current tax law). The penalty problem exists almost entirely in the Tax-Deferred bucket, where Congress granted upfront tax deductions in exchange for restricted access and eventual forced distributions.

Most American families unknowingly concentrate 70-90% of their retirement savings in the Tax-Deferred bucket through employer 401(k)s, creating massive tax risk, penalty risk, and RMD risk. When you need emergency funds before age 59½, your only accessible wealth sits in accounts that penalize early access. When you reach age 73, those same accounts force you to withdraw and pay taxes whether you need the income or not, potentially pushing you into higher tax brackets and triggering taxes on Social Security benefits and Medicare premium surcharges. This bucket imbalance creates a retirement income system with no flexibility, no control, and maximum tax exposure.

The Tax-Exempt bucket solves both the penalty problem and the RMD problem simultaneously. Roth IRAs allow you to withdraw your contributions (but not earnings) anytime without penalties or taxes, but contribution limits of $7,000 annually ($8,000 if 50+) severely restrict how much wealth you can build in this bucket. Index Strategies function as Roth-equivalent vehicles with no contribution limits, no income phase-outs, and policy loan access to both principal and growth without triggering taxable events. For high-income professionals who exceed Roth IRA income limits or who want to contribute more than $7,000 annually to tax-free retirement vehicles, Index Strategies provide the only scalable Tax-Exempt bucket available under current tax law.

Strategic bucket diversification eliminates penalty risk entirely. Instead of funding only a 401(k) and facing 10%+ penalties for early access, you fund multiple buckets: enough in the Tax-Deferred bucket to capture employer matching, systematic funding of the Tax-Exempt bucket through Index Strategies for penalty-free liquidity across all ages, and tactical use of Taxable buckets for short-term flexibility. When emergency needs arise before age 59½, you access the Tax-Exempt bucket via policy loans—zero penalties, zero taxes. When you reach retirement, you control your tax bracket by strategically withdrawing from each bucket in the most tax-efficient sequence, avoiding RMD-driven tax spikes and maintaining maximum after-tax income. This is proactive tax planning, not reactive penalty avoidance.

Retirement Account Loans vs Early Withdrawals: Understanding 401(k) Loan Rules

Many 401(k) plans offer loan provisions allowing participants to borrow against their account balance without triggering early withdrawal penalties or income taxes—but these loans come with strict limitations, repayment requirements, and significant risks that most participants don't fully understand. A 401(k) loan allows you to borrow up to 50% of your vested balance or $50,000, whichever is less. You repay the loan through payroll deductions over five years (or longer for primary residence purchases), and the interest you pay goes back into your own account. On the surface, this seems like an ideal penalty-free access strategy—but the details create substantial wealth destruction.

First, 401(k) loans must be repaid with after-tax dollars. You originally contributed to the 401(k) with pre-tax payroll deductions, reducing your taxable income. When you repay a 401(k) loan, you're using post-tax income from your paycheck—meaning you've lost the tax advantage on those dollars entirely. Then, when you eventually withdraw that money in retirement, you pay taxes again on the same dollars. This creates a double-taxation scenario on loan repayments that erodes the core tax benefit of 401(k) participation. You've converted tax-deferred money into taxed-twice money through the loan structure.

Second, if you leave your employer—whether through termination, resignation, or layoff—most plans require full loan repayment within 60-90 days. If you cannot repay, the outstanding loan balance is treated as a taxable distribution, triggering income taxes and the 10% early withdrawal penalty if you're under age 59½. During economic downturns when layoffs are common and finding new employment takes longer, this loan acceleration creates devastating financial consequences: you've lost your income, you owe taxes on a distribution you never actually received as cash, and you've permanently depleted your retirement savings. We've seen clients forced into bankruptcy after job loss triggered 401(k) loan default and created tax liabilities they couldn't pay.

Third, 401(k) loans remove invested capital from the market during the loan period. While you're repaying the loan, that borrowed amount is not participating in market gains—you're earning the loan interest rate (typically prime + 1-2%, around 9-10%) instead of potential S&P 500 returns. If the market delivers strong returns during your five-year loan repayment period, you've permanently lost that growth opportunity on the borrowed amount. The opportunity cost of foregone market gains often exceeds any perceived benefit of penalty-free access, especially for loans taken before major bull market runs. A $50,000 loan taken in 2010 and repaid by 2015 would have missed the 100%+ S&P 500 gains during that recovery period—a permanent loss of over $50,000 in potential growth.

Why Independent Brokers Recommend Index Strategies for Penalty-Free Lifetime Liquidity

As an independent broker with access to 75+ carriers across all 50 states, we're not employed by any insurance company, bank, or Wall Street institution. We work exclusively in the client's best interest, evaluating strategies across the entire market to find solutions that align with your goals, risk tolerance, and liquidity needs. This independence allows us to objectively compare retirement account structures and recommend Index Strategies not because we're captive to a single product, but because the math, the tax treatment, and the liquidity provisions deliver superior outcomes for families who value protection and flexibility alongside growth.

Wall Street firms and employer 401(k) platforms operate in what we call the retail financial system—marked by high embedded fees (1.5-2.5% total cost annually when you include advisor fees, fund expense ratios, and administrative costs), limited investment options (typically 10-25 mutual funds selected by the plan administrator), and no access to wholesale-priced insurance strategies that provide downside protection and tax-free liquidity. Independent brokers access the wholesale financial system—working directly with carriers offering institutional pricing, zero annual account fees, and product structures designed for tax efficiency and multi-generational wealth transfer. This retail-vs-wholesale distinction often determines whether your wealth compounds at 7% net (after fees) or 9% net (wholesale) over 30-35 years—the difference between retiring with $1 million or $2 million from the same contribution level.

Index Strategies eliminate the penalty discussion entirely through policy loan provisions. At any age, you can borrow against your cash value without penalties, without income taxes, and without credit checks or approval processes. The loan doesn't appear on your credit report, doesn't require monthly payments (interest can compound into the loan balance), and doesn't reduce your policy's continued index-linked growth potential. Your full cash value continues earning returns even while borrowed against. This creates the ultimate liquidity: accessible wealth with zero government restrictions, zero penalties, and zero forced distribution schedules. Compare this to 401(k) penalties, IRA penalties, and RMD mandates—every one of which represents government control over your wealth and government-imposed costs for accessing your own money.

The independent broker advantage extends beyond product access to ongoing strategy design. We stress-test your financial plan against market downturns, tax law changes, early liquidity needs, disability scenarios, and estate planning goals. If a 401(k) meets your needs efficiently—especially with generous employer matching—we recommend maximizing it within the Three Tax Buckets framework. But when penalty-free liquidity, tax-free retirement income, and downside protection become priorities—and especially for high-income earners who exceed Roth IRA limits—Index Strategies consistently deliver the most efficient vehicle for Tax-Exempt bucket wealth accumulation. Our compensation is transparent, our carrier options are comprehensive, and our guidance remains unconflicted by corporate product quotas or proprietary investment platforms.

About Steven Rosenberg & Everence Wealth

Steven Rosenberg is the Founder and Chief Wealth Strategist at Everence Wealth, an independent financial firm based in San Francisco, California. As an independent broker, Steven partners with more than 75 insurance carriers to deliver tax-efficient retirement strategies for families, business owners, and professionals across all 50 states. His expertise centers on Index Strategies—S&P 500-linked wealth-building vehicles with zero-floor protection and tax-free policy loan access—designed to eliminate the Three Silent Killers of retirement wealth: fees, volatility, and taxes. Steven specializes in helping high-income earners and residents of high-tax states maximize Tax-Exempt bucket contributions through Index Strategies that provide penalty-free liquidity at any age, zero Required Minimum Distributions, and protection from market downturns. Unlike captive agents employed by single insurance companies or fee-based advisors managing only investment portfolios, Steven operates as an independent broker with no corporate quotas, no proprietary products, and no conflicts of interest—offering unbiased guidance backed by carrier diversity and comprehensive tax strategy frameworks including the Three Tax Buckets, Zero is Your Hero, and S&P 500 vs Index Strategy comparisons. Every recommendation is mathematically stress-tested against fees, volatility, tax exposure, and liquidity requirements to ensure alignment with the client's complete financial picture. Steven's educational approach emphasizes transparency, data-driven analysis, and long-term wealth preservation through strategies that balance growth potential with downside protection and penalty-free access across all life stages.

Eliminate Retirement Account Penalties with a Customized Index Strategy Plan

If you're facing early withdrawal penalties, navigating 401(k) loan rules, or concerned about future Required Minimum Distributions, a Financial Needs Assessment with Everence Wealth provides clarity, strategy, and actionable solutions. We'll stress-test your current retirement accounts against penalty risk, tax exposure, and liquidity needs—then design a Three Tax Buckets diversification strategy incorporating Index Strategies for penalty-free access, S&P 500-linked growth with zero-floor protection, and tax-free retirement income. As an independent broker with 75+ carrier partnerships, we compare institutional-grade solutions unavailable through employer plans or retail brokerage platforms—delivering wholesale pricing, transparent costs, and unconflicted guidance aligned exclusively with your wealth-building goals. Schedule your complimentary Financial Needs Assessment today and discover how Index Strategies eliminate penalties, protect principal, and provide lifetime liquidity you control.

Schedule Your Financial Needs AssessmentThis content is for educational purposes only and does not constitute financial, tax, or legal advice. Index Strategy performance depends on policy structure, cap rates, participation rates, and carrier financial strength. Policy loans reduce death benefits and available cash value if not repaid. Consult a licensed insurance professional and tax advisor before implementing any retirement or tax strategy.