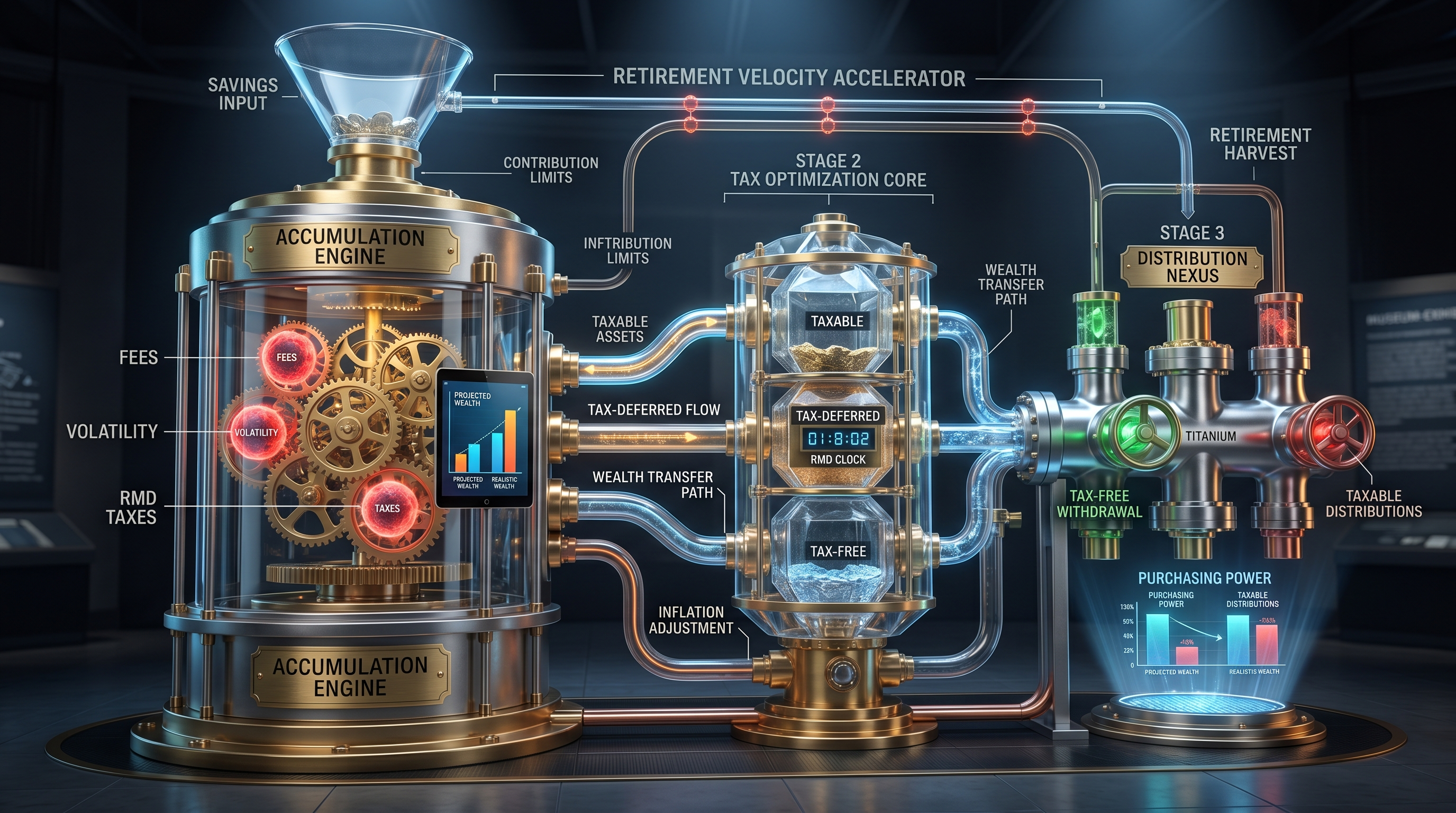

The 401k retirement calculator reveals critical gaps between projected savings and actual retirement income needs. At Everence Wealth, we've stress-tested thousands of portfolios using the Three Tax Buckets framework, uncovering how fees, volatility, and forced distributions erode purchasing power by 30-40% in retirement years.

Most Americans approach retirement with blind faith in their 401k statements, assuming that the balance projected by a standard 401k retirement calculator represents their true financial security. Yet in our experience stress-testing portfolios for families across all 50 states, we consistently discover that traditional calculators miss three silent killers that can reduce actual spending power by 30-40% during retirement years: compound fee drag, sequence-of-returns volatility, and mandatory tax exposure through Required Minimum Distributions. The mathematical reality is sobering—a $500,000 401k balance may deliver only $300,000 in actual purchasing power when subjected to real-world market conditions, distribution requirements, and tax obligations at potentially higher future rates.

The conventional 401k retirement calculator operates on dangerously optimistic assumptions: steady 7% annual returns without accounting for negative years, minimal fee impact calculations that ignore three-decade compounding effects, and tax-deferred growth projections that completely disregard the IRS mandatory distribution schedules beginning at age 73. These tools tell you what your balance might grow to, but they cannot tell you what that balance will actually deliver in sustainable, tax-adjusted income when you need it most. This disconnect between projected accumulation and actual distribution capacity represents the single largest blind spot in American retirement planning, affecting millions of households who discover the truth only after it's too late to restructure their strategy.

At Everence Wealth, we work as independent brokers partnered with 75+ carriers to help families build tax-diversified retirement strategies that address what traditional 401k calculators cannot measure: downside protection during market corrections, tax-free distribution capacity that eliminates RMD exposure, and guaranteed floor protection that prevents the devastating compounding damage of negative return years. By integrating Index Strategies that track S&P 500 performance with zero-loss floors alongside strategic tax bucket diversification, we help clients bridge the retirement gap that standard calculators fail to identify. This article reveals exactly what your 401k calculator isn't telling you and provides the mathematical frameworks to stress-test your retirement strategy against real-world risks.

Why Traditional 401k Retirement Calculators Miss the Three Silent Killers

When you input your current balance, contribution rate, and expected return into a standard 401k retirement calculator, the tool generates a smooth accumulation curve projecting decades into the future. But this mathematical elegance conceals three compounding destroyers that erode real-world outcomes: fees that compound against you for 30-35 years, volatility that damages your principal base during critical distribution years, and taxes that claim 22-37% of every withdrawal under current federal brackets—potentially higher when combined with state income taxes and future rate increases. We call these the Three Silent Killers because they operate invisibly inside tax-deferred accounts, compounding their damage year after year while your statement balance creates a false sense of security.

Consider the fee impact first. A typical 401k carries expense ratios of 0.5-1.5% annually when you account for plan administration costs, fund management fees, and advisor compensation layers. A 1% annual fee seems trivial in isolation, but over 30 years it doesn't reduce your balance by 30%—it reduces it by approximately 26% due to lost compounding on the fee amounts themselves. Using the Rule of 72, we can quickly calculate that a 1% fee doubles its damage roughly every 72 years, but over a 30-year accumulation period combined with a 20-year distribution period, that seemingly small percentage can cost a mid-career professional $200,000-400,000 in unrealized wealth. Standard 401k retirement calculators either ignore fees entirely or dramatically understate their long-term impact because they calculate fee drag linearly rather than exponentially.

The second silent killer—volatility—becomes especially dangerous during the distribution phase that most calculators completely ignore. Your 401k retirement calculator shows you an ending balance, but it cannot account for sequence-of-returns risk: the mathematically proven phenomenon where the timing of market losses relative to your withdrawal schedule determines whether your portfolio survives 25-30 years or depletes prematurely. If you retire into a bear market and begin taking distributions while your portfolio is declining, you lock in losses and reduce your principal base permanently. A 30% market correction in year one or two of retirement, combined with necessary living expense withdrawals, can reduce your portfolio's life expectancy by 8-12 years compared to the same average return sequence that begins with positive years. Traditional calculators cannot model this because they assume steady average returns—but retirement doesn't happen in averages.

The third silent killer—taxes—represents the largest single claim against your 401k balance, yet most retirement calculators treat it as a mere footnote. Every dollar you withdraw from a traditional 401k is taxed as ordinary income at your marginal federal rate (currently 10-37%), plus state income tax in 41 states, plus potential Medicare premium surcharges (IRMAA) if your distributions push you above $97,000 (single) or $194,000 (married) in modified adjusted gross income. Beginning at age 73, the IRS mandates Required Minimum Distributions calculated as a percentage of your balance—starting around 3.8% and increasing annually. You must take these distributions whether you need the income or not, and you must pay taxes on them at ordinary income rates. A $500,000 401k generates approximately $19,000 in mandatory first-year RMDs, creating a tax liability of $4,180-7,030 depending on your bracket—every year for the rest of your life, with the percentage increasing as you age.

The S&P 500 vs Index Strategy Framework: Capturing Growth While Protecting Your Floor

The S&P 500 has historically delivered strong long-term returns averaging approximately 10% annually over multi-decade periods—but with full exposure to market losses that can exceed 30-50% during recessionary cycles. When you invest directly in the S&P 500 through mutual funds or ETFs inside your 401k, you capture 100% of the upside during bull markets but you also absorb 100% of the downside during corrections. Index Strategies offer a fundamentally different mathematical structure: they track S&P 500 performance up to a predetermined cap rate (often 8-12% depending on carrier and policy year), while a contractually guaranteed floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss. This is what we call Zero is Your Hero—your worst year is 0%, not negative, which preserves your principal base for compounding during the next market recovery.

The mathematical advantage becomes clear when you stress-test both approaches through an actual market correction scenario. If the S&P 500 drops 30% in a given year, a traditional investor with $500,000 loses $150,000, reducing their balance to $350,000. To return to break-even, they now need a 42.86% gain—not 30%—because they're recovering from a smaller base. Meanwhile, the same investor using an Index Strategy with a 0% floor loses nothing during the correction year, maintaining their full $500,000 principal. When the market recovers and gains 20% the following year, the traditional investor grows their $350,000 to $420,000 (still $80,000 below starting point), while the Index Strategy investor captures the upside to their cap—let's assume a 10% cap—growing from $500,000 to $550,000. The Index Strategy investor is now $130,000 ahead despite giving up some upside participation, simply because they never lost their principal base to begin with.

This protection becomes exponentially more valuable during the retirement distribution phase, when you're simultaneously withdrawing living expenses and trying to preserve your portfolio through market volatility. With a traditional 401k invested in S&P 500 index funds, a bear market forces you to sell shares at depressed prices to meet your income needs—permanently reducing your principal and eliminating those shares from future recovery gains. With an Index Strategy, your contractual floor prevents account value loss while still allowing you to take distributions, and your gains lock in annually through the annual reset mechanism. Each year's positive return becomes your new protected floor for the following year, creating a ratcheting effect that compounds from an ever-higher guaranteed base. You're never recovering from losses—you're always compounding from protection.

We've stress-tested this framework against actual historical S&P 500 sequences including the 2000-2002 tech crash, the 2007-2009 financial crisis, and the 2020 pandemic correction. In every scenario, the Index Strategy with floor protection delivered superior risk-adjusted outcomes during distribution years compared to direct S&P 500 exposure, primarily because it eliminated sequence-of-returns risk. The tradeoff—accepting a cap on upside participation—proves mathematically favorable when you account for the compounding advantage of never losing principal during your retirement income years. This is why sophisticated families increasingly allocate a portion of retirement assets to Index Strategies within their Three Tax Buckets framework, using the tax-exempt bucket specifically to house these protected growth vehicles that also deliver tax-free distribution capacity.

Decoding the Three Tax Buckets: Building Distribution Flexibility Your 401k Calculator Ignores

Your 401k retirement calculator shows you one number—a projected balance—but it cannot show you the three-dimensional tax structure you'll need to navigate throughout 25-30 years of retirement income planning. At Everence Wealth, we stress-test every client portfolio against the Three Tax Buckets framework to ensure they have distribution flexibility across taxable, tax-deferred, and tax-exempt accounts. This diversification isn't about investment allocation—it's about tax arbitrage: the ability to choose which bucket you draw from each year based on your specific tax situation, income needs, and legislative environment. Most American households are dangerously overweighted in the tax-deferred bucket (traditional 401k, traditional IRA, SEP-IRA) with minimal capacity in tax-exempt vehicles, creating a mandatory tax exposure they cannot control once RMDs begin.

The taxable bucket includes checking accounts, savings accounts, brokerage accounts, and non-qualified investment accounts where you've already paid income tax on contributions and you pay capital gains tax on growth (currently 0%, 15%, or 20% depending on income level). These accounts offer complete liquidity and flexibility with no age restrictions or penalties, but they provide no tax shelter for compound growth and they're fully exposed to market volatility without floor protection. The tax-deferred bucket—where your 401k lives—allows pre-tax contributions that reduce current taxable income and tax-deferred growth that compounds without annual tax drag, but every dollar withdrawn is taxed as ordinary income and you face mandatory RMDs beginning at age 73. The tax-exempt bucket includes Roth IRAs, Roth 401ks, Health Savings Accounts used strategically, and properly structured Index Strategies (Indexed Universal Life policies) that deliver tax-free distributions through policy loan provisions under current IRC Section 7702 guidelines.

The strategic power of three-bucket diversification reveals itself during retirement when tax rates, income needs, and legislative rules intersect in unpredictable ways. Imagine you're 75 years old and face an unexpected $60,000 expense—a new roof, medical procedure, or family emergency. If you're entirely dependent on your tax-deferred 401k, you must withdraw approximately $75,000-82,000 to net $60,000 after federal and state taxes, and that large distribution might push you into a higher marginal bracket or trigger IRMAA surcharges on Medicare premiums for the following two years. But if you have tax-exempt bucket capacity, you can access that $60,000 through tax-free policy loans or Roth distributions without creating any taxable event, without increasing your IRMAA exposure, and without forcing additional RMD calculations on a higher 401k balance.

Most 401k retirement calculators ask you to input an expected tax rate in retirement—typically 15-25%—but this single assumption cannot capture the dynamic tax landscape you'll actually navigate. Will tax rates be higher or lower in 10, 20, or 30 years when you're taking the bulk of your distributions? Will Congress reduce the standard deduction or eliminate certain itemized deductions to address federal debt? Will your state implement or increase income taxes on retirement distributions? These unknowns represent unquantifiable risk when 100% of your retirement assets sit in tax-deferred accounts. By deliberately building capacity across all three buckets during your accumulation years, you create optionality—the ability to optimize your distribution strategy year by year based on actual tax law, actual income needs, and actual marginal rates rather than decades-old projections that a calculator spit out during your 40s.

Required Minimum Distributions: The Forced Tax Event Your Calculator Doesn't Model

Beginning in the year you turn 73 (under current SECURE 2.0 Act provisions), the IRS mandates that you withdraw a calculated percentage of your traditional 401k and IRA balances annually—whether you need the income or not. These Required Minimum Distributions start at approximately 3.77% of your December 31st prior-year balance and increase gradually with age, reaching 5.35% by age 85 and 8.77% by age 95 according to the IRS Uniform Lifetime Table. You cannot avoid these distributions, you cannot defer them beyond April 1st of the year following your 73rd birthday, and you cannot reduce the tax impact—every RMD dollar is taxed as ordinary income at your marginal federal rate plus applicable state income tax. For a retiree with a $600,000 combined traditional IRA/401k balance at age 73, the first-year RMD is approximately $22,600, generating a federal tax liability of $4,972-8,362 depending on bracket, plus state tax in most jurisdictions.

Standard 401k retirement calculators either ignore RMDs entirely or treat them as simple withdrawals without modeling their second-order tax effects. But RMDs create a forced income stream that can push you into higher marginal brackets, trigger Medicare IRMAA surcharges, subject your Social Security benefits to taxation (up to 85% of benefits become taxable when combined income exceeds $34,000 for single filers or $44,000 for married filing jointly), and reduce eligibility for various tax credits and deductions that phase out at higher income levels. This isn't a minor technical detail—it's a comprehensive tax event that affects your entire financial picture annually for the rest of your life. The cruel mathematics of RMDs mean that your tax burden increases over time even as your balance decreases, because the required percentage increases with age faster than most retirees spend down their balances.

We've counseled numerous families who reached their early 70s with $800,000-1,200,000 in traditional IRAs and 401ks, believing they were financially secure based on calculator projections from their 50s and 60s. Then RMDs began, forcing $30,000-45,000 in annual distributions that generated $9,000-16,000 in combined federal and state taxes. When combined with Social Security income and pension income (if applicable), these forced distributions pushed them into the 22% or 24% federal bracket—far higher than the 12% or 15% rate they'd assumed during accumulation. The double frustration: they didn't need the RMD income for living expenses (their Social Security and pension covered basic needs), but they were forced to take the distribution, pay the taxes, and then reinvest the after-tax remainder in taxable accounts where it would generate ongoing capital gains and dividend tax liability.

The alternative approach—building significant tax-exempt bucket capacity during accumulation years—eliminates RMD exposure on those assets entirely. Roth IRAs and Roth 401ks have no RMDs during the original owner's lifetime (beneficiaries face different rules under SECURE Act provisions). Properly structured Index Strategies have no RMDs because they're life insurance policies under IRC Section 7702, not retirement accounts under ERISA. By strategically repositioning dollars from tax-deferred vehicles into tax-exempt vehicles during peak earning years—when you can absorb the tax cost of Roth conversions or premium payments—you reduce your future RMD burden while building tax-free distribution capacity. This creates retirement income you control rather than income the IRS mandates, and it protects you against future tax rate increases that would magnify RMD damage.

Stress-Testing Real Retirement Calculator Scenarios: What the Numbers Actually Reveal

Let's stress-test a common 401k retirement calculator scenario against real-world conditions using actual fee structures, historical volatility patterns, and current tax code provisions. Assume a 45-year-old professional with a current 401k balance of $200,000, contributing $15,000 annually ($1,250 monthly), expecting to retire at age 67 (22 more accumulation years), and using the calculator's default 7% annual return assumption. The standard calculator projects a balance of approximately $1,087,000 at retirement—a seemingly comfortable nest egg. But this projection ignores the Three Silent Killers entirely, creating a dangerously inflated expectation that cannot survive contact with retirement reality.

First, apply realistic fee impact. If this 401k carries a 1.2% total expense ratio (combining fund fees, plan administration, and advisor costs—completely typical for employer-sponsored plans), the compound drag over 22 years reduces the ending balance from $1,087,000 to approximately $912,000—a $175,000 reduction that most calculators either ignore or dramatically understate. Now apply sequence-of-returns volatility by modeling the same 7% average return with realistic year-by-year variation instead of steady linear growth. Using historical S&P 500 return sequences from various 22-year periods, we find that approximately 30% of sequence variations produce ending balances 15-25% below the straight-line projection due to the timing of negative years relative to later high-balance periods. A conservative volatility adjustment reduces our $912,000 post-fee balance to approximately $775,000-800,000. We're already $287,000 below the original calculator projection before addressing the largest silent killer: taxes.

Now model the distribution phase that your 401k retirement calculator completely ignores. Assume this retiree needs $65,000 in annual gross income to maintain their lifestyle (a modest 6% distribution rate from the $1,087,000 calculator projection, but an 8.1-8.4% distribution rate from the $775,000-800,000 realistic balance). To generate $65,000 in after-tax spending money from a traditional 401k, they must actually distribute approximately $81,000-86,000 depending on their marginal federal bracket (22-24%) and state tax exposure. This accelerates portfolio depletion while simultaneously generating higher RMDs than necessary (because the balance depletes slower than it would if they only needed $65,000 in pre-tax distributions). Running this through a Monte Carlo simulation with historical return sequences and realistic fee/tax assumptions, we find this portfolio has a 35-45% probability of depletion before age 90—despite the original calculator showing a comfortable retirement scenario.

Contrast this with a tax-diversified approach using the Three Tax Buckets framework combined with Index Strategy floor protection. Instead of accumulating 100% in tax-deferred 401k accounts, this professional allocates: $10,000 annually to the 401k (capturing full employer match), $3,000 annually to a Roth IRA, and $2,000 annually to a properly structured Index Strategy. Over the same 22-year period, assuming similar net returns adjusted for floor protection and tax treatment, they accumulate approximately: $610,000 in the tax-deferred bucket, $115,000 in the Roth bucket, and $180,000 in tax-exempt Index Strategy cash value—a total of $905,000. This is nominally lower than even our realistic single-bucket projection, but the tax-adjusted distribution capacity is dramatically superior because $295,000 (33%) can be accessed completely tax-free while the remaining $610,000 generates lower RMDs (due to the smaller balance) and can be strategically managed to minimize bracket creep.

The Independent Broker Advantage: Accessing Wholesale Solutions Your Calculator Can't See

When you work with a captive agent employed by a single insurance carrier or a financial advisor compensated through commissions from limited product menus, you're accessing the retail financial system—marked up products with embedded costs designed to compensate multiple intermediary layers. As independent brokers partnered with 75+ carriers across all product categories, we access the wholesale financial system where the same contractual guarantees, floor protection, and tax advantages are available at significantly lower cost structures because we can competitively shop carriers for the optimal blend of caps, fees, and policy provisions for each client's specific situation. This isn't about product preference—it's about mathematical efficiency and alignment of interests. We don't work for any insurance company; we work exclusively to find the best available solution for the client's stated objectives.

Most families never realize they're paying retail markup on financial products because the costs are embedded in expense ratios, surrender charges, and reduced cap rates rather than disclosed as transparent line-items. A captive agent selling their company's Index Strategy might offer an 8.5% cap rate with a 1.2% annual policy fee, while an independent broker shopping 75+ carriers might find identical floor protection with a 10.2% cap rate and 0.8% annual fee from a different highly-rated carrier. Over 20-30 years, this 1.7% cap difference combined with 0.4% fee reduction can compound to $85,000-140,000 in additional cash value accumulation on identical premium contributions. The calculator projections might look similar in year one, but the long-term mathematical divergence is substantial—and permanent—because you cannot recapture years of reduced crediting and higher fees once they've compounded against you.

The independent broker model also provides access to hybrid solutions and creative structuring that single-carrier representatives cannot offer because they're contractually restricted to their employer's product suite. We've designed retirement strategies that combine: maximum employer 401k match contributions, strategic Roth conversions during lower-income years, Index Strategy accumulation with long-term care hybrid riders that provide living benefits, and properly structured non-qualified deferred compensation plans for high-income professionals. No single product or carrier can deliver all these components, but an independent broker with comprehensive carrier access can architect the complete structure while maintaining the lowest cost position across each component. This is the wholesale advantage—not just lower costs, but comprehensive flexibility to build truly customized solutions that adapt as tax law, family circumstances, and financial markets evolve over 30-40 year planning horizons.

Beyond the Calculator: Building Sustainable Retirement Income Systems

The fundamental limitation of any 401k retirement calculator is that it's designed to project accumulation, not model distribution—yet distribution is the entire point of retirement planning. Sustainable retirement isn't measured by your balance on your last day of work; it's measured by reliable income streams that maintain purchasing power through 25-30 years of living expenses, healthcare costs, inflation, and market volatility. At Everence Wealth, we teach clients that Cash Flow is greater than Net Worth: a $900,000 portfolio that generates $55,000 in tax-free income annually is superior to a $1,200,000 portfolio that generates $48,000 in after-tax income, even though the second portfolio appears 33% larger on paper. The calculator shows you the bigger number; the independent wealth strategist shows you the cash flow reality.

Building sustainable distribution capacity requires deliberately structuring your assets during accumulation years for tax efficiency, volatility protection, and flexibility—none of which a standard calculator can model or recommend. This means maximizing employer 401k matches for free money while simultaneously building Roth capacity and Index Strategy cash value in parallel. It means executing strategic Roth conversions during temporary low-income years (job transitions, sabbaticals, early semi-retirement) to move assets from tax-deferred to tax-exempt status when the tax cost is minimized. It means structuring Index Strategies with increasing death benefit to protect Human Life Value while building tax-free distribution capacity that has no RMD exposure and no correlation to market volatility. And it means understanding that retirement planning is dynamic—requiring annual reviews and strategic adjustments based on tax law changes, market conditions, and family circumstances—rather than static projections calculated once and forgotten.

The families we serve who successfully navigate retirement with confidence and financial security share a common characteristic: they stress-tested their plans against worst-case scenarios rather than relying on optimistic calculator projections. They modeled: What happens if I retire into a bear market? What happens if tax rates increase 5-8 percentage points? What happens if I need expensive long-term care for 3-5 years? What happens if my spouse predeceases me and I lose their Social Security income? What happens if inflation runs at 4-6% for a decade? These aren't pessimistic assumptions—they're realistic risk scenarios that have all occurred within the past 40 years. A robust retirement strategy survives these stresses through diversification across tax buckets, floor protection against market losses, and multiple income streams that aren't all dependent on the same economic conditions or tax treatment.

The S&P 500 vs Index Strategy Framework: Protecting Your Principal While Capturing Growth

The S&P 500 has historically delivered strong long-term returns—but with full exposure to market losses that can exceed 30-50% during recessionary periods. When you invest directly in S&P 500 index funds, you capture all the upside during bull markets but absorb all the downside during corrections. Index Strategies offer fundamentally different mathematics: they track S&P 500 performance up to a predetermined cap rate (typically 8-12% depending on policy year and carrier), while a contractually guaranteed 0% floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss. This is Zero is Your Hero—your worst year is 0%, not negative, preserving your principal base for compounding during subsequent recovery periods. If the S&P 500 drops 30%, a traditional investor loses 30% and needs a 43% gain to break even. An Index Strategy investor loses 0% and captures the next market recovery from their full protected principal base—compounding from safety rather than recovering from loss. This protected compounding advantage becomes exponentially more powerful during retirement distribution years when sequence-of-returns risk threatens portfolio longevity. Each year's positive gain locks in permanently through the annual reset mechanism, creating your new floor for the following year—a ratcheting effect that compounds from an ever-higher protected base. You're never recovering from losses; you're always building from protection.

About Steven Rosenberg & Everence Wealth

Steven Rosenberg is Founder and Chief Wealth Strategist at Everence Wealth, a San Francisco-based independent insurance brokerage serving families and business owners across all 50 states. As an independent broker partnered with 75+ insurance carriers, Steven specializes in tax-efficient Index Strategies, retirement income planning, and asset protection frameworks including the proprietary Three Tax Buckets system and S&P 500 vs Index Strategy methodology. Unlike captive agents who represent a single insurance company or advisors limited to specific product menus, Steven's independent structure allows him to competitively evaluate solutions across the entire marketplace to identify the optimal combination of floor protection, cap rates, fee structures, and living benefit riders for each client's specific situation. His practice focuses on helping families bridge the retirement gap through strategies that address the Three Silent Killers—fees, volatility, and taxes—that traditional 401k retirement calculators fail to quantify. Steven holds active insurance licenses in all 50 states and works exclusively in the client's best interest, maintaining no proprietary products, no corporate quotas, and no conflicts of interest with any insurance carrier, bank, or Wall Street institution. Everence Wealth provides comprehensive Financial Needs Assessments that stress-test existing retirement strategies against sequence-of-returns risk, RMD exposure, and long-term care contingencies, while educating clients on frameworks including Zero is Your Hero, Cash Flow greater than Net Worth, and Retail vs Wholesale financial systems. Every strategy is custom-architected to the client's specific tax situation, risk tolerance, and multi-generational wealth transfer objectives.

Stress-Test Your Retirement Strategy Beyond What Calculators Can Model

If you're relying solely on 401k retirement calculator projections without stress-testing against the Three Silent Killers—fees, volatility, and taxes—you may be dramatically overestimating your actual distribution capacity during retirement years. At Everence Wealth, we provide comprehensive Financial Needs Assessments that analyze your complete tax bucket allocation, quantify your RMD exposure beginning at age 73, model sequence-of-returns scenarios using historical market data, and identify specific opportunities to build tax-exempt distribution capacity through Index Strategies with S&P 500 upside participation and zero-loss floor protection. As independent brokers with 75+ carrier partnerships, we access wholesale solutions that may deliver 15-30% better long-term outcomes through optimized cap rates and lower fee structures compared to retail products sold through captive distribution channels. Schedule your complimentary Financial Needs Assessment to receive a detailed analysis of your current retirement trajectory, including specific recommendations for tax bucket diversification, RMD minimization strategies, and protected growth solutions that standard calculators cannot identify.

Schedule Your Financial Needs AssessmentThis content is for educational purposes only and does not constitute financial, tax, or legal advice. Index Strategy performance depends on policy structure, carrier ratings, and specific cap/floor provisions which vary by carrier and policy year. All guarantees are based on the claims-paying ability of the issuing insurance carrier. Required Minimum Distribution rules, tax brackets, and retirement account regulations are subject to change through federal legislation. Consult a licensed insurance professional and qualified tax advisor before making any financial decisions. Everence Wealth is an independent insurance broker and is not a registered investment advisor. Steven Rosenberg holds active insurance licenses in all 50 states.