A Financial Needs Assessment (FNA) is a comprehensive evaluation of your current financial situation, future goals, and potential risks. Through Everence Wealth's FNA process, we analyze income protection, retirement readiness, tax exposure across the Three Tax Buckets, and retirement gap vulnerabilities using Index Strategies with S&P 500-linked growth and zero-floor protection to build sustainable, tax-efficient wealth.

Most families approach retirement with a dangerous assumption: that their current savings trajectory will be enough. According to the Federal Reserve's Survey of Consumer Finances, the median retirement account balance for families approaching retirement is just $164,000—a figure that represents less than four years of typical retirement spending. The real challenge isn't just accumulation—it's understanding whether your current financial strategy can survive the Three Silent Killers: fees, volatility, and taxes. Without a comprehensive Financial Needs Assessment, you're navigating retirement with an incomplete map.

A Financial Needs Assessment (FNA) is fundamentally different from the typical portfolio review offered by commission-driven advisors or bank representatives. While conventional financial planning often focuses narrowly on asset allocation and product sales, a true FNA examines your entire financial ecosystem: income protection, tax exposure across all three tax buckets, retirement gap analysis, estate planning vulnerabilities, and the mathematical reality of how market volatility destroys compounding. We've seen portfolios that looked healthy on paper crumble under stress-testing because families never accounted for sequence-of-returns risk or the compounding damage of a 30-year fee drain.

As an independent broker with access to 75+ carrier partnerships, we conduct Financial Needs Assessments that prioritize one thing: your actual needs, not product quotas. This means examining whether you're overexposed to tax-deferred accounts that will trigger Required Minimum Distributions, whether your Human Life Value is properly protected, and whether Index Strategies with S&P 500 participation and zero-loss floors should replace or complement your current retirement vehicles. The FNA process reveals gaps that Wall Street's retail financial system systematically ignores—because those gaps aren't profitable for them to solve.

What Does a Financial Needs Assessment Actually Measure?

A comprehensive Financial Needs Assessment evaluates seven critical dimensions of your financial life. First, it calculates your Human Life Value—the present value of your future earning potential. This is the most underinsured asset in any financial plan, yet most families focus exclusively on their existing net worth while ignoring the income engine that creates it. If you earn $150,000 annually and have 20 working years remaining, your Human Life Value exceeds $3 million before adjusting for raises and inflation. Protecting that asset through proper income replacement strategies is foundational.

Second, an FNA stress-tests your retirement projections against realistic market conditions. This includes sequence-of-returns analysis—the mathematical proof that market timing matters enormously in retirement. If you retire into a bear market and begin withdrawing from a depleted portfolio, you can permanently impair your retirement income even if markets eventually recover. We model this using historical S&P 500 data, showing how a traditional investor who retired in 2000 or 2008 faced a decade of essentially zero returns while simultaneously drawing down principal. An Index Strategy with a zero floor protects against this exact scenario: you participate in S&P 500 growth up to a cap rate, but your worst year is always 0%, not negative.

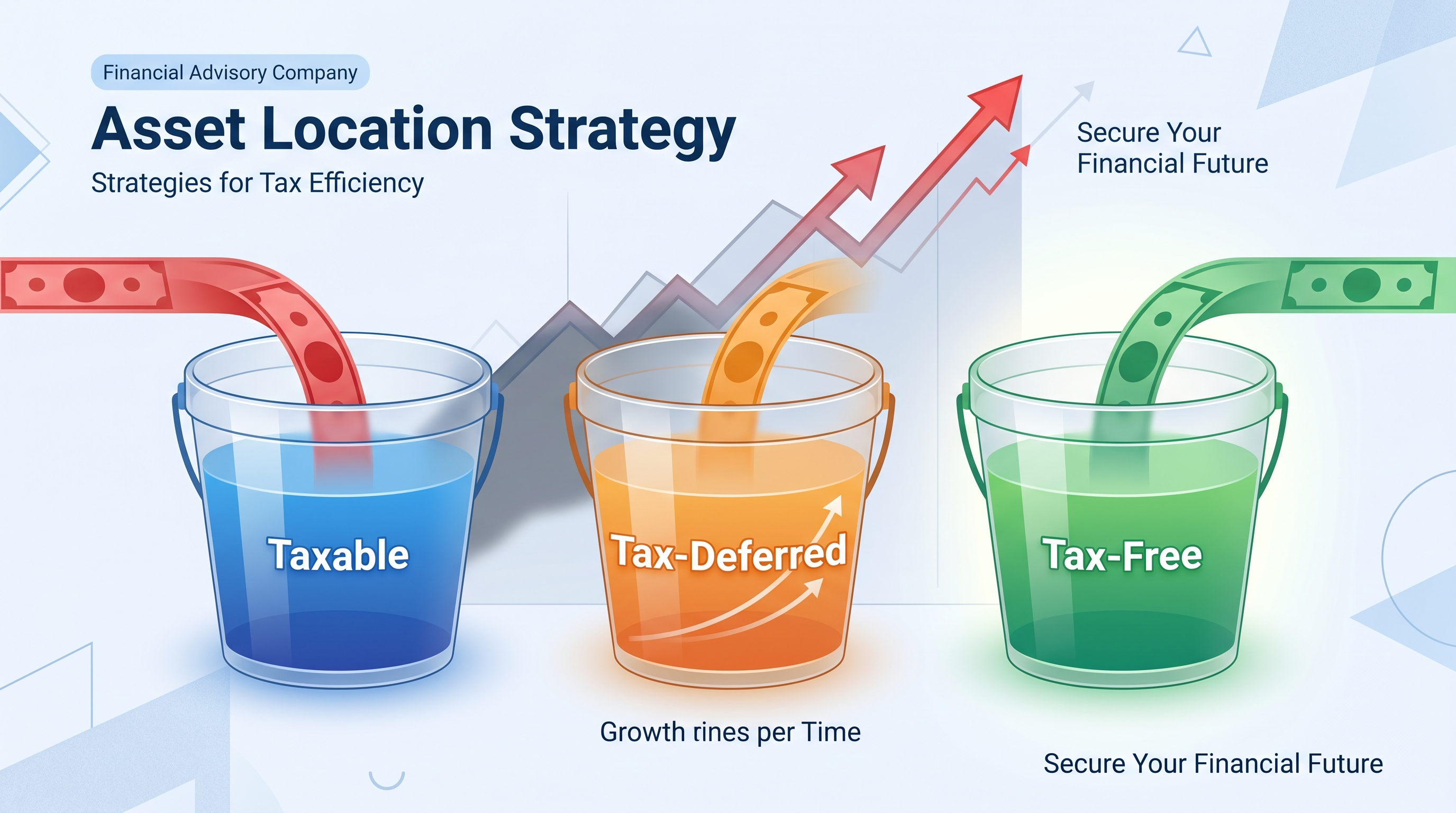

Third, we analyze your Three Tax Buckets exposure: taxable accounts, tax-deferred accounts like 401(k)s and Traditional IRAs, and tax-exempt vehicles like Roth IRAs and Index Strategies. Most families discover they're dangerously overweight in tax-deferred accounts—meaning they've deferred taxes into an unknown future tax environment and guaranteed that Required Minimum Distributions will force taxable income whether they need it or not. Balancing across all three buckets creates flexibility and reduces lifetime tax exposure.

Fourth, the FNA identifies fee drag across your entire portfolio. A 1.5% annual fee might sound modest, but compounded over 30 years it can consume 40% or more of your total returns. Using the Rule of 72, we can quickly estimate that at a 1.5% annual cost, your fees double every 48 years—meaning half of your portfolio's growth potential is transferred to financial institutions rather than compounding for your benefit. Index Strategies typically carry lower internal costs than managed mutual funds, and because growth isn't taxed annually, you compound on your full balance rather than after-tax returns.

How Is a Financial Needs Assessment Different from a Portfolio Review?

Portfolio reviews focus on what you own. Financial Needs Assessments focus on what you need. This distinction is critical. A portfolio review conducted by a bank advisor or brokerage representative typically evaluates asset allocation, rebalances positions, and suggests products that generate commissions or management fees. These reviews rarely challenge the fundamental structure of your financial plan or reveal conflicts of interest embedded in the products you already own. Because these advisors work for institutions with product quotas and revenue targets, their recommendations are constrained by what their employer wants to sell.

By contrast, an independent broker conducting an FNA has no institutional allegiance. We partner with 75+ carriers, meaning we can objectively compare solutions across the entire marketplace rather than being limited to proprietary products. This independence allows us to ask uncomfortable questions: Is your 401(k) charging excessive fees? Are you overexposed to market risk as you approach retirement? Have you stress-tested your plan against a 2008-style downturn or a prolonged flat market like 2000–2010? Would an Index Strategy with S&P 500 participation and downside protection better serve your risk tolerance than continuing to expose 100% of your retirement savings to full market volatility?

The FNA process also incorporates cash flow analysis, not just net worth snapshots. We've worked with families who had impressive account balances but couldn't generate sustainable retirement income without liquidating assets during down markets—a recipe for sequence-of-returns disaster. Cash Flow > Net Worth is one of our core frameworks because retirement isn't about how much you have; it's about how much reliable, tax-efficient income you can generate for 25–35 years. An FNA models this income across multiple tax scenarios, inflation environments, and market conditions to identify vulnerabilities before you retire.

What Questions Should You Expect During a Financial Needs Assessment?

Expect detailed questions about income, expenses, debt, insurance coverage, estate planning documents, and retirement timing. We begin by understanding your current cash flow: what you earn, what you spend, and what you save. This reveals your savings rate and whether you're on track to meet retirement goals. We then examine your debt structure: mortgage balances, interest rates, and payoff timelines. High-interest debt compounds against you at the same rate Index Strategies compound for you, so debt strategy is inseparable from wealth strategy.

Next, we inventory all existing financial accounts: 401(k)s, IRAs, taxable brokerage accounts, savings accounts, real estate equity, and business interests. For each account, we document fees, tax treatment, liquidity constraints, and whether Required Minimum Distributions will apply. This inventory often reveals redundancy—families holding five different IRAs across old employers, each charging separate fees and requiring separate tax reporting. Consolidation can reduce costs and simplify management, but only when done strategically to avoid tax traps.

We also assess your insurance coverage across four categories: life, disability, long-term care, and liability. Life insurance is evaluated not just for death benefit adequacy but for living benefits—the ability to access the death benefit if you're diagnosed with a chronic, critical, or terminal illness. Disability insurance is tested against your actual living expenses, not the arbitrary coverage your employer provides. Long-term care risk is quantified by examining family health history and state-specific care costs. Liability protection includes umbrella policies and whether your asset structure exposes you to creditor risk.

Finally, we discuss retirement timing, legacy goals, and risk tolerance. When do you want to retire? What does retirement look like—full stop or phased transition? Do you want to leave an inheritance, and if so, in what form? How did you react emotionally during the 2008 financial crisis or the March 2020 drawdown? These answers shape strategy. Someone who panicked and sold in 2008 needs downside protection more than someone who stayed invested. Someone who wants to leave a tax-free legacy to children should prioritize Index Strategies and life insurance over tax-deferred accounts that pass with embedded tax liabilities.

How the S&P 500 vs Index Strategy Framework Shapes Your FNA

One of the most important comparisons we make during a Financial Needs Assessment is between traditional S&P 500 exposure and Index Strategy positioning. The S&P 500 has historically delivered strong long-term returns—approximately 10% annualized over the past several decades—but with full exposure to market losses. During the 2008 financial crisis, the S&P 500 dropped 38.5%. During the early 2000s tech crash, it fell over 49% from peak to trough. During March 2020, it declined 34% in just 23 trading days. Each time, investors holding traditional stock portfolios experienced those full losses.

Index Strategies track S&P 500 performance up to a cap rate, while a guaranteed floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss. If the S&P 500 drops 30%, a traditional investor loses 30% and needs a 43% gain just to break even. An Index Strategy investor loses 0% and captures the next market recovery from their full principal—compounding from a protected base. This is what we call Zero is Your Hero. Your worst year is 0%, not negative, which fundamentally changes the mathematics of long-term compounding.

During the FNA, we model this difference using historical data. We show what would have happened to two investors who each started with $500,000 in 2000: one in a traditional S&P 500 index fund with full volatility exposure, and one in an Index Strategy with a 0% floor and a 10% cap. While the traditional investor would have experienced two brutal bear markets (2000–2002 and 2007–2009) and the emotional trauma of watching their account lose half its value twice, the Index Strategy investor would have avoided all downside while still participating in recovery years up to the cap. Over the full period, the Index Strategy's protected compounding often produces comparable or superior results—with dramatically less volatility and zero years of negative returns.

This comparison is central to the FNA because it reframes risk. Most families assume higher returns require higher risk. But Index Strategies demonstrate that strategic risk management—giving up unlimited upside in exchange for eliminating downside—can produce better risk-adjusted returns and far better emotional sustainability. We've never met a retiree who regretted avoiding a 30% loss. We've met many who regretted experiencing one and being forced to delay retirement or reduce their lifestyle as a result.

S&P 500 vs Index Strategy: Protected Participation

The S&P 500 has historically delivered strong long-term returns—but with full exposure to market losses. Index Strategies track S&P 500 performance up to a cap rate, while a guaranteed floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss. If the S&P 500 drops 30%, a traditional investor loses 30% and needs a 43% gain just to break even. An Index Strategy investor loses 0% and captures the next market recovery from their full principal—compounding from a protected base. This is what we call Zero is Your Hero. During the 2008 financial crisis, traditional investors needed 5–7 years to recover their losses. Index Strategy holders maintained their principal and began capturing gains immediately when the market turned. This annual reset mechanism locks in gains each year, protecting the new higher base from future downturns. Over a 30-year retirement, avoiding even two or three major bear markets can make the difference between running out of money and leaving a legacy.

Why Independent Brokers Conduct Better Financial Needs Assessments

The quality of your Financial Needs Assessment is directly tied to the independence of the professional conducting it. Advisors employed by banks, wirehouses, or insurance companies operate under inherent conflicts of interest. They're incentivized—through commissions, bonuses, and employment requirements—to recommend their employer's proprietary products regardless of whether those products are optimal for you. We've reviewed countless portfolios where clients were sold high-fee annuities, load mutual funds, or whole life policies that generated huge commissions but delivered mediocre performance.

As an independent broker, I'm not employed by any insurance company, bank, or Wall Street institution. I'm compensated by clients for providing objective advice and by carriers when clients choose to implement strategies—but with access to 75+ carriers, I have no incentive to favor one over another. My loyalty is to finding the best solution, not meeting a product quota. This independence is especially critical when evaluating Index Strategies, because carrier features, cap rates, and fees vary significantly. An independent broker can compare all options and select the one that best fits your specific situation.

Independence also means we can challenge conventional wisdom. If your 401(k) has high fees and limited investment options, we can say so—and explore alternatives like rolling old 401(k)s into IRAs with broader Index Strategy access. If your advisor is charging 1.5% annually to manage a passive index portfolio you could replicate yourself for 0.05%, we can quantify that cost over 30 years and show you the damage. If your estate plan leaves tax-deferred IRA assets to your children, triggering the 10-year distribution rule and forcing them into their highest tax brackets, we can redesign that legacy using tax-free life insurance death benefits instead.

The FNA conducted by an independent broker is a rigorous, best-interest-aligned process without the regulatory constraints that limit what registered investment advisors can recommend. We can objectively evaluate insurance solutions, tax strategies, and alternative structures that RIAs often can't or won't discuss because they fall outside their typical product universe. This comprehensive approach produces better outcomes because it draws from the full toolkit of financial strategies rather than being limited to what one institution offers.

What Happens After Your Financial Needs Assessment?

After completing your FNA, we deliver a detailed written analysis covering every dimension of your financial life. This report includes a retirement gap analysis showing the difference between your current trajectory and your retirement income goal. If there's a gap, we model different strategies to close it: increasing savings rates, reallocating assets to more efficient vehicles like Index Strategies, optimizing Social Security claiming strategies, or reducing fee drag through lower-cost alternatives.

The report also includes a tax projection showing your estimated lifetime tax liability under current law and under various scenarios. We model what happens if tax rates increase, if Required Minimum Distributions push you into higher brackets, or if state taxes change. We then illustrate how reallocating a portion of tax-deferred savings into tax-exempt Index Strategies can reduce total taxes paid over your lifetime by hundreds of thousands of dollars. This is the Three Tax Buckets framework in action: balancing across taxable, tax-deferred, and tax-exempt accounts to give you control and flexibility.

We provide specific recommendations ranked by priority and impact. High-priority actions might include replacing an underfunded term life policy, rolling over an old 401(k) with high fees, or establishing an Index Strategy to create tax-free retirement income. Medium-priority actions could include rebalancing asset allocation, updating estate documents, or increasing 401(k) contributions to capture full employer match. Lower-priority items might include optimizing credit card rewards strategies or refinancing a mortgage if rates drop.

Critically, the FNA includes implementation support. We don't just hand you a report and wish you luck. If you choose to move forward with an Index Strategy, we handle carrier selection, application paperwork, underwriting coordination, and policy setup. If you need estate planning documents updated, we connect you with attorneys who understand tax-efficient wealth transfer. If you need tax projections refined, we coordinate with CPAs who specialize in retirement tax planning. The FNA is the diagnostic; implementation is the treatment. Both are essential.

About Steven Rosenberg & Everence Wealth

Steven Rosenberg is the Founder and Chief Wealth Strategist at Everence Wealth, a San Francisco-based independent financial firm specializing in Index Strategies, tax-efficient retirement planning, and wealth protection for families, business owners, and professionals across all 50 states. As an independent broker with partnerships across 75+ insurance carriers, Steven works exclusively in the client's best interest—not for any insurance company, bank, or Wall Street institution. His approach is rooted in transparent, math-based analysis of the Three Silent Killers—fees, volatility, and taxes—and how Index Strategies with S&P 500-linked growth and zero-floor protection solve for all three simultaneously. Steven's expertise includes retirement gap analysis, Three Tax Buckets framework implementation, Human Life Value assessment, sequence-of-returns risk mitigation, and estate planning using tax-free life insurance strategies. His educational content is designed to expose the inefficiencies of retail financial products and guide families toward wholesale-priced, institutionally sound wealth-building strategies. Everence Wealth's Financial Needs Assessment process has helped hundreds of families identify hidden vulnerabilities, reduce lifetime tax exposure, and build sustainable retirement income that doesn't depend on market timing or risk excessive principal during down markets. Every recommendation is backed by regulatory guidelines from the IRS, Department of Labor, and state insurance departments, and every strategy is stress-tested against historical market conditions to ensure it can withstand real-world volatility.

Schedule Your Comprehensive Financial Needs Assessment

If you've never had a true Financial Needs Assessment—one conducted by an independent broker with access to 75+ carriers and no institutional conflicts of interest—you're navigating retirement with incomplete information. Our FNA process examines your income protection, retirement gap, tax exposure across the Three Tax Buckets, fee drag, sequence-of-returns risk, and estate planning vulnerabilities. We stress-test your current strategy against historical market conditions and model how Index Strategies with S&P 500 participation and zero-loss floors can protect and enhance your retirement. There's no cost for the assessment, no obligation to implement, and no pressure to buy products. We simply show you the math and let you decide. Schedule your Financial Needs Assessment today and discover whether your current retirement plan can actually deliver the future you're counting on.

Schedule Your Financial Needs AssessmentThis content is for educational purposes only and does not constitute financial, tax, or legal advice. Index Strategy performance depends on carrier-specific cap rates, participation rates, and fees, which vary and are not guaranteed. S&P 500 historical performance is not indicative of future results. Consult a licensed insurance professional and tax advisor before making any financial decisions.