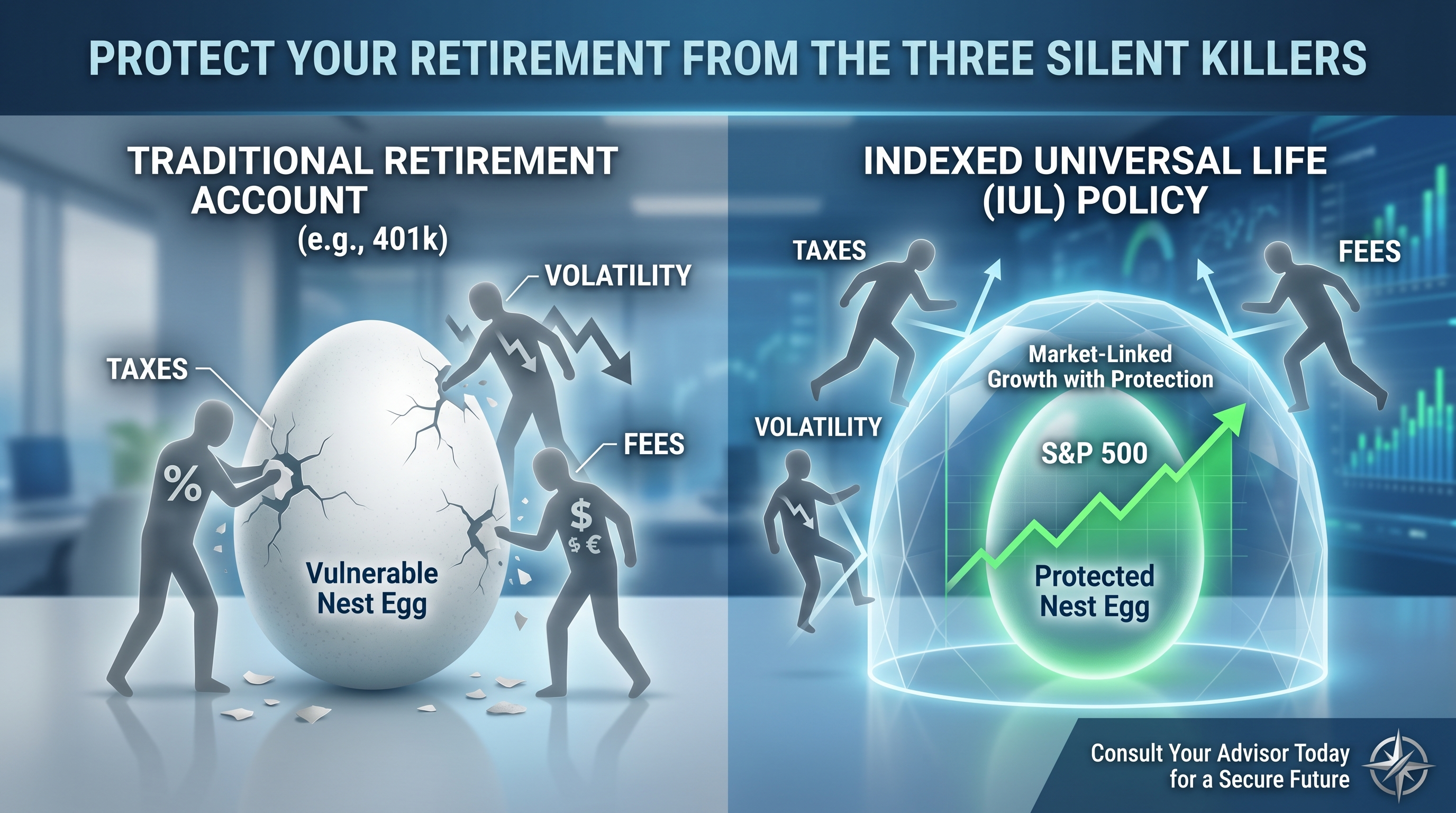

Indexed Universal Life Insurance (IUL) offers tax-free retirement income by linking cash value growth to market indexes like the S&P 500 with downside protection. Everence Wealth specializes in Index Strategies that capture market upside while protecting principal with a zero-loss floor—applying the S&P 500 vs Index Strategy framework where you participate in growth but are protected from loss.

Most Americans facing retirement are sitting on a tax time bomb they don't even recognize. With over $35 trillion held in tax-deferred retirement accounts like 401(k)s and traditional IRAs, millions of families will face mandatory withdrawals that push them into higher tax brackets precisely when they need income stability most. The question isn't whether taxes will erode your retirement—it's how much. We've worked with professionals and business owners across all fifty states who discovered too late that their nest egg was actually a partnership with the IRS, one where Uncle Sam holds the majority stake and decides when you must withdraw.

The retirement income crisis isn't just about saving enough—it's about keeping what you've saved. Traditional qualified plans force Required Minimum Distributions starting at age seventy-three, converting paper wealth into taxable income whether you need the cash or not. Market volatility compounds the problem: a 30% loss requires a 43% gain just to break even, and most retirees can't afford to wait years for recovery. Meanwhile, management fees quietly drain 1-2% annually, reducing a potential thirty-year nest egg by hundreds of thousands through compound erosion. This triple threat of taxes, volatility, and fees represents what we call the Three Silent Killers of retirement security.

Index Strategies built through Indexed Universal Life Insurance offer a fundamentally different approach to retirement income planning. By participating in S&P 500 index growth while maintaining a contractual zero-loss floor, these strategies create tax-free income streams without Required Minimum Distributions, probate exposure, or forced liquidation during market downturns. As an independent broker with access to seventy-five-plus carrier partnerships, we've seen firsthand how properly structured Index Strategies can bridge the retirement gap between what traditional accounts promise and what they actually deliver after taxes and market corrections. This article examines exactly how Index Strategies create tax-free retirement income, comparing them directly against traditional qualified plans and explaining the mechanics, benefits, limitations, and implementation framework.

How Do Index Strategies Generate Tax-Free Retirement Income?

Index Strategies generate tax-free retirement income through policy loans against accumulated cash value rather than taxable distributions. When structured correctly as Indexed Universal Life Insurance, premiums paid above the death benefit cost accumulate in a cash value account that tracks market index performance—typically the S&P 500—up to a maximum cap rate while a contractual floor prevents losses during down markets. This accumulated cash value grows tax-deferred, and more importantly, can be accessed completely tax-free through policy loans that don't trigger income recognition or taxation events. Unlike 401(k) withdrawals or IRA distributions that add to your adjusted gross income and potentially push you into higher brackets, policy loans remain invisible to the IRS.

The mechanics work through what's called the annual reset mechanism. Each year, any index gains lock into your policy's cash value, establishing a new protected floor for the following year. If the S&P 500 gains twelve percent and your cap rate is ten percent, you capture the full ten percent gain—and that gain can never be taken away by future market losses. Your policy anniversary locks in the growth, resetting your floor to the new higher amount. This creates protected compounding where gains build upon gains without erosion from market corrections. Over twenty to thirty years, this protection mechanism can significantly outpace accounts exposed to full market volatility, despite the cap rate limitation, because you never lose ground and therefore compound from a consistently higher base.

When you're ready to access income during retirement, you request policy loans against the accumulated cash value. These loans aren't taxable events because the IRS treats them as debt, not income. You're essentially borrowing your own money using the policy as collateral. Most carriers charge competitive loan rates between four and six percent, but your cash value typically continues earning index credits even on the borrowed amount through participating loan provisions or wash loan structures. The loan doesn't need to be repaid during your lifetime—it's simply deducted from the death benefit when you pass, with remaining death benefit passing income-tax-free to your beneficiaries. This structure creates a triple tax advantage: tax-deferred accumulation, tax-free access, and tax-free legacy transfer.

This approach satisfies the Tax-Exempt bucket of the Three Tax Buckets Framework. Most Americans over-concentrate in the Tax-Deferred bucket (401k, traditional IRA) where every dollar withdrawn creates taxable income. Some allocate to the Taxable bucket (brokerage accounts, savings) where gains and dividends face annual taxation. Very few maximize the Tax-Exempt bucket where Index Strategies, Roth IRAs, and certain municipal bonds reside. We recommend retirement income diversification across all three buckets to maintain flexibility—but the Tax-Exempt bucket often provides the highest sustainable withdrawal rates because it's not eroded by tax liability or Required Minimum Distribution mandates that force withdrawals during unfavorable market conditions.

What Is the S&P 500 vs Index Strategy Framework?

The S&P 500 has historically delivered strong long-term returns—averaging approximately ten percent annually over the past seventy years—but with full exposure to market losses that can exceed thirty to forty percent during recessions and corrections. Traditional equity investors experience these losses directly: their account values drop, and they must either hold through the decline or sell at a loss. Recovery from significant losses requires disproportionate gains. A thirty percent loss necessitates a forty-three percent gain just to return to break-even. A fifty percent loss requires a one hundred percent gain for recovery. During these recovery periods, traditional investors endure years of stagnant real returns and potentially miss income needs that force them to sell depressed assets.

Index Strategies track S&P 500 performance up to a contractual cap rate—typically ranging from nine to twelve percent depending on carrier and current interest rate environment—while a guaranteed floor ensures you never lose principal when the market drops. You participate in the growth up to your cap. You are protected from the loss entirely. If the S&P 500 gains fifteen percent, you might capture ten percent based on your cap. If the S&P 500 drops thirty percent the following year, you capture zero percent—not negative thirty. This is what we call Zero is Your Hero: your worst year is always zero, never negative, which fundamentally changes the mathematics of compound growth over multi-decade time horizons.

The mathematical advantage becomes clear when comparing sequence-of-returns risk. Consider two investors each starting with one hundred thousand dollars over a ten-year period where the S&P 500 experiences both gains and a severe correction. The traditional S&P 500 investor captures full upside but also full downside: Year 1 (+12%), Year 2 (+8%), Year 3 (-35%), Year 4 (+25%), and so on. After the thirty-five percent loss in Year 3, this investor's account drops to approximately eighty-one thousand dollars and requires years to recover. The Index Strategy investor with a ten percent cap captures Year 1 (+10%), Year 2 (+8%), Year 3 (0%), Year 4 (+10%). By Year 3, the Index Strategy investor maintains approximately one hundred nineteen thousand dollars, never experiencing the devastating drawdown. Over the full decade, despite giving up some upside through the cap, the Index Strategy investor often ends with comparable or superior results because they never had to recover from deep losses.

This framework doesn't suggest Index Strategies will outperform the S&P 500 in every scenario—during extended bull markets with minimal corrections, direct S&P 500 investment may produce higher absolute returns. But for retirement income planning, consistency matters more than peak performance. Retirees can't afford thirty to fifty percent drawdowns when they're taking income. A market correction during the withdrawal phase can permanently impair a portfolio through sequence-of-returns risk, where early losses deplete principal and leave insufficient assets to recover. Index Strategies eliminate this risk entirely by ensuring zero is always your floor. You participate in market growth during good years and sit out market losses during bad years, compounding from a protected base and maintaining stable collateral value for tax-free policy loans throughout retirement.

How Do Index Strategies Compare to 401(k) Plans for Retirement Income?

Traditional 401(k) plans offer valuable employer matching and high contribution limits—up to twenty-three thousand dollars annually for those under fifty—but come with significant structural limitations that erode retirement income. Every dollar withdrawn from a traditional 401(k) adds to your taxable income at your ordinary income tax rate, which for most retirees ranges from twelve to thirty-two percent at the federal level, plus state taxes in higher-tax jurisdictions. Required Minimum Distributions mandated by the IRS force withdrawals starting at age seventy-three regardless of whether you need the income, potentially pushing you into higher brackets and increasing Medicare premium surcharges through Income-Related Monthly Adjustment Amounts (IRMAA). Finally, 401(k) assets receive full market volatility exposure—your account drops when markets correct, potentially forcing you to liquidate depressed assets for needed income.

Index Strategies through Indexed Universal Life Insurance require no mandatory distributions at any age. You control when, how much, and whether to access your cash value through policy loans. This flexibility allows you to manage taxable income strategically—taking larger distributions in low-income years and minimizing withdrawals in high-income years—something impossible with RMD mandates. Policy loans don't appear on your tax return at all, meaning they don't affect your adjusted gross income, your Social Security taxation threshold, or your Medicare premiums. For high-net-worth retirees and professionals in states like California, New York, or New Jersey where combined federal and state marginal rates can exceed forty-five percent, this tax-free access advantage compounds dramatically over a twenty to thirty-year retirement.

The volatility protection difference becomes critical during retirement. We've worked with clients who retired in 2008 just as the S&P 500 dropped thirty-seven percent. Those relying exclusively on 401(k) assets faced a devastating choice: liquidate depressed equities to meet income needs, locking in losses permanently, or drastically reduce living standards until markets recovered. Neither option was acceptable. Clients with Index Strategy foundations maintained their cash value entirely—capturing zero percent for that policy year instead of negative thirty-seven—and continued taking tax-free policy loans at pre-correction levels because their collateral value never decreased. When markets recovered over the following three years, their policy cash values captured the upside through annual reset credits while their 401(k) counterparts were still recovering from realized losses.

From a fee perspective, 401(k) plans often carry hidden costs including expense ratios on underlying mutual funds (typically 0.5% to 1.5%), administrative fees, and sometimes advisor management fees that compound to two percent or more annually. Over thirty-five years, these fees can reduce your final account balance by thirty to forty percent through compound erosion—the difference between retiring with one million dollars or six hundred fifty thousand. Index Strategies have insurance costs including mortality charges and administrative fees, but carriers build these into the cap and floor structure. Your credited rate already reflects all costs, creating transparency. More importantly, the death benefit protection means even if you pass earlier than expected, your beneficiaries receive a tax-free death benefit that typically far exceeds your premium contributions, providing downside protection that 401(k) accounts can't match.

What Are the Contribution Limits and Funding Requirements?

Unlike qualified retirement plans with government-imposed contribution limits, Index Strategies don't have annual contribution caps—but they do have structural guidelines to maintain tax-advantaged status. The IRS requires that Indexed Universal Life Insurance policies remain primarily insurance contracts rather than investment vehicles, which means the death benefit must stay proportional to cash value accumulation. This relationship is defined by the Modified Endowment Contract (MEC) rules that establish maximum premium funding levels relative to death benefit. Funding below the MEC limit ensures your policy maintains tax-free loan access; exceeding the MEC limit converts the policy to MEC status where loans become taxable events similar to annuity withdrawals.

For most properly designed Index Strategies focused on retirement income, we structure premium levels at approximately eighty to ninety percent of the MEC limit, maximizing cash accumulation while maintaining a safety margin. This typically allows significantly higher contributions than qualified plan limits, especially for high-income professionals and business owners who've maxed out 401(k) and IRA options. A forty-five-year-old professional might fund fifty to seventy-five thousand dollars annually into an Index Strategy—three times the 401(k) limit—while maintaining full tax-free growth and access. This makes Index Strategies particularly powerful for those with substantial cash flow who've exhausted traditional retirement vehicles or for business owners building exit strategies and supplemental retirement income outside company-sponsored plans.

Funding flexibility represents another advantage. While consistent annual premiums optimize long-term results, most Index Strategy policies allow flexible premium schedules within the MEC guidelines. You can increase premiums during high-income years, reduce them during business downturns, or even skip years entirely while maintaining coverage through accumulated cash value. This flexibility proves invaluable for entrepreneurs, commission-based professionals, and anyone with variable income. Compare this to 401(k) contributions that require W-2 wage income and operate on rigid annual cycles, or to Roth IRA contributions limited to seven thousand dollars annually with strict income phase-out thresholds that disqualify high earners entirely.

The funding timeline also differs significantly from traditional retirement accounts. Most qualified plan strategies assume thirty-five to forty years of accumulation from age twenty-five or thirty through sixty-five. Index Strategies can be implemented much later—we've designed effective strategies for clients in their fifties and even early sixties—because the death benefit provides downside protection regardless of accumulation period. If you fund a policy for ten years and pass away in year twelve, your beneficiaries receive the full death benefit tax-free, typically exceeding total premiums by multiples. This mortality leverage makes Index Strategies viable even with compressed timelines, though longer funding periods obviously produce higher cash values and greater tax-free retirement income potential. For optimal retirement income design, we typically recommend beginning Index Strategies in your thirties through early fifties, allowing fifteen to thirty years of accumulation before retirement income needs begin.

How Does the Independent Broker Model Benefit Your Strategy?

As an independent broker with partnerships across seventy-five-plus carriers, we work exclusively in the client's best interest without contractual obligations to any single insurance company, bank, or Wall Street institution. This independence fundamentally changes the advice relationship. Captive agents representing single carriers can only offer their company's products regardless of whether those products best serve your specific situation. Even multi-line agents typically have production quotas and preferential commission structures that create subtle conflicts of interest toward certain carriers. Our independent structure eliminates these conflicts entirely—we evaluate your goals, risk tolerance, tax situation, and timeline, then access the entire marketplace to identify which carriers and products optimize your specific outcome.

This matters enormously in the Index Strategy space because carrier performance, cap rates, participation rates, and crediting methods vary significantly. One carrier might offer superior cap rates but lower participation in certain market conditions. Another might provide better loan provisions or more favorable underwriting for clients with specific health histories. Some carriers excel at income riders and guaranteed withdrawal benefits while others optimize pure cash accumulation. Without access to the full marketplace, you might receive a good solution when an optimal solution exists with a different carrier. We've seen cases where the difference between two carriers' cap rate structures produced an additional one hundred fifty thousand dollars in cash value over a twenty-five-year period—money left on the table simply because the advisor lacked access or incentive to search beyond their preferred carrier relationships.

The independent broker model also aligns with the Retail vs Wholesale Banking framework we teach clients. Wall Street operates on retail pricing—selling packaged mutual funds, annuities, and insurance products with embedded fees and commissions that create seven-figure profit margins for institutions. As an independent broker, we access wholesale pricing structures by comparing carriers competitively, eliminating redundant layers, and structuring policies for maximum efficiency. This doesn't mean our services are free—insurance products pay commissions to advisors whether captive or independent—but it means those commissions come from carriers in competitive bid scenarios rather than inflated retail markups. The result is better cap rates, lower internal costs, and higher net cash value accumulation for identical premium outlays.

Our independence also provides continuity and flexibility advantages. If a carrier changes its crediting methods, reduces cap rates significantly, or experiences financial strength rating changes, we can recommend policy adjustments, partial exchanges to better-performing carriers, or strategic rebalancing across multiple policies with different carriers. Captive agents can't offer these options—they're locked into defending their company's changes regardless of client impact. We've helped clients over the years navigate carrier transitions, optimize underwriting across multiple applications, and build diversified Index Strategy foundations across three or four top-rated carriers to eliminate single-carrier concentration risk. This institutional-quality approach to insurance planning simply isn't available through captive distribution channels, giving our clients significant long-term structural advantages in retirement income security and tax efficiency.

What Are the Key Risks and Limitations to Consider?

Index Strategies provide powerful benefits for tax-free retirement income, but they're not universally appropriate for every situation and come with important limitations and considerations. First, these are long-term commitments—typically requiring ten to fifteen years minimum to optimize the cash value-to-premium ratio and recover early policy costs. Surrendering an Index Strategy in the first five to seven years usually produces surrender charges and results in cash values below total premiums paid. Unlike liquid savings accounts or even brokerage accounts, early access to Index Strategy cash value can be costly. This makes Index Strategies inappropriate for emergency funds or short-term goals. They're retirement and legacy planning tools, not liquidity solutions.

Second, cap rates limit your upside participation. During extended bull markets where the S&P 500 produces consistent fifteen to twenty-five percent annual returns—like the 2013-2021 period—direct equity investors capture full gains while Index Strategy holders are capped at nine to twelve percent. Over certain measurement periods, this foregone upside can be substantial. The zero-floor protection provides enormous value during corrections and volatile periods, but during sustained growth cycles, you leave gains on the table. Whether this trade-off is advantageous depends on your specific risk tolerance, time horizon, and overall financial structure. For investors comfortable with volatility and focused purely on wealth accumulation rather than wealth protection, direct S&P 500 investment through low-cost index funds might produce higher long-term returns despite periodic drawdowns. Index Strategies optimize for protection and tax-free income consistency, not maximum absolute returns.

Third, policy loans do carry costs. While the loans themselves aren't taxable, carriers charge loan interest—typically four to six percent annually. Many policies offer participating loan provisions where loaned cash value continues earning index credits, and some carriers provide wash loan structures where the loan interest rate equals or nearly equals the credited rate on loaned values, creating minimal net cost. But these provisions vary by carrier and aren't universal. In some policy structures, particularly if you borrow heavily during low-crediting years, loan interest can compound and gradually erode your death benefit over time. Proper policy monitoring and strategic loan management are essential to prevent loan collapse scenarios where accumulated loan interest exceeds policy value, triggering policy lapse and potentially creating a massive taxable event on all previously accessed cash value.

Fourth, the strategy requires adequate death benefit to maintain the insurance structure. If you underfund the policy or take loans too aggressively early, you might need to add premiums later to keep the policy in force. This differs from a 401(k) where contributions are optional and the account simply reflects invested values. An Index Strategy is a contractual obligation—maintaining it requires either sufficient funding upfront or ongoing premium flexibility. We typically design policies with premium flexibility and stress-test them across various market scenarios to ensure they remain viable even with conservative crediting assumptions, but this requires professional design expertise. Poorly designed policies from inexperienced advisors or captive agents trying to minimize premium can create future funding crises that compromise the entire strategy.

Finally, Index Strategies don't eliminate the need for diversification. They should complement, not replace, other retirement vehicles. We generally recommend Index Strategies as part of a Three Tax Bucket approach: maintain your 401(k) for employer match and tax deferral benefits, fund Roth accounts if eligible, and layer Index Strategies as the tax-free income foundation. This diversification provides withdrawal flexibility, Roth conversion planning opportunities, and balanced exposure across tax treatments. No single vehicle optimizes every goal, which is why comprehensive planning across multiple strategies typically produces superior lifetime outcomes compared to concentration in any single approach regardless of how powerful that individual strategy might be.

S&P 500 vs Index Strategy: Protected Participation

The S&P 500 has historically delivered strong long-term returns—but with full exposure to market losses that can exceed thirty to forty percent during economic crises. Index Strategies track S&P 500 performance up to a contractual cap rate, while a guaranteed floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss. Anchor to Zero is Your Hero.

If the S&P 500 drops thirty percent, a traditional investor loses thirty percent of their account value and needs a forty-three percent gain just to break even—a recovery that can take five to seven years historically. An Index Strategy investor loses zero percent and captures the next market recovery from their full principal base, compounding from a protected foundation. Over twenty to thirty-year retirement income timelines, this protection mechanism can produce comparable or superior outcomes despite the cap rate limitation, because you never experience the devastating drawdowns that permanently impair portfolio values during the critical retirement income years when you're simultaneously taking withdrawals.

This is particularly powerful for retirement income planning where sequence-of-returns risk—the order in which returns occur—can make or break your retirement sustainability. Early losses during retirement withdrawal years deplete principal and leave insufficient assets to participate in eventual recoveries. Index Strategies eliminate this risk by ensuring your cash value never decreases from market corrections, providing stable collateral for tax-free policy loans regardless of broader market conditions. You maintain consistent income access while your principal remains protected and positioned to capture the next market advance through annual reset crediting.

About Steven Rosenberg & Everence Wealth

Steven Rosenberg is the Founder and Chief Wealth Strategist at Everence Wealth, a San Francisco-based independent financial firm specializing in tax-efficient retirement income planning through Index Strategies. As an independent broker with partnerships across seventy-five-plus insurance carriers, Steven serves families, business owners, and professionals across all fifty states who are seeking to build sustainable, tax-free retirement income while protecting their wealth from market volatility and excessive taxation. Unlike captive agents who represent single insurance companies or advisors tied to Wall Street institutions, Steven operates exclusively in the client's best interest without contractual obligations to any carrier, bank, or financial product manufacturer. This independence allows comprehensive marketplace evaluation to identify optimal solutions rather than being limited to predetermined product menus.

Steven's expertise centers on indexed wealth-building strategies that apply the S&P 500 vs Index Strategy framework—capturing market upside through index participation while contractually protecting principal with zero-loss floors. His educational approach focuses on exposing the Three Silent Killers of retirement wealth: excessive fees, market volatility during income years, and tax inefficiency in distribution planning. He developed the Three Tax Buckets Framework to help clients diversify across Taxable, Tax-Deferred, and Tax-Exempt income sources, and regularly teaches the Zero is Your Hero principle that demonstrates how avoiding losses proves more powerful than capturing maximum gains during volatile accumulation and distribution periods. As a licensed insurance professional with deep expertise in Indexed Universal Life Insurance, Fixed Indexed Annuities, and comprehensive retirement income design, Steven works collaboratively with clients' CPAs and estate planning attorneys to integrate Index Strategies within broader wealth management, tax minimization, and legacy planning objectives. His commitment to transparency, mathematical precision, and long-term client relationships has established Everence Wealth as a trusted resource for families seeking independent, conflict-free guidance in an industry often dominated by institutional sales agendas and hidden compensation structures.

Ready to Build Your Tax-Free Retirement Income Strategy?

If you're concerned about Required Minimum Distributions forcing taxable income you don't need, worried about market volatility eroding your retirement principal during withdrawal years, or frustrated by the fees quietly draining your qualified accounts, it's time to explore whether Index Strategies belong in your retirement income foundation. Our Financial Needs Assessment examines your current tax exposure across all three tax buckets, stress-tests your portfolio against sequence-of-returns risk, quantifies the compound impact of fees over your remaining accumulation period, and models how much tax-free income an Index Strategy could generate based on your specific age, health profile, and premium capacity. This comprehensive analysis typically reveals opportunities to redirect existing savings, optimize premium structures across multiple carriers, and integrate Index Strategies with your current 401(k), IRA, and taxable accounts to create a diversified, tax-efficient retirement income plan.

As an independent broker with no institutional conflicts, we'll show you exactly which carriers offer the most competitive cap rates, participation rates, and loan provisions for your situation—and we'll explain precisely how the S&P 500 vs Index Strategy framework protects your wealth while maintaining growth potential. Whether you're a high-income professional who's maxed out qualified plan contributions, a business owner building supplemental retirement income outside your company, or a near-retiree seeking to convert a portion of tax-deferred assets into tax-free income access, we'll design a strategy tailored to your goals. Schedule your confidential Financial Needs Assessment today and discover how Index Strategies can help you keep more of what you've earned, protect your principal from market corrections, and build sustainable tax-free income that lasts throughout retirement.

Schedule Your Financial Needs AssessmentThis content is for educational purposes only and does not constitute financial, tax, or legal advice. Index Strategy performance depends on carrier financial strength, policy design, premium funding levels, and market conditions. Policy loans reduce death benefit and can cause policy lapse if not managed properly. Consult a licensed insurance professional and tax advisor before making any financial decisions. Insurance products are not FDIC insured, are not bank guaranteed, and may lose value.