Tax-free retirement income is achieved by funding the Tax-Exempt bucket using Index Strategies that track S&P 500 performance with zero-floor protection. Unlike 401(k)s or Traditional IRAs that defer taxes, Index Strategies grow tax-deferred and distribute tax-free. Everence Wealth guides families through this approach using the Three Tax Buckets Framework to minimize lifetime tax exposure.

Most Americans spend decades saving for retirement without realizing they're building a tax time bomb. The average retiree with $500,000 in a 401(k) doesn't actually have $500,000—they have a partnership with the IRS where every withdrawal triggers ordinary income tax. At a 24% federal rate plus state taxes, that "half-million" becomes $350,000 or less after taxes. The silent partner you never invited now controls a quarter of your retirement security.

We work with families across all fifty states who discover this reality too late—often in their sixties when Required Minimum Distributions force taxable withdrawals whether they need the income or not. The frustration is palpable: they followed every rule, maximized employer matches, and deferred gratification for thirty years, only to learn they deferred taxes into their highest-need, lowest-flexibility years. This systemic flaw isn't your fault—it's the default design of employer-sponsored retirement plans that prioritize corporate tax deductions over your long-term tax efficiency.

Tax-free retirement income isn't just possible—it's mathematically superior when structured correctly through Index Strategies that participate in S&P 500 growth while protecting against market losses. By diversifying across the Three Tax Buckets and anchoring wealth in the Tax-Exempt bucket, families create sustainable cash flow without Required Minimum Distributions, without ordinary income tax, and without the volatility that destroys compounding during distribution years. This is how independent brokers with seventy-five-plus carrier partnerships build retirement strategies Wall Street doesn't advertise.

What Are the Three Tax Buckets and Why Do They Matter for Retirement Income?

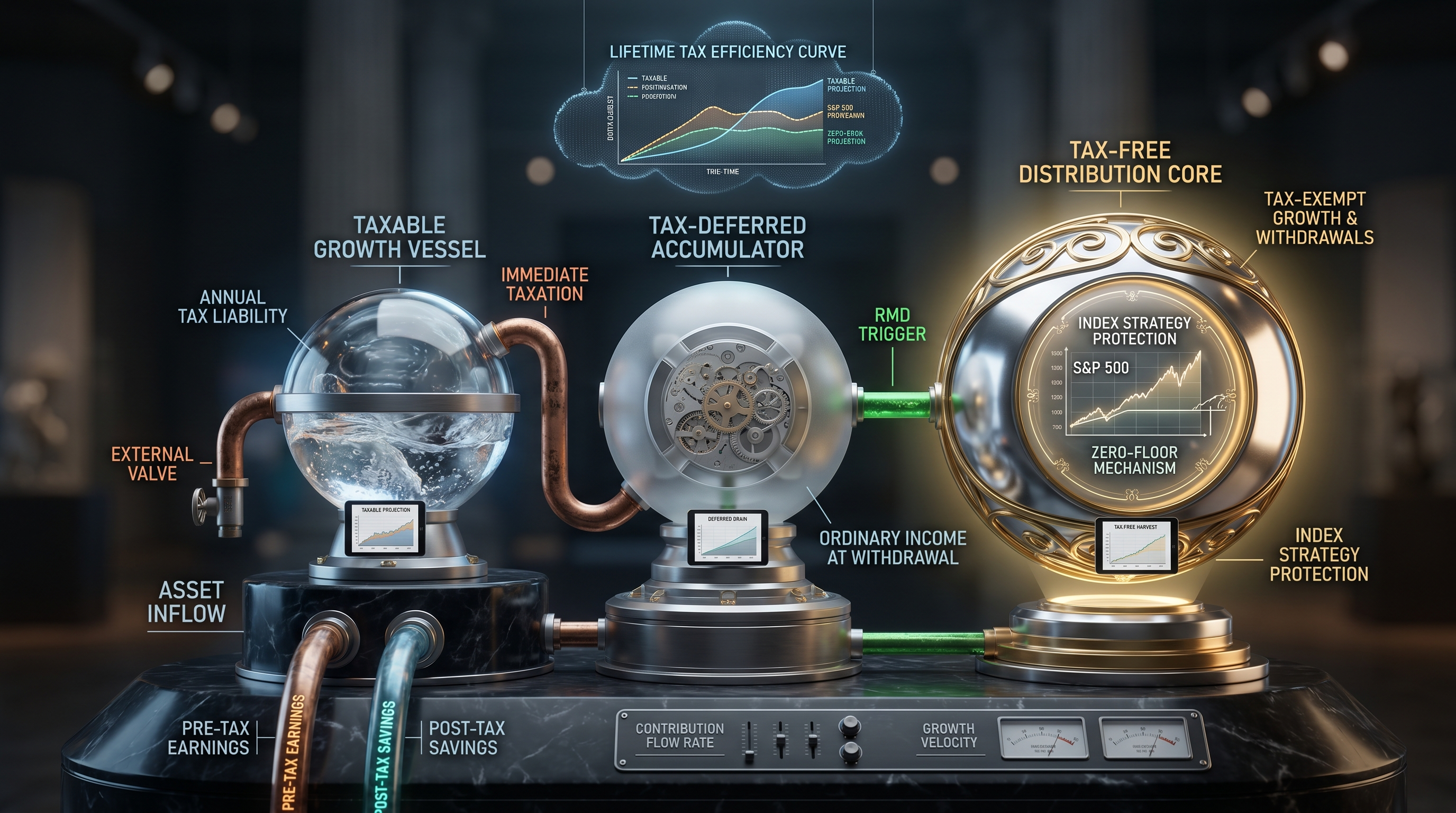

The Three Tax Buckets Framework divides all financial accounts into three categories based on how the IRS taxes distributions: Taxable, Tax-Deferred, and Tax-Exempt. Understanding which bucket holds your wealth determines your lifetime tax burden and retirement income flexibility. Most Americans over-concentrate in the Tax-Deferred bucket—401(k)s, Traditional IRAs, and 403(b)s—creating maximum tax exposure precisely when income is needed most.

The Taxable bucket includes checking accounts, savings accounts, brokerage accounts, and non-qualified investments. Every dollar of interest, dividends, and capital gains generates a tax liability in the year earned. You pay taxes annually, which reduces compounding efficiency. However, long-term capital gains receive preferential tax treatment (currently 0%, 15%, or 20% depending on income), making this bucket more efficient than Tax-Deferred for certain strategies. Liquidity is immediate, but growth is taxed continuously.

The Tax-Deferred bucket includes 401(k)s, Traditional IRAs, SEP IRAs, and most employer-sponsored plans. Contributions reduce current taxable income, and growth compounds without annual taxation—but every distribution is taxed as ordinary income at your future tax rate. Required Minimum Distributions begin at age seventy-three (as of current IRS rules), forcing taxable withdrawals even if you don't need the income. This bucket is a tax postponement strategy, not a tax elimination strategy. If tax rates rise—or if your retirement income pushes you into higher brackets—you may pay more tax later than you saved earlier.

The Tax-Exempt bucket includes Roth IRAs, Roth 401(k)s, Health Savings Accounts (used correctly), and Index Strategies structured for tax-free distributions. Contributions are made with after-tax dollars, growth compounds tax-deferred, and distributions are completely tax-free when structured properly. There are no Required Minimum Distributions during your lifetime (for Roth IRAs and Index Strategies), giving you complete control over distribution timing. This bucket provides the highest lifetime value when funded consistently and protected from market losses through zero-floor mechanisms.

Diversifying across all three buckets—rather than concentrating in Tax-Deferred—gives you tax flexibility in retirement. You can strategically withdraw from different buckets based on annual income needs, tax bracket management, and changing tax policy. Index Strategies excel in the Tax-Exempt bucket because they combine S&P 500-linked growth potential, zero-loss floor protection, and tax-free access to cash value, creating a triple advantage no traditional investment vehicle can match.

How Index Strategies Create Tax-Free Retirement Income Without Required Minimum Distributions

Index Strategies—specifically Indexed Universal Life insurance policies—function as tax-exempt wealth accumulation and distribution vehicles when structured correctly. These contracts link cash value growth to external market indices like the S&P 500, capturing upside participation up to a cap rate while guaranteeing a zero-percent floor in down years. This floor-and-cap structure is the mathematical foundation of protected compounding: you participate in market growth but never lose principal to market downturns.

When you fund an Index Strategy, premiums flow into the policy's cash value account. A portion covers the cost of insurance (the death benefit), and the remainder grows based on the performance of the chosen index, subject to cap and floor rates. If the S&P 500 gains fifteen percent and your cap is twelve percent, you earn twelve percent. If the S&P 500 drops thirty percent, you earn zero percent—not negative thirty. Your worst year is zero, not a catastrophic loss that requires years of recovery. This is what we call Zero is Your Hero.

Cash value grows tax-deferred inside the policy, just like a Traditional IRA. The critical difference emerges at distribution. Instead of taking taxable withdrawals, you access cash value through policy loans—borrowing against your own cash value at minimal or zero net cost (depending on policy design). Because loans are not considered income by the IRS, they generate zero taxable events. You receive cash flow without triggering ordinary income tax, without affecting your tax bracket, and without increasing Medicare premiums or Social Security taxation. This is tax-free retirement income in its purest form.

There are no Required Minimum Distributions with Index Strategies. You control when and how much to access, maintaining complete flexibility throughout retirement. If you need income at sixty, you can access it. If you delay until seventy-five, that's your choice. Compare this to Tax-Deferred accounts where the IRS mandates distributions starting at seventy-three, forcing taxable income whether you need it or not. For retirees with pension income, Social Security, or rental income, forced RMDs often push them into higher tax brackets, eroding wealth unnecessarily.

Index Strategies also provide a tax-free death benefit to beneficiaries, bypassing probate and income tax. Your heirs receive the full death benefit without the tax burden that accompanies inherited IRAs (which now must be distributed within ten years under the SECURE Act). This creates a multi-generational tax advantage that compounds across family wealth transfer. When you combine tax-free growth, tax-free access, tax-free legacy transfer, and zero-loss floor protection, Index Strategies become the cornerstone of the Tax-Exempt bucket.

S&P 500 vs Index Strategy: Understanding the Floor-and-Cap Tradeoff

S&P 500 vs Index Strategy: Protected Participation

The S&P 500 has historically delivered strong long-term returns—but with full exposure to market losses. Index Strategies track S&P 500 performance up to a cap rate, while a guaranteed floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss.

If the S&P 500 drops thirty percent, a traditional investor loses thirty percent and needs a forty-three percent gain just to break even. An Index Strategy investor loses zero percent and captures the next market recovery from their full principal—compounding from a protected base. This is what we call Zero is Your Hero.

Consider a real-world scenario: In 2008, the S&P 500 lost thirty-seven percent. A $500,000 portfolio dropped to $315,000. To recover to $500,000 required a fifty-nine percent gain—which took years. An Index Strategy with a zero-percent floor would have credited zero for that year, maintaining the full $500,000 base. When the market rebounded in 2009 with a twenty-six percent gain, the Index Strategy would have captured gains (subject to cap) from $500,000, not $315,000. The math advantage is undeniable: protected compounding accelerates wealth accumulation over multi-decade timeframes.

The tradeoff is the cap rate. If the S&P 500 gains thirty percent and your cap is twelve percent, you earn twelve percent—not thirty. You sacrifice unlimited upside in exchange for eliminating catastrophic downside. For retirement-focused wealth—where preservation matters more than speculation—this tradeoff is mathematically sound. Volatility kills compounding during distribution years, and sequence-of-returns risk can devastate portfolios when withdrawals occur during downturns. Index Strategies eliminate both risks.

Why the Tax-Deferred Bucket Becomes a Liability in Retirement

Tax-deferred accounts like 401(k)s and Traditional IRAs are marketed as retirement solutions, but they're better described as tax postponement vehicles with uncertain future liabilities. You receive a tax deduction today in exchange for paying ordinary income tax on every dollar withdrawn in retirement—when you may be in a higher tax bracket, facing higher tax rates, or both. This gamble assumes tax rates will be lower in retirement, an assumption increasingly challenged by fiscal realities.

Required Minimum Distributions (RMDs) turn tax deferral into forced taxation. Starting at age seventy-three, the IRS mandates annual withdrawals calculated as a percentage of your account balance. If you have $800,000 in a Traditional IRA at seventy-three, your first RMD is approximately $30,075 (using the IRS Uniform Lifetime Table). That's $30,075 of ordinary income added to Social Security, pension, rental income, or part-time work—potentially pushing you into the 24% or even 32% federal tax bracket. You didn't choose this income. The IRS chose it for you.

RMDs increase annually as the distribution percentage rises with age. By eighty-five, you're required to withdraw roughly 6.25% of your account balance—far more than the safe withdrawal rate most retirees target. If markets decline during these years, you're forced to sell assets at depressed values to meet RMD requirements, locking in losses and accelerating portfolio depletion. This is sequence-of-returns risk weaponized against your wealth.

Tax-Deferred accounts also trigger "stealth taxes" that erode wealth beyond the headline rate. RMDs count toward Modified Adjusted Gross Income (MAGI), which determines Medicare Part B and Part D premiums. Cross certain thresholds and you'll pay Income-Related Monthly Adjustment Amounts (IRMAA)—surcharges that can add hundreds of dollars per month to Medicare costs. RMDs also increase the taxable portion of Social Security benefits, potentially subjecting up to 85% of benefits to federal income tax. The cascading tax consequences of RMDs make the Tax-Deferred bucket a liability, not an asset, for many retirees.

By contrast, Index Strategy distributions via policy loans generate zero MAGI impact. Your Medicare premiums stay low. Your Social Security remains minimally taxed. Your tax bracket stays controlled. This is why independent brokers prioritize Tax-Exempt bucket strategies for clients seeking sustainable, low-tax retirement income. The goal isn't just accumulation—it's efficient, tax-controlled distribution that maximizes lifetime spending power.

How to Fund the Tax-Exempt Bucket Using Index Strategies

Funding the Tax-Exempt bucket requires intentional, disciplined strategy—not default enrollment in an employer plan. Most families allocate retirement savings exclusively to 401(k)s and IRAs because of employer matches and immediate tax deductions. While employer matches provide value, over-reliance on Tax-Deferred accounts creates concentration risk and tax inflexibility. A balanced approach funds all three buckets proportionally based on income, tax situation, and retirement timeline.

Start by maximizing Roth IRA contributions if income limits allow. For married couples filing jointly, the ability to contribute to a Roth IRA begins phasing out at $230,000 of Modified Adjusted Gross Income (as of current IRS limits). Contributions are capped at $7,000 annually ($8,000 if age fifty or older). While valuable, Roth IRAs alone rarely provide sufficient Tax-Exempt assets for a comfortable retirement. This is where Index Strategies become essential.

Index Strategies have no income limits and no contribution caps (beyond what underwriting and tax policy allow). High-income earners locked out of Roth IRAs can fund Index Strategies with five figures or more annually, building substantial Tax-Exempt cash value over decades. The key is structuring the policy for maximum cash value accumulation—minimizing insurance costs, maximizing premium allocation to cash value, and selecting competitive crediting strategies tied to indices like the S&P 500.

Work with an independent broker who has access to seventy-five-plus carriers to design a policy optimized for your tax situation and retirement timeline. Not all Index Strategies are created equal. Cap rates, floor guarantees, fee structures, and loan provisions vary significantly across carriers. An independent broker isn't locked into a single company's product lineup—we compare dozens of options to find the most efficient structure for your goals. This is the wholesale advantage over retail: you're not limited to what one company offers. You access the competitive best across the entire market.

Consider funding Index Strategies alongside—not instead of—401(k) contributions. Contribute enough to capture the full employer match (it's free money), then redirect additional retirement savings into Index Strategies for tax diversification. If you're contributing $20,000 annually to a 401(k), consider splitting it: $10,000 to capture the match, $10,000 to an Index Strategy for Tax-Exempt growth. Over thirty years, this creates balanced tax exposure and distribution flexibility that pure Tax-Deferred accumulation cannot provide.

Real-World Tax Savings: Comparing Tax-Deferred vs Tax-Exempt Retirement Income

Let's quantify the lifetime tax difference between Tax-Deferred and Tax-Exempt retirement strategies using realistic assumptions. Assume a fifty-year-old professional contributes $15,000 annually for twenty years, retiring at seventy. We'll compare a Traditional IRA (Tax-Deferred) versus an Index Strategy (Tax-Exempt), both earning an average annual return of 6.5% (accounting for Index Strategy cap rates and compounding).

In the Traditional IRA, $15,000 annual contributions over twenty years total $300,000 in cumulative contributions. At 6.5% average growth, the account grows to approximately $620,000 by age seventy. Distributions begin immediately to supplement income. Assuming a 4% withdrawal rate ($24,800 annually) and a 24% federal tax rate plus 5% state tax, total tax on each distribution is 29%—roughly $7,192 annually. Over a twenty-five-year retirement, total taxes paid exceed $179,000. The net after-tax value delivered is significantly reduced.

In an Index Strategy, the same $15,000 annual contributions over twenty years build approximately $580,000 in cash value (slightly lower due to insurance costs, though these decrease over time as the policy matures). Distributions via policy loans are tax-free. The same $24,800 annual income generates zero tax liability. Over twenty-five years, total taxes paid are zero. The difference—$179,000—represents wealth preserved for spending, legacy, or long-term care rather than transferred to the IRS.

Additionally, the Traditional IRA is subject to Required Minimum Distributions starting at seventy-three, forcing taxable income regardless of need. The Index Strategy has no RMDs—distributions occur only when you choose. If you delay distributions until seventy-five or eighty, cash value continues compounding tax-deferred, increasing available lifetime income. If you need extra income one year for travel or medical expenses, you access it tax-free without bracket creep. This flexibility is worth tens of thousands in avoided taxes and preserved wealth.

Consider also the estate planning advantage. The Traditional IRA becomes taxable income to heirs under the SECURE Act's ten-year distribution rule. If your children inherit $400,000, they'll pay ordinary income tax on every dollar distributed over ten years—potentially at their highest earning-year tax rates. The Index Strategy pays a tax-free death benefit, bypassing income tax and probate. Your legacy transfers intact, not diminished by a final tax bill. The cumulative tax savings across accumulation, distribution, and legacy transfer make Tax-Exempt strategies mathematically superior for most families focused on lifetime wealth maximization.

About Steven Rosenberg & Everence Wealth

Steven Rosenberg is the Founder and Chief Wealth Strategist at Everence Wealth, a San Francisco-based independent insurance brokerage specializing in tax-efficient retirement planning through Index Strategies. As an independent broker with partnerships across seventy-five-plus insurance carriers, Steven operates exclusively in the client's best interest—he is not employed by any insurance company, bank, or Wall Street institution. This independence allows him to design customized strategies using the most competitive products available nationwide, rather than being limited to a single company's offerings. Steven is a licensed insurance professional serving families across all fifty states, focusing on Index Strategies that combine S&P 500-linked growth potential with zero-floor protection. His expertise centers on the Three Tax Buckets Framework, helping clients reduce lifetime tax exposure by strategically diversifying across Taxable, Tax-Deferred, and Tax-Exempt accounts. He guides business owners, professionals, and retirees through complex decisions involving Required Minimum Distributions, sequence-of-returns risk, and tax-free retirement income structuring. Steven's educational approach emphasizes transparency, math-based analysis, and long-term cash flow sustainability over short-term product sales. He teaches foundational concepts like Zero is Your Hero, Cash Flow Over Net Worth, and the mechanics of S&P 500 vs Index Strategy tradeoffs, empowering families to make informed decisions aligned with their values and goals. Everence Wealth's mission is to expose the hidden costs—fees, volatility, and taxes—that Wall Street's retail financial system doesn't advertise, and to build sustainable, multi-generational prosperity through independent, wholesale-access strategies.

Ready to Build Your Tax-Free Retirement Income Strategy?

Creating tax-free retirement income requires more than good intentions—it requires structured planning, carrier access, and expertise in Index Strategies that most retail advisors don't offer. At Everence Wealth, we guide families through comprehensive Financial Needs Assessments that stress-test your current strategy against taxes, volatility, and hidden fees. We'll show you exactly how much Tax-Deferred exposure you're carrying, quantify your future RMD liability, and design a Tax-Exempt bucket strategy using Index Strategies optimized for your income, timeline, and risk tolerance. Our independent broker model gives you access to seventy-five-plus carriers, ensuring you receive the most competitive floor rates, cap rates, and loan provisions available nationwide—not just what one company offers. If you're serious about reducing lifetime taxes, eliminating Required Minimum Distributions, and protecting retirement wealth from market downturns, schedule your Financial Needs Assessment today. We serve families across all fifty states and provide transparent, math-based analysis with zero pressure and zero conflicts of interest. Your retirement deserves a strategy as sophisticated as your career—let's build it together.

Schedule Your Financial Needs AssessmentThis content is for educational purposes only and does not constitute financial, tax, or legal advice. Index Strategy performance depends on policy structure, carrier crediting methods, and individual circumstances. Consult a licensed insurance professional and tax advisor before making any financial decisions. Policy loans reduce death benefit and cash value if not repaid.