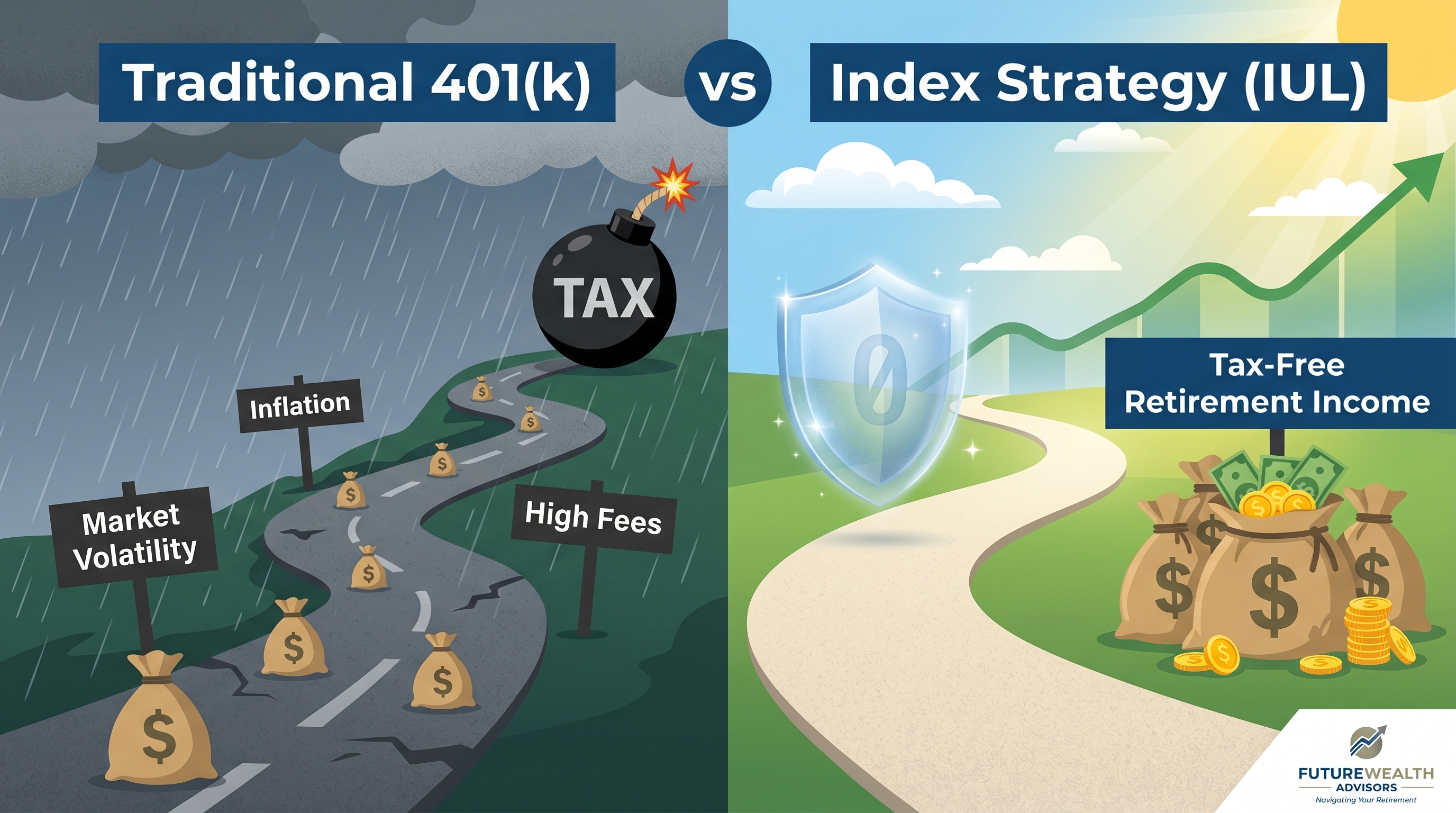

Tax-free retirement income through Index Strategies allows you to access funds without triggering federal income tax, RMDs, or IRMAA surcharges. Unlike 401(k)s and traditional IRAs that defer taxes until withdrawal, Index Strategies at Everence Wealth use tax-exempt policy loans to provide cash flow while tracking S&P 500 performance with zero-loss floor protection—what we call Zero is Your Hero.

Most Americans unknowingly build their retirement inside a tax time bomb. They contribute to 401(k)s and traditional IRAs for decades, believing they're securing their future—only to discover that every dollar withdrawn in retirement is fully taxable as ordinary income. When required minimum distributions (RMDs) force mandatory withdrawals starting at age seventy-three, many retirees find themselves pushed into higher tax brackets, triggering IRMAA Medicare surcharges and potentially losing deductions they counted on. The math is sobering: a $1 million IRA may deliver only $700,000 to $750,000 in actual purchasing power after federal and state taxes consume their share over two decades of retirement.

This tax exposure compounds during market volatility. If your IRA loses thirty percent in a downturn, you still owe taxes on future withdrawals—but now from a smaller principal base. You need a forty-three percent gain just to break even, and every dollar of that recovery is still taxable. This dual erosion—volatility drag combined with deferred tax liability—creates what we call the Retirement Gap: the distance between what you think you have and what you can actually spend. For families in high-tax states like California, New York, or New Jersey, combined federal and state marginal rates can exceed forty-five percent, meaning nearly half of every IRA withdrawal funds government obligations rather than your lifestyle.

Index Strategies offer a fundamentally different approach. By building tax-exempt accumulation through permanent life insurance structures, you create a retirement income stream that bypasses federal income tax, avoids RMDs entirely, and protects principal during market downturns through a guaranteed zero-loss floor. You participate in S&P 500 index growth up to a cap rate—typically eight to twelve percent annually depending on carrier and contract design—while locking in gains each year through an annual reset mechanism. When you need income, you access your cash value through tax-free policy loans rather than taxable distributions. This is how we help families shift from tax-deferred uncertainty to tax-exempt clarity, building sustainable retirement cash flow that compounds free from the Three Silent Killers: fees, volatility, and taxes.

Why Traditional Retirement Accounts Create Hidden Tax Liabilities

The appeal of 401(k)s and traditional IRAs rests on a single promise: defer taxes today, pay them later when you're in a lower bracket. But this assumption collapses under scrutiny. First, tax rates are historically low and likely to rise as federal debt expands and entitlement obligations grow. The Tax Cuts and Jobs Act provisions expire after the current legislative window, potentially returning top marginal rates to thirty-nine point six percent or higher. Second, successful savers often find themselves in the same or higher tax brackets during retirement, especially when RMDs force large mandatory withdrawals that stack atop Social Security income, pensions, and investment dividends. Third, the tax calculation is applied to the entire distribution amount, not just your original contributions—meaning you pay taxes on decades of compound growth you could have shielded entirely.

Required minimum distributions transform tax deferral into tax inevitability. Beginning at age seventy-three under current IRS rules, you must withdraw a percentage of your IRA or 401(k) balance annually, whether you need the cash or not. These forced distributions often push retirees into higher brackets, trigger IRMAA Medicare premium surcharges—which can add five hundred to six hundred dollars per month for high earners—and reduce eligibility for deductions and credits. For a married couple with $2 million in tax-deferred accounts, RMDs can exceed $80,000 annually by age seventy-five, creating a tax bill of $20,000 to $35,000 depending on state residency and other income sources. Over a twenty-five-year retirement, that's $500,000 to $875,000 in cumulative tax payments, none of which builds legacy or funds your actual lifestyle.

State income taxes amplify the damage. California's top marginal rate reaches thirteen point three percent. New York's combined state and city rates can exceed twelve percent. Add federal taxes, and a retiree in Los Angeles or Manhattan can lose nearly half of every IRA distribution to tax authorities. Even states without income tax, like Florida or Texas, expose retirees to full federal liability. The math is unavoidable: tax-deferred accounts defer the tax, but they don't eliminate it—and in many cases, they increase lifetime tax payments by allowing government claims to compound alongside your balance. This is why we emphasize the Three Tax Buckets Framework: diversifying across taxable, tax-deferred, and tax-exempt accounts so you control the tax timing and minimize government participation in your retirement income.

How Index Strategies Build Tax-Exempt Retirement Income

Index Strategies—structured as Indexed Universal Life (IUL) insurance contracts—are permanent life insurance policies with cash value growth linked to an external index, typically the S&P 500. Unlike traditional whole life insurance with fixed dividends or variable life insurance with direct market exposure, Index Strategies use a crediting mechanism that tracks index performance up to a specified cap rate while guaranteeing you never lose principal when the market drops. This floor-and-cap structure creates asymmetric returns: you participate in market gains, you're protected from market losses. Your worst year is zero percent, not negative. This is the foundation of Zero is Your Hero.

Here's how the mechanics work. Each policy anniversary, the carrier measures the S&P 500 index performance over the previous twelve months. If the index gained ten percent and your contract cap is eleven percent, you receive the full ten percent credit applied to your cash value. If the index gained fifteen percent, you receive the capped eleven percent credit. If the index dropped twenty percent, you receive zero percent credit—but you lose nothing. Your previous gains remain locked in through the annual reset, and your new floor begins at your protected principal balance. This means you compound from a stable base, never needing to recover from losses before resuming growth. Compare that to a traditional 401(k) investor who lost thirty percent in the 2008 financial crisis and needed over four years to break even, with every dollar of that recovery still fully taxable.

The tax advantage emerges through policy loans. IRS code Section 7702 governs life insurance taxation and allows policyholders to borrow against their accumulated cash value without triggering a taxable event, provided the contract remains in force. These loans are not considered distributions or withdrawals—they're advances against the death benefit, secured by the policy's cash value. As long as the policy does not lapse, you never repay the loans, and your beneficiaries receive a death benefit reduced by the outstanding loan balance but still entirely income-tax-free under Section 101(a). This structure allows you to generate retirement income that bypasses federal and state income taxes, escapes RMD requirements, and avoids IRMAA Medicare surcharge calculations entirely. You control the timing, the amount, and the tax treatment—what we call cash flow liberation.

S&P 500 vs Index Strategy: Protected Participation

The S&P 500 has historically delivered strong long-term returns—averaging approximately ten percent annually over the past fifty years—but with full exposure to market losses. Index Strategies track S&P 500 performance up to a cap rate, while a guaranteed floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss. If the S&P 500 drops thirty percent, a traditional investor loses thirty percent and needs a forty-three percent gain just to break even. An Index Strategy investor loses zero percent and captures the next market recovery from their full principal—compounding from a protected base. This is what we call Zero is Your Hero. Over a thirty-five-year accumulation period, avoiding just two major downturns—such as the 2000-2002 dot-com collapse and the 2008 financial crisis—can preserve hundreds of thousands of dollars in capital that would otherwise require years to recover, all while deferring or eliminating taxes on that growth.

The Three Tax Buckets Framework: Diversification Beyond Asset Allocation

Most financial planning focuses on asset allocation: stocks, bonds, real estate, commodities. But tax diversification is equally critical and often overlooked. The Three Tax Buckets Framework organizes your wealth by tax treatment, not asset class, allowing you to optimize withdrawals and minimize lifetime tax liability. The three buckets are Taxable, Tax-Deferred, and Tax-Exempt. Each serves a different purpose, and strategic retirement planning requires intentional balance across all three, not overconcentration in just one.

The Taxable Bucket includes checking accounts, savings, brokerage accounts, rental properties, and any asset that generates reportable income each year. Interest, dividends, capital gains, and rental income are taxed annually, reducing your net compounding rate. The advantage is liquidity and flexibility: you can access these funds anytime without penalties. The disadvantage is tax drag—your effective growth rate is reduced every year by your marginal tax rate, sometimes shaving two to four percentage points off your nominal returns over decades. For emergency funds and short-term cash needs, the Taxable Bucket is essential. But it's the least efficient vehicle for long-term compounding.

The Tax-Deferred Bucket includes 401(k)s, traditional IRAs, 403(b)s, SEP IRAs, and similar qualified retirement accounts. Contributions reduce your taxable income today, and growth compounds without annual tax, but every dollar withdrawn in retirement is taxed as ordinary income. This bucket is powerful for high earners during peak earning years who can defer six-figure contributions and reduce current-year tax bills. The danger is concentration: most Americans have eighty to ninety percent of their retirement savings in this bucket, creating massive future tax liability and zero flexibility to manage tax brackets during retirement. RMDs force withdrawals on the IRS timeline, not yours, often at the worst possible tax moment.

The Tax-Exempt Bucket includes Roth IRAs, Roth 401(k)s, Health Savings Accounts (HSAs) used strategically, and Index Strategies. Contributions are made with after-tax dollars, but all growth and distributions are entirely tax-free if structured correctly. Roth accounts have contribution limits—$7,000 annually for IRAs in recent years, plus catch-up contributions—and income phaseouts that exclude high earners. Index Strategies have no contribution limits and no income restrictions, making them the only scalable tax-exempt vehicle for affluent families. A business owner earning $500,000 annually can fund $100,000 or more into an Index Strategy, building seven-figure tax-free cash value over twenty to thirty years—something impossible through Roth accounts alone. This is the wholesale advantage independent brokers provide: access to institutional-grade strategies without retail limitations.

How Policy Loans Deliver Tax-Free Income Without RMDs or IRMAA Exposure

The single greatest advantage of Index Strategies for retirement income is the policy loan mechanism. Unlike Roth IRA distributions, which are tax-free but still counted as income for IRMAA calculations, policy loans are not reported as income to the IRS. They don't appear on your 1040. They don't increase your adjusted gross income. They don't trigger RMDs, affect Social Security taxation, or push you into higher Medicare premium brackets. For high-net-worth retirees, this invisibility is worth tens of thousands of dollars annually in avoided surcharges and preserved deductions.

Here's how it works in practice. Suppose you've accumulated $800,000 in cash value inside an Index Strategy over twenty-five years. You retire at age sixty-five and need $60,000 annually to supplement Social Security and pension income. Instead of withdrawing $60,000 from your IRA—which would be fully taxable and potentially trigger IRMAA—you take a $60,000 policy loan from your Index Strategy. The carrier advances you the cash and secures it against your policy's cash value. You owe no interest payments, though most carriers charge an internal loan rate of three to five percent, offset partially by a credited wash loan rate. The net cost is typically one to two percent annually, far less than the twenty to forty percent combined tax hit you'd face on an IRA distribution.

Because the loan is not income, your adjusted gross income remains low, preserving your eligibility for lower Medicare Part B and Part D premiums. In recent years, IRMAA thresholds for married couples began at modified adjusted gross income above $194,000, with surcharges escalating in five tiers up to $750 per person per month at the highest income levels. A couple pulling $100,000 from IRAs could easily trigger $12,000 to $18,000 in annual IRMAA surcharges. By using policy loans instead, you avoid this entirely, keeping Medicare costs at the standard base premium. Over a twenty-five-year retirement, this invisibility saves $300,000 or more in surcharges alone—money that stays in your estate rather than funding government programs.

Policy loans also provide flexibility. You decide how much to borrow and when. If markets drop and you want to reduce spending temporarily, you simply take a smaller loan or skip a year. There's no RMD forcing your hand. If you need a large lump sum for a home remodel, medical expense, or family gift, you can access it without tax consequences or penalties. And because the policy remains in force until death, any outstanding loan balance is simply deducted from the death benefit, which passes income-tax-free to your beneficiaries under Section 101(a). This means your heirs inherit the net death benefit without income tax, estate tax (up to current exemption limits), or probate delay—what we call the triple tax advantage of permanent life insurance.

Comparing Index Strategies to Roth IRAs and 401(k)s for Retirement Income

Clients frequently ask how Index Strategies compare to Roth IRAs, given that both offer tax-free income. The answer hinges on contribution limits, income restrictions, and flexibility. Roth IRAs cap contributions at $7,000 annually (with $1,000 catch-up for those fifty and older), and high earners face phaseout limits that begin at modified adjusted gross income of $153,000 for married couples in recent years. If you earn $250,000, you cannot contribute directly to a Roth IRA without using backdoor conversion strategies—which themselves carry tax costs and complexity. A couple maxing out Roth contributions at $16,000 annually for thirty years, assuming seven percent growth, accumulates approximately $1.5 million. That's meaningful, but insufficient for many affluent families.

Index Strategies have no contribution limits and no income phaseouts. A business owner can fund $50,000, $100,000, or more annually depending on policy design and underwriting limits, building multi-million-dollar cash values over the same time horizon. This scalability makes Index Strategies the primary tax-exempt vehicle for high earners who've maxed out Roth accounts and still need additional tax-free accumulation. Additionally, Roth distributions—while tax-free—are still counted as income for IRMAA calculations under current Medicare rules. Policy loans are not. For retirees managing IRMAA exposure, Index Strategies provide true income invisibility that Roth accounts cannot match.

Compared to 401(k)s, the contrast is even sharper. A 401(k) allows tax-deferred contributions up to $23,000 annually (with catch-up provisions), and employer matches can push total contributions higher. Growth compounds tax-deferred, but every dollar withdrawn is taxed as ordinary income. RMDs begin at seventy-three, forcing withdrawals whether needed or not. If the market crashes the year before you retire, your balance drops and you lose years recovering—with every dollar of that recovery still taxable. Index Strategies eliminate all four risks: no annual taxation, no RMDs, no sequence-of-returns risk due to the zero floor, and no income tax on distributions via policy loans. The tradeoff is that Index Strategies require permanent life insurance underwriting and carry internal costs—but for healthy individuals planning multi-decade retirements, the tax arbitrage and downside protection often deliver superior net after-tax income compared to fully taxable 401(k) withdrawals.

| Feature | Index Strategy | 401(k) | Roth IRA |

|---|---|---|---|

| Annual Contribution Limit | No statutory limit; determined by underwriting and policy design, often $50,000 to $150,000+ annually for affluent families depending on age, health, and income replacement needs. | $23,000 employee deferral (recent limit), plus employer match; total contributions capped at $69,000 including profit-sharing for high earners in recent years. | $7,000 annually ($8,000 age fifty-plus); phaseout begins at $153,000 MAGI for married couples, eliminating direct contributions for high earners. |

| Tax Treatment of Growth | Cash value grows tax-deferred; gains are never taxed if accessed via policy loans and policy remains in force until death. | Growth is tax-deferred; all distributions taxed as ordinary income at federal and state marginal rates during retirement. | Growth is tax-free; qualified distributions after age fifty-nine and a half and five-year holding period are entirely tax-free. |

| Required Minimum Distributions | None. No RMDs ever. You control timing and amount of policy loans for income without IRS-mandated withdrawal schedules. | RMDs begin at age seventy-three; IRS mandates annual withdrawals based on life expectancy tables, forcing taxable income whether needed or not. | No RMDs during owner's lifetime; beneficiaries face RMDs under SECURE Act rules, but original owner has full control. |

| Market Downside Protection | Zero-loss floor guarantees no principal loss in down markets; annual reset locks in gains; worst-case year is 0% credited interest, preserving capital. | Full market exposure; account value drops during bear markets; sequence-of-returns risk can devastate early retirees forced to sell in downturns. | Full market exposure within chosen investments; no principal protection; losses reduce compounding base and require recovery gains. |

| Income Tax on Distributions | Policy loans are not taxable income; do not appear on Form 1040; provide true tax-free cash flow without increasing AGI or triggering IRMAA. | All distributions taxed as ordinary income; every dollar withdrawn adds to taxable income, potentially pushing retirees into higher brackets and triggering IRMAA surcharges. | Qualified distributions are tax-free but counted as income for IRMAA purposes under current Medicare rules; can trigger premium surcharges despite zero tax. |

| Early Access Penalties | Policy loans available anytime without penalty or age restriction; no 10% early withdrawal penalty; liquidity from day one if policy is properly funded. | Withdrawals before age fifty-nine and a half incur 10% penalty plus ordinary income tax; exceptions exist but are limited and complex. | Contributions (not earnings) can be withdrawn anytime tax- and penalty-free; earnings withdrawn before fifty-nine and a half face 10% penalty plus tax unless exception applies. |

| Estate Planning & Death Benefit | Death benefit passes income-tax-free to beneficiaries under IRC Section 101(a); avoids probate; can provide immediate liquidity to heirs; outstanding loans reduce benefit but remainder is tax-free. | Beneficiaries pay ordinary income tax on inherited balance; must withdraw within ten years under SECURE Act for most non-spouse heirs; no step-up in basis. | Beneficiaries receive tax-free but must withdraw within ten years for most non-spouse heirs; no income tax but distributions required under SECURE Act. |

Structuring an Index Strategy for Maximum Tax-Free Retirement Income

Designing an Index Strategy for retirement income requires precision. The goal is to maximize cash value accumulation while maintaining permanent life insurance status under IRS Section 7702 guidelines, which impose a corridor test and guideline premium test to prevent policies from becoming modified endowment contracts (MECs). A MEC loses the tax-free loan advantage—distributions become taxable and subject to penalties if taken before fifty-nine and a half. Properly structured policies avoid MEC status by funding below the guideline premium limit while maximizing contributions over the first ten to fifteen years, front-loading cash value growth during the early compounding phase.

We typically design policies with minimum death benefit relative to premium to maximize cash accumulation, using either a level death benefit option or an increasing benefit that adjusts with cash value. Younger clients—ages thirty-five to fifty—can fund aggressively for twenty to twenty-five years, allowing cash value to compound for decades before retirement income begins. Older clients—ages fifty to sixty—use a shorter funding period, often ten to fifteen years, with higher annual premiums to build sufficient cash value by retirement age. Riders such as paid-up additions or indexed account allocations are selected based on client risk tolerance, income timeline, and carrier-specific crediting options.

Carrier selection is critical. Not all Index Strategies are created equal. We partner with seventy-five-plus carriers, allowing us to compare cap rates, participation rates, crediting methods, loan provisions, and financial strength ratings. Some carriers offer uncapped accounts with participation rates; others provide higher fixed caps with simpler crediting. Some allow zero-cost loans with offset provisions; others charge net loan costs of one to two percent. We stress-test each contract using historical S&P 500 data, modeling performance across multiple decades including the 2000-2002 and 2008-2009 downturns, ensuring the policy can sustain planned loan amounts without lapse risk. This is the independent broker advantage: we're not captive to one company's product—we build your strategy across the best available options in the marketplace.

About Steven Rosenberg & Everence Wealth

Steven Rosenberg is the Founder and Chief Wealth Strategist at Everence Wealth, an independent insurance brokerage headquartered in San Francisco, California. As an independent broker, Steven is not employed by any insurance company, bank, or Wall Street institution—he works exclusively in the client's best interest, with access to seventy-five-plus carrier partnerships across all fifty states. His expertise centers on Index Strategies, tax-exempt retirement planning, and the S&P 500-linked growth models that provide principal protection through zero-floor mechanisms. Steven specializes in helping families, business owners, and professionals navigate the Three Tax Buckets Framework, minimize exposure to the Three Silent Killers—fees, volatility, and taxes—and build sustainable retirement cash flow that does not trigger RMDs or IRMAA surcharges. He is a licensed insurance professional with deep experience stress-testing portfolios across multiple economic cycles, including the dot-com collapse, the financial crisis, and recent market volatility. Steven's educational approach emphasizes math-based transparency, regulatory accuracy, and long-term strategies that prioritize Cash Flow over Net Worth. Every Index Strategy designed at Everence Wealth is built using real carrier illustrations, historical S&P 500 performance data, and rigorous scenario planning to ensure policies remain in force and deliver planned income throughout retirement. Everence Wealth does not offer securities, investment advisory services, or fiduciary investment management—our focus is exclusively on insurance-based wealth strategies, asset protection, and tax-efficient retirement income planning through independent broker access to wholesale markets.

Schedule Your Financial Needs Assessment Today

If you're concerned about future tax rates, RMD exposure, or sequence-of-returns risk in your retirement plan, it's time to stress-test your strategy. At Everence Wealth, we provide a comprehensive Financial Needs Assessment that evaluates your Three Tax Buckets, quantifies your exposure to the Three Silent Killers, and models Index Strategy solutions tailored to your income timeline, risk tolerance, and legacy goals. We'll compare your current plan against tax-free alternatives, run historical performance scenarios, and show you exactly how Zero is Your Hero can protect your principal while capturing S&P 500 upside. Whether you're a business owner maxing out 401(k) contributions, a high-earner phased out of Roth IRAs, or a retiree managing IRMAA surcharges, we'll build a roadmap to tax-exempt retirement income that puts you in control. Schedule your Financial Needs Assessment today and discover how independent broker access to seventy-five-plus carriers can transform your retirement outcome.

Schedule Your Financial Needs AssessmentThis content is for educational purposes only and does not constitute financial, tax, or legal advice. Index Strategies involve permanent life insurance contracts with fees, costs, and underwriting requirements. Policy performance depends on carrier financial strength, crediting rates, and proper policy management. Consult a licensed insurance professional and tax advisor before making any financial decisions.