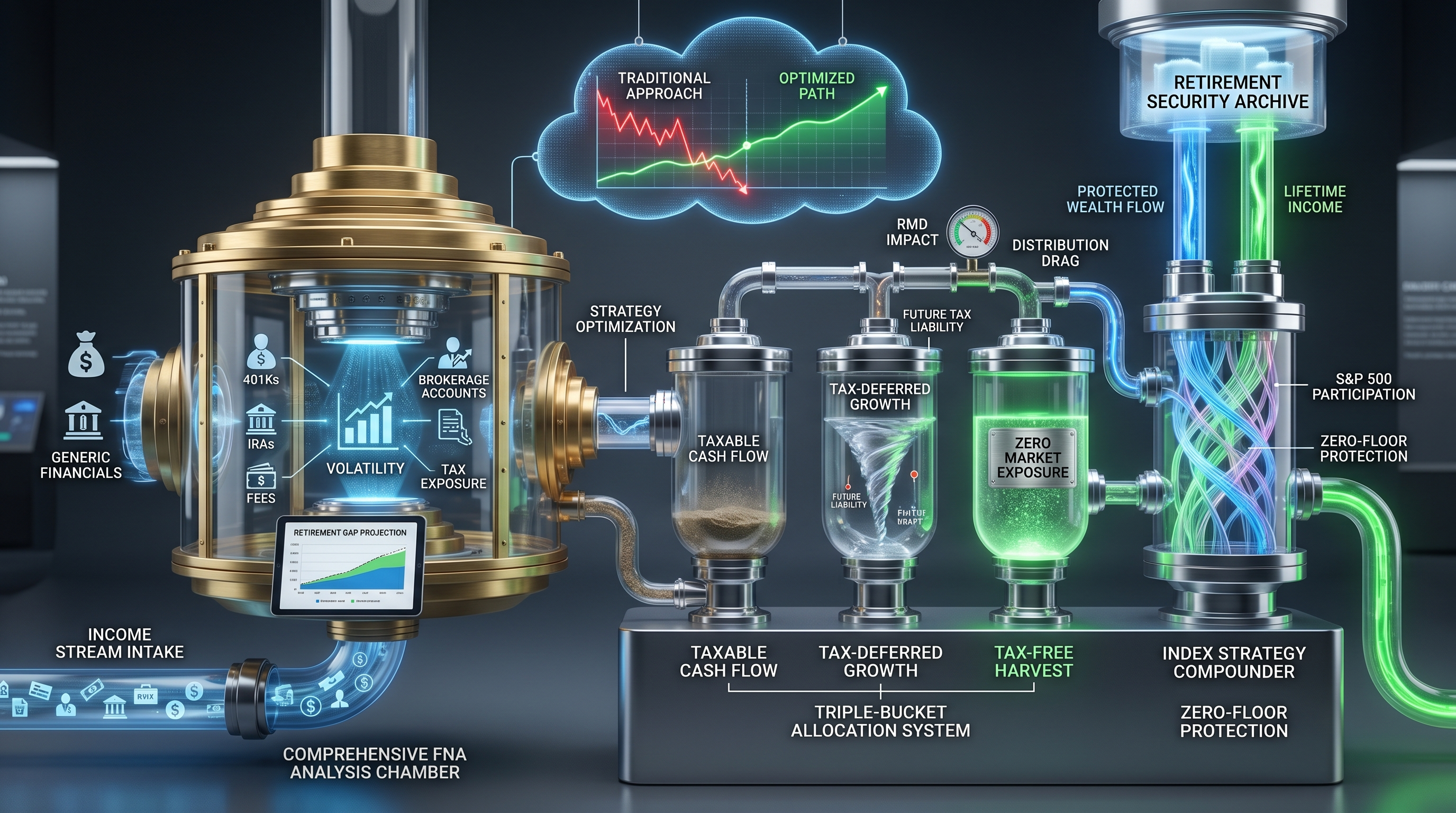

A Financial Needs Assessment (FNA) is a comprehensive evaluation of your complete financial picture, analyzing income sources, tax exposure, retirement gaps, and protection strategies. At Everence Wealth, we use the FNA process to identify hidden risks in traditional retirement plans and demonstrate how Index Strategies with S&P 500 participation and zero-floor protection can bridge your retirement gap while minimizing tax liability across all three tax buckets.

Most Americans believe they have a retirement plan when they actually have a collection of financial products with no coordinated strategy. A 401k here, an old IRA there, some life insurance from a decade ago, and maybe a taxable brokerage account. But without a comprehensive Financial Needs Assessment, these disconnected pieces often work against each other, exposing families to unnecessary tax liability, market volatility, and catastrophic income gaps in retirement. We've seen portfolios that look substantial on paper crumble under the weight of required minimum distributions, market downturns, and compounding fee drag over thirty-five years.

A properly executed Financial Needs Assessment doesn't just inventory your accounts. It stress-tests your entire financial strategy against the Three Silent Killers: fees, volatility, and taxes. It calculates your actual retirement gap—the difference between what you'll have and what you'll need to maintain your lifestyle without market exposure or tax surprises. Most importantly, it reveals whether your current approach positions you in the right tax buckets to maximize cash flow when you need it most. The results often surprise people who assumed their employer-sponsored plan would be enough.

At Everence Wealth, we approach the Financial Needs Assessment from the perspective of an independent broker with access to seventy-five carrier partnerships across all fifty states. We don't work for any insurance company, bank, or Wall Street institution. Our analysis focuses on building tax-efficient retirement income through Index Strategies that track S&P 500 performance with a guaranteed zero-loss floor, ensuring you participate in market growth while protecting your principal from downturns. This article breaks down exactly what a Financial Needs Assessment entails, why it's critical for retirement planning, and how it reveals opportunities traditional advisors often miss.

What Does a Comprehensive Financial Needs Assessment Actually Include?

A true Financial Needs Assessment goes far beyond reviewing your current account balances. It begins with a detailed analysis of your Human Life Value—the total economic worth of your future earning potential. Most families dramatically underinsure this asset, leaving spouses and dependents vulnerable if something happens to the primary income earner. We calculate the present value of your remaining work years, factor in inflation and income growth, and determine the protection gap between your current life insurance coverage and what your family would actually need to maintain their standard of living without you.

The assessment then maps your entire asset base across the Three Tax Buckets: taxable accounts subject to capital gains and ordinary income tax, tax-deferred accounts like 401ks and traditional IRAs that will trigger required minimum distributions and ordinary income tax in retirement, and tax-exempt accounts including Roth IRAs and properly structured Index Strategies that generate income without 1099 reporting. Most people concentrate too heavily in the tax-deferred bucket because of employer matching and immediate deductions, not realizing they're building a tax time bomb that will detonate when they can least afford it—during retirement when they need maximum flexibility and minimum government interference.

We also stress-test your portfolio against market volatility using actual S&P 500 historical data. If the market drops thirty percent like it did in 2008, how long until you recover? Remember, a thirty percent loss requires a forty-three percent gain just to break even—and you're earning zero returns on money you no longer have during the recovery period. We compare this to Index Strategy positioning where your worst year is zero percent, allowing you to compound from your full principal base when markets recover. This is what we mean by Zero is Your Hero—the mathematical advantage of never participating in market losses while still capturing S&P 500 linked growth up to annual cap rates.

Finally, the assessment projects your actual retirement income need, not the generic seventy to eighty percent of pre-retirement income that traditional planners cite. We analyze your current lifestyle expenses, add healthcare inflation, factor in travel and leisure goals, and calculate the monthly cash flow required to live comfortably without worrying about market conditions or tax bracket surprises. Then we compare that to what your current strategy will actually deliver after fees, taxes, and required minimum distributions. The gap is often shocking, particularly for high-income professionals who assumed their 401k would be sufficient simply because the balance looks impressive today.

Why Traditional Retirement Planning Often Fails the Stress Test

The traditional retirement model promoted by Wall Street and most employer-sponsored plans operates on deeply flawed assumptions. It assumes consistent market returns despite well-documented volatility cycles. It assumes tax rates will remain stable or decrease despite mounting federal debt and demographic pressures on Social Security and Medicare. It assumes your health will remain good and long-term care needs won't materialize. And critically, it assumes the financial products you purchased years ago still serve your current needs despite dramatic life changes like marriage, children, home purchases, business ownership, or aging parents requiring support.

Most 401k plans expose participants to the full downside of market volatility while charging annual fees that compound negatively over decades. A seemingly modest one percent annual management fee can reduce your portfolio value by twenty-eight percent over thirty-five years compared to a zero-fee alternative, according to Department of Labor calculations using the Rule of 72. Divide seventy-two by your return rate to estimate doubling time—but also recognize that fees work the same way in reverse, cutting your wealth accumulation roughly in half over a typical career if you're paying one to two percent annually in combination fees, expense ratios, and transaction costs embedded in mutual funds.

Tax-deferred growth sounds appealing until you realize you're simply postponing taxation to a period when you have zero control over future rates. Required minimum distributions force you to withdraw and pay taxes on money you might not need, potentially pushing you into higher brackets and triggering taxation on Social Security benefits. Medicare premium surcharges kick in at certain income thresholds, meaning your RMD can cost you thousands in additional healthcare expenses beyond the direct tax hit. This is why we emphasize positioning assets across all three tax buckets—you need flexibility to pull income from the most tax-efficient source each year based on your specific situation.

A proper Financial Needs Assessment exposes these structural weaknesses before they become catastrophic. We've worked with families in their late fifties who discovered their 401k and IRA balances, while substantial, would generate fifty to sixty percent of their required income after accounting for taxes, required distributions, and conservative withdrawal rates designed to prevent running out of money. The remaining forty percent gap requires a completely different strategy—one focused on tax-exempt cash flow, protection from market losses, and access to living benefits if health issues emerge before retirement age.

S&P 500 vs Index Strategy: Understanding Protected Participation

S&P 500 vs Index Strategy: Protected Participation

The S&P 500 has historically delivered strong long-term returns—but with full exposure to market losses during downturns. Index Strategies track S&P 500 performance up to a cap rate, typically ranging from ten to fourteen percent annually depending on carrier and current interest rate environments, while a guaranteed floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss. This isn't about outperforming the market—it's about protecting your retirement from the devastating mathematics of volatility.

If the S&P 500 drops thirty percent, a traditional investor loses thirty percent of their account value and needs a forty-three percent gain just to break even. During the recovery period, they're compounding returns on a reduced principal base. An Index Strategy investor loses zero percent and captures the next market recovery from their full principal—compounding from a protected base without the recovery drag. Over multiple market cycles, this protection significantly reduces sequence-of-returns risk, which is the danger that market losses early in retirement permanently impair your ability to generate income for thirty-plus years.

The annual reset mechanism locks in your gains each year, creating a new protected floor. If you earn twelve percent in year one, that gain becomes part of your protected principal going into year two. A market crash in year two doesn't erase your previous year's growth—it simply results in a zero percent year while traditional portfolios crater. This is what we call Zero is Your Hero. Your worst year is zero, not negative twenty or negative thirty. The mathematics of compounding from a stable, protected base versus a volatile, frequently negative base make an enormous difference over the thirty to forty years most people spend in retirement.

How Index Strategies Position Across the Three Tax Buckets

One of the most powerful advantages revealed during a Financial Needs Assessment is how properly structured Index Strategies provide tax-exempt retirement income without the contribution limits and restrictions of Roth IRAs. When you access the cash value of an Index Strategy through policy loans rather than withdrawals, those loans are not considered taxable income by the IRS. You receive cash flow to live on, no 1099 form arrives, and the money doesn't count toward Medicare premium surcharge thresholds or cause taxation of Social Security benefits. This is fundamentally different from pulling money from a 401k or traditional IRA, which triggers ordinary income tax at your highest marginal rate.

This tax treatment becomes extraordinarily valuable for high-income professionals, business owners, and anyone who maxes out Roth IRA contributions but still faces a significant retirement gap. While Roth contributions are limited to seven thousand dollars annually for individuals under fifty and eight thousand for those over fifty, Index Strategies have no such restrictions. You can fund them with amounts appropriate to your actual retirement need rather than arbitrary government limits designed for average earners. For someone needing to generate an additional fifty to seventy-five thousand dollars annually in tax-free retirement income, this flexibility is essential.

The Financial Needs Assessment maps your current tax bucket allocation and projects what it will look like at retirement. Many people discover ninety percent or more of their retirement assets sit in tax-deferred accounts, meaning virtually every dollar they withdraw will be taxed as ordinary income. By repositioning a portion of assets into tax-exempt Index Strategies over time, you create optionality. In low-income years, you might pull from taxable accounts and pay capital gains rates. In higher-income years, you access tax-exempt Index Strategy cash value. In years when Roth conversions make sense, you have tax-free income from Index Strategies to live on while converting traditional IRA money and paying the tax bill from other sources. This flexibility is worth tens of thousands of dollars annually for many retirees.

Additionally, Index Strategies include a death benefit that passes income-tax-free to beneficiaries, creating a powerful estate planning tool that traditional retirement accounts simply cannot match. Your heirs inherit a traditional IRA and must pay ordinary income tax on every dollar distributed under the ten-year rule imposed by the SECURE Act. They inherit an Index Strategy death benefit and receive the money income-tax-free, often using it to pay estate taxes or fund trusts without additional tax liability. This consideration becomes particularly important for families with estates approaching or exceeding federal and state exemption thresholds.

Calculating Your Actual Retirement Gap with Mathematical Precision

The retirement gap is the difference between what you'll have and what you'll need, but most people dramatically miscalculate both sides of that equation. On the income side, they overestimate portfolio performance by assuming historical average returns without accounting for sequence-of-returns risk—the reality that actual year-by-year volatility produces significantly worse outcomes than smooth average returns. They underestimate fee drag, often unaware of the cumulative expense ratios, 12b-1 fees, transaction costs, and advisor fees embedded in their accounts. And they completely ignore tax liability, mentally spending their gross 401k balance rather than the net after-tax amount they'll actually receive.

On the expense side, people consistently underestimate retirement spending, particularly in the early active years when travel, hobbies, and healthcare costs peak before gradually declining. Healthcare inflation runs substantially higher than general inflation, and most people will face significant out-of-pocket costs despite Medicare coverage. Long-term care expenses represent a catastrophic risk that can consume hundreds of thousands of dollars, yet most families have no dedicated strategy beyond hoping it doesn't happen to them. A comprehensive Financial Needs Assessment quantifies all these factors with actuarial precision rather than hopeful assumptions.

We use Monte Carlo simulation to stress-test your portfolio against thousands of potential market scenarios, calculating the probability you'll run out of money at different withdrawal rates. A four percent withdrawal rate—the traditional rule of thumb—often produces failure rates of twenty to thirty percent when you factor in realistic volatility, extended life expectancy, and the current low-yield environment. This is why Index Strategies with protected floors and annual reset mechanisms provide such value. They remove the left tail risk of catastrophic market losses early in retirement, significantly improving the probability your money lasts through your entire life expectancy and potentially leaves a legacy for heirs.

The assessment also calculates the breakeven age for various strategies. At what age does delaying Social Security maximize lifetime benefits? When does a Roth conversion create more after-tax wealth than leaving money in a traditional IRA despite paying conversion taxes now? At what point does repositioning money from volatile market exposure into protected Index Strategies reduce lifetime sequence-of-returns risk more than it costs in foregone upside above the cap rate? These calculations are mathematically complex but critically important, and they're unique to your specific situation, risk tolerance, and life expectancy assumptions.

Living Benefits and Protection Strategies Most Financial Plans Ignore

A complete Financial Needs Assessment addresses not just retirement income but protection against life events that can derail even the best wealth accumulation strategy. Index Strategies include living benefit riders that allow you to access a portion of the death benefit while you're still alive if diagnosed with a chronic, critical, or terminal illness. This means the same dollar provides both lifetime tax-free retirement income through policy loans and catastrophic health event protection through living benefits—dual purposes that traditional retirement accounts cannot serve.

Consider the financial devastation a cancer diagnosis or stroke creates for most families. Medical treatment costs pile up despite insurance. One spouse may need to stop working to provide care, cutting household income precisely when expenses spike. Traditional retirement accounts can be accessed early, but you'll pay a ten percent penalty plus ordinary income tax, potentially surrendering forty to fifty percent of every dollar withdrawn to penalties and taxes when you're most financially vulnerable. Index Strategy living benefits provide access to cash with no penalties, no taxation, and no permanent impairment of your retirement strategy if you recover and return to work.

The Human Life Value calculation component of the Financial Needs Assessment reveals protection gaps that could bankrupt surviving spouses and dependents. Most people carry enough life insurance to pay off the mortgage and cover a few years of expenses, but nowhere near enough to replace the lifetime income earning potential of the deceased spouse. A forty-year-old professional earning one hundred fifty thousand annually has a present value of approximately three to four million dollars in future earnings potential. If they're insured for five hundred thousand dollars, their family faces a multi-million-dollar wealth destruction event if they die prematurely. Index Strategies can fill this gap while simultaneously serving as a tax-exempt retirement vehicle, making them dramatically more capital-efficient than buying term insurance and investing the difference in taxable accounts.

Disability insurance through employer plans typically replaces sixty percent of income and is taxable if the employer paid the premiums, netting perhaps forty to fifty percent of pre-disability income after taxes. This is often insufficient to maintain mortgage payments, fund children's education, and continue retirement savings. The cash value accumulation in Index Strategies provides an additional liquidity source during disability periods, supplementing limited disability benefits without triggering additional taxation. This layer of protection rarely appears in traditional financial plans because traditional advisors don't have access to these integrated life insurance and retirement income strategies.

Why Independent Broker Access to 75+ Carriers Matters for Your Strategy

As an independent broker rather than a captive agent or registered investment advisor limited to proprietary products, we access policy designs and carriers that provide superior value for clients across different ages, health classifications, and financial objectives. Not all Index Strategy carriers are equal. Some offer higher cap rates but weaker financial strength ratings. Others provide better living benefit riders but lower cash value accumulation. Some excel with younger, healthy clients while others specialize in simplified underwriting for older individuals or those with health conditions. Having access to seventy-five carriers means we can design your strategy using the optimal carrier for your specific situation rather than forcing you into whatever products we're contracted to sell.

This independent structure also eliminates conflicts of interest inherent in traditional financial planning models. We don't manage assets for a percentage fee, creating incentive to keep your money under management whether or not that serves your needs. We don't receive ongoing trailing commissions from mutual fund companies, creating incentive to recommend expensive products with hidden 12b-1 fees. We don't work for a bank trying to cross-sell mortgages, credit cards, and brokerage accounts. Our compensation comes from helping you implement properly structured protection and Index Strategy solutions, after which we have zero financial incentive to churn your account or recommend unnecessary changes.

The Financial Needs Assessment process reveals whether you're paying retail prices for wholesale financial products. Wall Street sells retail—high fees, limited transparency, conflicts of interest embedded throughout the distribution chain. Independent brokers with carrier partnerships access wholesale pricing and institutional-quality products typically reserved for high-net-worth families working with private wealth managers. For many clients, the fee savings alone over a thirty-year retirement exceed six figures compared to traditional managed accounts charging one to two percent annually on increasingly large balances as your wealth compounds.

We're also not geographically limited. Licensed across all fifty states, we work with families in high-tax states like California, New York, and New Jersey where state income tax makes tax-deferred retirement accounts particularly punitive, as well as families in no-income-tax states like Texas, Florida, and Nevada where the strategy considerations differ. The Financial Needs Assessment accounts for your specific state tax environment, property tax burden, and estate tax exposure if you live in one of the states with exemptions lower than the federal threshold. These state-level considerations often make the difference between a good retirement and a great one.

What Happens After Your Financial Needs Assessment

The Financial Needs Assessment generates a detailed written analysis showing your current trajectory, identifying specific gaps and vulnerabilities, and proposing an alternative strategy using Index Strategies, tax bucket repositioning, and protection solutions. You'll see side-by-side projections comparing your current path to an optimized approach, with all assumptions clearly stated and conservative rather than aggressive. We show you the math on fee drag, tax liability, volatility impact, and death benefit leverage so you can make fully informed decisions based on your specific values and risk tolerance.

Implementation happens in stages based on your liquidity, insurability, and timeline. For younger families still in wealth accumulation phase, we typically emphasize maximizing Human Life Value protection while beginning tax-exempt cash value accumulation through Index Strategies funded at levels appropriate to your budget and retirement gap calculations. For families approaching retirement, we may recommend partial Roth conversions during low-income years, repositioning of tax-deferred money into tax-exempt Index Strategies, and strategic timing of Social Security to maximize lifetime benefits. For retirees already drawing income, we focus on tax-efficient distribution strategies and healthcare cost management.

Every strategy is customized because every family's situation is unique. Cookie-cutter financial planning fails because it ignores the specific variables that matter most to you—your state tax environment, your health status and insurability, your risk tolerance after living through market crashes, your legacy intentions for heirs, and your willingness to accept cap rate limitations in exchange for downside protection. The Financial Needs Assessment provides the data foundation for these decisions, but the strategy reflects your values and objectives rather than a one-size-fits-all model.

We also provide ongoing support as your situation evolves. Marriage, divorce, children, home purchases, business sales, inheritance, job changes, and health events all require strategy adjustments. Most traditional financial advisors provide an initial plan and then essentially leave you alone except for annual reviews focused on investment performance. We maintain relationships focused on life transitions and tax law changes that create planning opportunities. When the SECURE Act changed inherited IRA rules, we proactively contacted clients to discuss how Index Strategy death benefits could replace the stretch IRA strategy for legacy planning. This kind of ongoing strategic support reflects the difference between a product sale and a true advisory relationship.

About Steven Rosenberg and Everence Wealth

Steven Rosenberg is the Founder and Chief Wealth Strategist at Everence Wealth, a San Francisco-based independent financial firm specializing in tax-efficient retirement planning through Index Strategies. As an independent broker with seventy-five carrier partnerships, Steven works exclusively in the client's best interest without conflicts of interest from proprietary products, asset management fees, or institutional sales quotas. Licensed across all fifty states, he serves families, business owners, and professionals seeking alternatives to traditional Wall Street retirement planning, with particular expertise in high-tax-state strategies, business succession planning, and tax bucket optimization. Steven developed the comprehensive Financial Needs Assessment framework to expose the Three Silent Killers—fees, volatility, and taxes—that traditional financial plans ignore, and to demonstrate how S&P 500-linked Index Strategies with zero-floor protection can bridge retirement gaps while providing living benefits and tax-exempt income unavailable through 401ks and IRAs. His educational approach emphasizes mathematical transparency, historical market data, and current tax law rather than projections or promises, helping clients make fully informed decisions about protection and wealth transfer strategies that serve multiple generations. As an independent broker rather than a captive agent or fee-based advisor, Steven's compensation structure aligns with implementing solutions rather than managing assets indefinitely, eliminating the conflicts inherent in traditional financial planning models where advisors profit from keeping clients invested in volatile markets regardless of actual retirement security.

Schedule Your Comprehensive Financial Needs Assessment

Most families have never received a true Financial Needs Assessment that stress-tests their retirement strategy against fees, volatility, and taxes while calculating their actual Human Life Value protection gap. If you're concerned about market volatility in retirement, frustrated by high fees and confusing statements, worried about tax time bombs in your 401k, or simply unsure whether your current trajectory will actually deliver the retirement you envision, we can help. Our comprehensive assessment process reveals exactly where you stand, identifies specific vulnerabilities, and demonstrates how Index Strategies with S&P 500 participation and zero-floor protection can provide tax-exempt income, living benefits, and legacy advantages traditional retirement accounts cannot match. As an independent broker with access to seventy-five carriers across all fifty states, we design customized strategies using optimal carriers for your age, health, and objectives rather than limiting you to proprietary products. Schedule your Financial Needs Assessment today and discover what Wall Street doesn't want you to know about building tax-efficient, protected retirement income that lasts your entire lifetime.

Schedule Your Financial Needs AssessmentThis content is for educational purposes only and does not constitute financial, tax, or legal advice. Index Strategy performance depends on carrier financial strength, policy design, current cap and participation rates, and individual circumstances. Past performance of the S&P 500 or any index does not guarantee future results. Consult a licensed professional before making any financial decisions.