Indexed Universal Life (IUL) insurance is a permanent life insurance policy that links cash value growth to a market index like the S&P 500, offering downside protection through a zero-percent floor while capturing upside potential up to a cap rate. At Everence Wealth, we help families understand how Index Strategies deliver S&P 500-linked growth with guaranteed principal protection—what we call Zero is Your Hero—creating tax-exempt retirement income without the volatility risk traditional investments carry.

Most Americans have never heard of Indexed Universal Life insurance, yet it represents one of the most mathematically efficient vehicles for building tax-exempt retirement income while maintaining complete principal protection. While Wall Street promotes volatile 401(k)s and tax-deferred IRAs that expose your retirement to market crashes and mandatory distributions, Index Strategies offer a fundamentally different approach: capture market-linked growth when the S&P 500 rises, lose absolutely nothing when it falls, and access your accumulated cash value completely tax-free in retirement.

The challenge isn't that these strategies don't work—it's that most financial advisors can't offer them. Brokers employed by banks and wirehouses are restricted to selling their employer's limited product menu. Independent brokers like Everence Wealth, with access to 75+ carrier partnerships, can design Index Strategy solutions tailored specifically to your retirement timeline, tax situation, and legacy goals. We don't work for insurance companies or Wall Street firms. We work exclusively in your best interest, structuring strategies that Wall Street doesn't want you to discover because they bypass the fee-based system entirely.

This comprehensive guide explains exactly what Indexed Universal Life insurance is, how the mechanics of floor-and-cap protection work, why the S&P 500 versus Index Strategy comparison matters, and how families use these vehicles to build tax-exempt cash flow that isn't subject to required minimum distributions, market volatility, or the compounding destruction of hidden fees. If you're building retirement assets in traditional accounts without understanding the Three Tax Buckets framework, you're likely setting yourself up for a tax time bomb that will detonate exactly when you need your money most.

How Does Indexed Universal Life Insurance Actually Work?

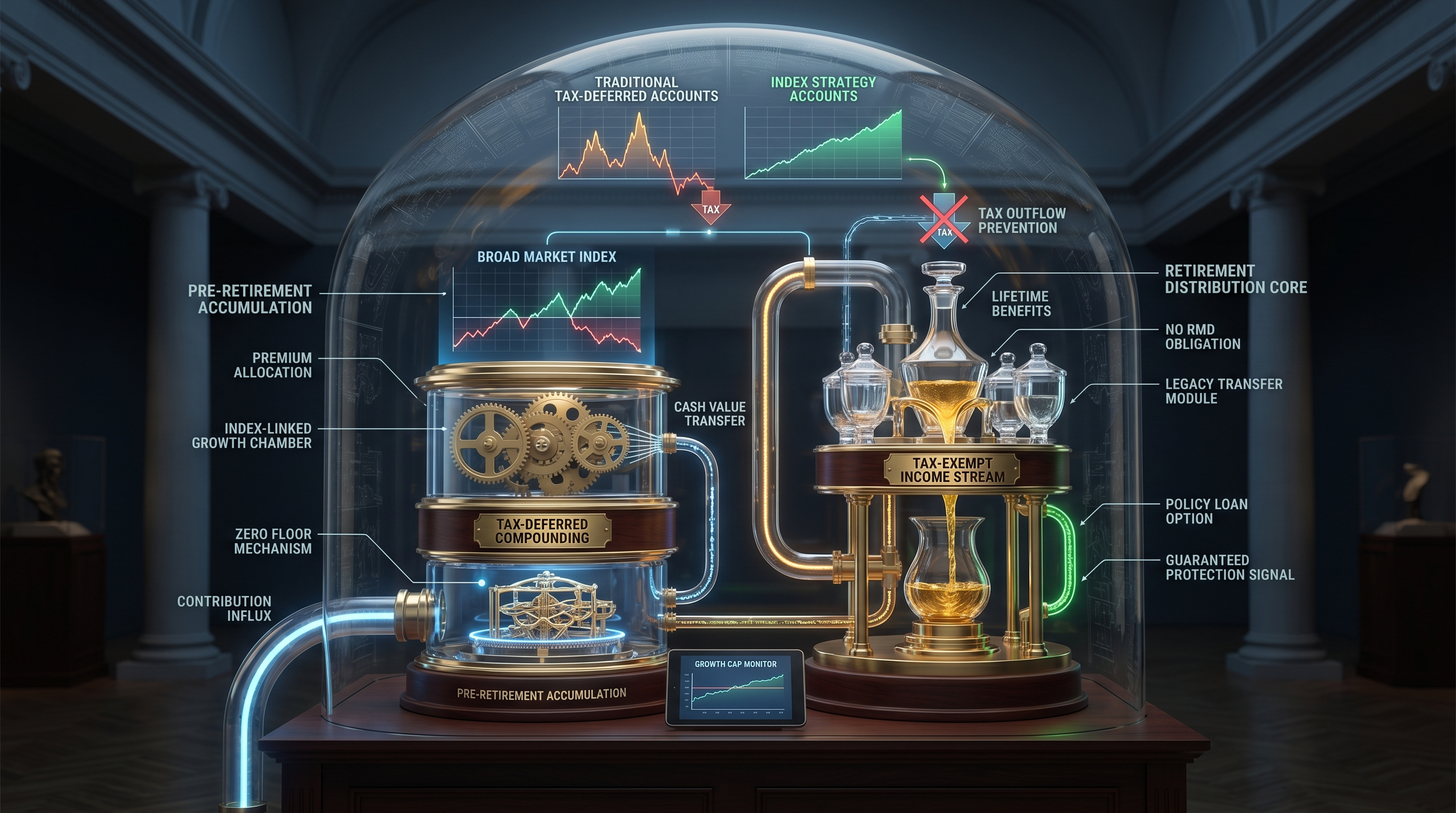

Indexed Universal Life insurance is a permanent life insurance contract that combines a death benefit with a cash value accumulation account linked to the performance of a market index—most commonly the S&P 500. Unlike term life insurance, which expires after a set period, IUL policies remain in force for your entire lifetime as long as premiums are paid or sufficient cash value exists to cover policy costs. The defining feature that separates Index Strategies from traditional whole life or variable universal life is the index crediting mechanism with built-in floor-and-cap protection.

Here's how the math works in practice. When you pay premiums into an IUL policy, a portion covers the cost of insurance (mortality charges, administrative fees, and rider costs), while the remainder flows into your cash value account. This cash value is then credited based on the performance of your chosen index—typically the S&P 500—subject to two critical parameters: a floor and a cap. The floor, usually set at zero percent, guarantees you never lose principal due to market downturns. The cap, which varies by carrier and market conditions but often ranges from eight to twelve percent, limits your upside participation in exchange for that downside protection.

Let's walk through a concrete example. Suppose the S&P 500 gains fifteen percent in a given year, and your policy has a ten percent cap. Your cash value would be credited with a ten percent gain—not the full fifteen, but still a substantial return with zero market risk. Now imagine the following year the S&P 500 crashes thirty percent, as it did in 2008 and again in early 2020. A traditional stock investor loses thirty percent of their account value and must generate a forty-three percent gain just to break even. Your Index Strategy account? It credits zero percent. You don't gain anything that year, but you also don't lose a single dollar. You maintain your full principal base and capture the next market recovery from that protected foundation—this is the essence of Zero is Your Hero.

The annual reset mechanism is equally critical. Each year on your policy anniversary, your gains lock in and become your new protected floor. If your account grows from one hundred thousand dollars to one hundred ten thousand dollars due to a ten percent credit, that one hundred ten thousand becomes your new guaranteed base. Even if the market collapses the following year, your account value cannot drop below one hundred ten thousand. This ratcheting effect creates compounding growth on a protected base—something impossible to achieve with traditional market exposure where previous gains remain vulnerable to future losses.

IUL policies also offer flexible premium payments, unlike traditional whole life insurance with rigid premium schedules. You can increase contributions during high-income years to maximize cash value accumulation, reduce payments during lean periods (as long as sufficient cash value covers policy costs), or even skip payments entirely if your cash value can sustain the policy. This flexibility makes Index Strategies particularly attractive for business owners, commissioned professionals, and families with variable income streams who need adaptable wealth-building tools.

S&P 500 vs Index Strategy: Understanding Protected Participation

The most common question we encounter at Everence Wealth is straightforward: why wouldn't I just invest directly in the S&P 500 through a low-cost index fund instead of accepting a capped return through an Index Strategy? The answer lies in understanding the mathematics of loss recovery and the compounding damage volatility inflicts on retirement portfolios, especially during the critical decade immediately before and after retirement—what financial researchers call the sequence-of-returns risk window.

S&P 500 vs Index Strategy: Protected Participation

The S&P 500 has historically delivered strong long-term returns—approximately ten percent annualized over the past century—but with full exposure to market losses that can devastate retirement plans when they occur at the wrong time. Index Strategies track S&P 500 performance up to a cap rate, while a guaranteed floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss.

If the S&P 500 drops thirty percent, a traditional investor loses thirty percent of their account value and needs a forty-three percent gain just to break even—a mathematical reality that often takes years to achieve. An Index Strategy investor loses zero percent and captures the next market recovery from their full principal base—compounding from a protected foundation. A fifty percent market loss requires a one hundred percent gain to recover. These aren't abstract numbers; they represent the difference between a secure retirement and running out of money at age eighty-two.

Consider two investors, both age fifty-five with five hundred thousand dollars, planning to retire at sixty-five. Investor A places everything in an S&P 500 index fund. Investor B structures an Index Strategy with a zero-percent floor and ten-percent cap. Over the next decade, assume the market delivers three years of fifteen percent gains, two years of eight percent gains, two years of negative five percent, one year of negative twelve percent, one year of negative twenty-five percent, and one year of twelve percent—a realistic sequence incorporating normal volatility.

Investor A experiences the full roller coaster: massive gains followed by devastating losses that erase years of progress. Their account balance at retirement depends entirely on whether the negative years occurred early or late in the sequence—sequence-of-returns risk in action. Investor B captures the positive years up to their ten-percent cap (crediting ten percent in years the market gained fifteen or twelve percent, eight percent when the market gained eight percent), but credits zero in all negative years—never losing principal. The Index Strategy investor reaches retirement with a protected base that compounded without interruption, while the S&P 500 investor's outcome varies wildly based purely on the timing of market crashes they couldn't control.

This protection becomes even more valuable when you consider taxes. Direct S&P 500 investments in taxable accounts generate annual capital gains taxes, dividend taxes, and ultimately ordinary income taxes when converted to retirement income through traditional IRAs or 401(k)s. Index Strategies accumulate cash value with tax-deferred growth, then allow tax-free access through policy loans in retirement—completely bypassing the tax system. This places Index Strategies in the Tax-Exempt bucket of the Three Tax Buckets framework, alongside Roth IRAs and municipal bonds, but without contribution limits, income restrictions, or required minimum distributions.

The trade-off for this protection is the cap rate—you sacrifice unlimited upside potential in exchange for eliminating all downside risk. For families prioritizing retirement income security over maximum wealth accumulation, particularly those within fifteen years of retirement, this trade-off makes mathematical and emotional sense. You're not trying to hit a home run; you're trying to ensure you never strike out.

The Three Tax Buckets Framework: Where Index Strategies Fit

At Everence Wealth, we structure every comprehensive retirement plan around the Three Tax Buckets framework—a strategic approach to diversifying not just your assets, but your tax exposure across retirement. Most Americans concentrate their entire retirement savings in a single tax bucket, creating a massive vulnerability that detonates exactly when they begin withdrawals. Understanding where Indexed Universal Life fits within this framework is essential for building truly tax-efficient retirement income.

The first bucket is your Taxable accounts—individual brokerage accounts, savings accounts, certificates of deposit, and non-qualified investments. Every year these accounts generate taxable interest, dividends, and capital gains whether you withdraw money or not. The ongoing tax drag reduces your compound growth significantly over thirty to thirty-five years. Using the Rule of 72, even a one-percent annual tax drag doubles the time required to double your money. If you're earning seven percent but paying one percent in annual taxes on growth, your effective return drops to six percent—extending your doubling time from 10.3 years to twelve years. Over a thirty-five-year career, that difference compounds to hundreds of thousands of dollars in lost wealth.

The second bucket is Tax-Deferred accounts—traditional 401(k)s, traditional IRAs, 403(b)s, and SEP IRAs. These vehicles give you an upfront tax deduction when you contribute, grow without annual taxation, but then tax every dollar you withdraw in retirement as ordinary income at whatever rates Congress decides to impose decades from now. The trap most Americans fall into is accumulating millions in these accounts without considering the tax consequences when required minimum distributions (RMDs) begin at age seventy-three. When you're forced to withdraw increasing percentages each year, your taxable income spikes—triggering higher Medicare premiums, increasing the taxable portion of Social Security benefits, potentially pushing you into higher tax brackets, and reducing the net income you actually keep. We call these accounts tax-postponed, not tax-deferred, because you haven't eliminated the tax liability—you've simply delayed it until a time when you have less control and Congress may have raised rates.

The third bucket is Tax-Exempt accounts—Roth IRAs, Roth 401(k)s, Health Savings Accounts (when used for qualified medical expenses), and properly structured Indexed Universal Life insurance. Money in these accounts grows without annual taxation and can be accessed in retirement completely tax-free. This is the most powerful bucket for retirement income because every dollar you withdraw is a dollar you keep—no IRS involvement, no required distributions, no impact on Social Security taxation or Medicare premiums. Index Strategies function as a Roth IRA without contribution limits, income restrictions, or mandatory waiting periods. You can fund an IUL policy with fifty thousand, one hundred thousand, or even several hundred thousand dollars annually (subject to IRS guidelines to maintain tax-advantaged status), accumulate tax-deferred cash value, and access it tax-free through policy loans starting as early as your fifties if structured properly.

The strategic goal is balance across all three buckets. Having money in taxable accounts provides liquidity and flexibility without penalties. Having money in tax-deferred accounts captures employer matches and upfront deductions. But having substantial money in tax-exempt accounts—particularly Index Strategies with principal protection—gives you the freedom to control your retirement tax bill, weather market downturns without panic, and pass wealth to heirs without generating massive taxable events. Families who concentrate everything in tax-deferred accounts discover too late they've built a retirement funded with after-tax dollars despite receiving upfront deductions—the IRS simply waited patiently for decades to collect.

How Index Strategy Cash Value Accumulation Works Over Time

Understanding the long-term accumulation curve of an Index Strategy is essential for setting realistic expectations and structuring policies correctly. Unlike qualified retirement accounts where you simply contribute a percentage of salary each year and hope for compound growth, IUL policies require strategic design—balancing premium payments, policy costs, death benefit levels, and crediting rates to maximize cash value while maintaining tax-advantaged status under IRS rules.

In the early years of an IUL policy, cash value accumulation feels slow. A significant portion of your premium covers mortality charges (the cost of the death benefit), administrative fees, premium loads, and rider charges for any additional benefits like chronic illness or disability waivers. This front-loading of costs is a legitimate criticism of permanent life insurance and why these strategies require long-term commitment—typically fifteen to twenty years minimum to realize their full value. If you surrender a policy in years three or four, you'll likely receive less cash value than total premiums paid due to these early costs.

However, as you move into years seven through fifteen, the accumulation curve accelerates dramatically. Your mortality costs remain relatively stable or increase slowly if you purchased the policy at a younger age, while your cash value base grows larger each year—generating larger index credits even at the same percentage rate. This is compound growth working in your favor on a protected base. Annual reset mechanisms lock in gains, creating a rising floor that protects increasingly larger account values from market downturns. By year ten, your cash value may exceed total premiums paid by twenty to thirty percent depending on index performance, and from that point forward the gap widens exponentially.

Years fifteen through thirty represent the peak accumulation phase where Index Strategies truly demonstrate their value. Your cash value has compounded for over a decade without losses, your policy costs have stabilized, and your account continues capturing market-linked gains while avoiding all market-linked losses. At this stage, many families begin taking tax-free policy loans to supplement retirement income, fund college expenses, or cover unexpected financial needs—all without creating taxable events or triggering early withdrawal penalties. The remaining cash value continues growing even while you're accessing funds, since policy loans don't actually withdraw money from your cash value—they're loans from the insurance company's general account collateralized by your policy's cash value.

This loan mechanism is critical to understand and represents one of the most powerful features of Index Strategies. When you need income, you don't surrender cash value—you borrow against it. The insurance company charges loan interest (often five to six percent annually), but your full cash value remains in the policy continuing to receive index credits. If your policy credits eight percent and you're paying five percent loan interest, you're experiencing a positive arbitrage of three percent on borrowed funds—generating spread income on money you're actively using. These loans never require repayment during your lifetime. When you pass away, the insurance company deducts outstanding loans plus accumulated interest from the death benefit and pays the remainder to your beneficiaries income-tax-free. You've effectively converted your cash value to retirement income without ever triggering a taxable event.

Properly structured, an Index Strategy can deliver thirty to forty years of tax-free supplemental retirement income starting in your sixties, maintain a death benefit to protect your spouse and heirs, and accomplish all of this without exposure to stock market crashes, required minimum distributions, or the sequence-of-returns risk that destroys traditionally invested retirement accounts. This isn't a get-rich-quick scheme—it's a methodical, mathematically sound approach to building guaranteed retirement cash flow that banks, wirehouses, and Wall Street firms cannot replicate with their fee-based investment products.

Who Should Consider Indexed Universal Life Insurance?

Index Strategies aren't appropriate for everyone, and we're explicit about this at Everence Wealth. These vehicles work best for specific financial profiles—families and individuals who have maxed out traditional retirement accounts, face high current or future tax exposure, need asset protection from lawsuits or creditors, want to pass wealth efficiently to heirs, or simply cannot tolerate the emotional volatility of market-based investing during the critical years approaching retirement.

High-income professionals—physicians, attorneys, business owners, executives, and commissioned sales professionals—represent ideal candidates for IUL policies. These individuals typically earn too much to contribute to Roth IRAs (income limits phase out contributions for individuals earning over a certain threshold), have already maximized 401(k) or SEP IRA contributions, and face substantial tax liabilities both now and in retirement. An Index Strategy allows them to redirect additional capital into tax-advantaged accumulation without contribution limits, building a tax-exempt income stream that doesn't appear on tax returns and won't trigger higher Medicare premiums or Social Security taxation when accessed in retirement.

Business owners benefit particularly from the flexibility IUL policies provide. Variable income years are common in entrepreneurship—some years generate significant profits while others produce modest returns or even losses. The flexible premium structure of Index Strategies allows owners to fund policies heavily during profitable years, reduce or skip premiums during lean years (if cash value can cover costs), and maintain the strategy long-term without the rigid requirements traditional whole life insurance imposes. Additionally, business owners face lawsuit and creditor risks that employees typically don't encounter. In many states, cash value life insurance receives significant asset protection—shielding accumulated wealth from business liabilities, malpractice claims, or bankruptcy proceedings.

Families with special needs dependents find Index Strategies invaluable for legacy planning. The combination of guaranteed death benefit plus accumulated cash value creates a vehicle that can fund special needs trusts, provide lifetime income for disabled children, or replace parent income when primary caregivers pass away—all with tax-advantaged growth and protection from market volatility. These families can't afford to see college funds or care accounts devastated by market crashes during critical transition periods, making the zero-floor protection essential rather than optional.

Pre-retirees within ten to fifteen years of retirement increasingly turn to Index Strategies as a way to reduce portfolio risk without sacrificing growth potential. Sequence-of-returns risk—the danger that market crashes occurring early in retirement will permanently reduce your sustainable withdrawal rate—is one of the most serious threats to retirement security. By moving a portion of retirement assets into Index Strategies during the peak accumulation years before retirement, families create a protected income floor that cannot be eroded by market crashes. They maintain equity exposure for growth through remaining investments while eliminating downside volatility in the portion designated for essential retirement expenses.

Conversely, Index Strategies are generally not appropriate for young professionals in their twenties still building emergency funds and paying down student loans, individuals who lack consistent surplus income to fund premiums long-term, families who may need full liquidity within five to seven years, or people seeking maximum wealth accumulation without regard to protection or taxes. For those profiles, term life insurance for pure protection plus low-cost index funds for growth usually make more sense. The value of IUL policies emerges over time—typically fifteen-plus years—which requires patience and consistent funding that not every financial situation can support.

Common Misconceptions and Criticisms About IUL Insurance

Indexed Universal Life insurance attracts significant criticism from fee-based financial advisors, and it's important to address these concerns directly and honestly. Some criticisms are legitimate and reflect poorly designed policies sold by inexperienced agents focused on commissions rather than client outcomes. Other criticisms stem from fundamental misunderstandings about how these vehicles work or from conflicts of interest where advisors can't earn fees managing insurance assets and therefore dismiss the entire category.

The most common criticism is that IUL policies are too expensive compared to buying term insurance and investing the difference in low-cost index funds. This argument has merit if you're comparing pure costs in isolation and assuming uninterrupted market growth over thirty years. However, it completely ignores three critical factors: tax treatment, downside protection, and the forced savings discipline permanent insurance creates. The buy-term-invest-the-difference strategy assumes you'll actually invest the difference consistently for three decades without panic-selling during market crashes, that you'll hold investments in tax-efficient accounts, and that you won't encounter sequence-of-returns risk when you need the money most. Real-world investor behavior studies consistently show that average investors significantly underperform market indexes because they buy high, sell low, and abandon strategies during volatility. Index Strategies eliminate this behavioral risk through contractual structure.

Critics also point to policy illustrations showing optimistic crediting rates that may not materialize in reality. This criticism is entirely valid when agents run illustrations at maximum historical rates and present them as guaranteed outcomes. At Everence Wealth, we stress-test every policy illustration at multiple crediting scenarios—six percent, five percent, and four percent annually—to show clients how their policy performs under conservative assumptions. We also compare guaranteed policy values (the absolute minimum the carrier contractually promises) against illustrated values to ensure families understand the range of outcomes. Transparency about crediting rate assumptions is non-negotiable for ethical policy design.

Another frequent concern is that caps reduce upside participation and therefore IUL policies will underperform direct S&P 500 investment over time. This argument assumes markets consistently deliver above-cap returns without significant downturns—an assumption that ignores history. Since 2000, the S&P 500 has experienced two fifty-percent crashes (dot-com bubble and financial crisis) plus multiple corrections exceeding twenty percent. During these periods, Index Strategy holders credited zero percent while stock investors lost three to five years of gains. The subsequent recovery period favors stock investors during bull markets, but the protection during bear markets often produces similar long-term accumulation with far lower volatility and none of the emotional trauma that causes investors to abandon strategies at exactly the wrong time.

Some critics dismiss IUL policies as complex and difficult to understand compared to straightforward Roth IRAs or 401(k)s. Complexity is a fair concern—these contracts involve moving parts including mortality charges, policy loans, crediting methods, and annual reset mechanics that require education to fully grasp. However, complexity isn't inherently negative if it delivers superior outcomes for specific situations. Airplanes are complex, but we don't avoid flying because cars are simpler. The question is whether the complexity serves a purpose—and for families needing tax-exempt accumulation beyond Roth IRA limits, downside protection during volatile markets, or asset protection from creditors, the complexity of IUL policies delivers benefits unavailable through simpler alternatives.

Finally, there's the legitimate concern about policy lapses and surrenders. If you terminate an IUL policy in early years, you'll likely recover less than you paid in premiums due to front-loaded costs. This makes these strategies unsuitable for anyone without confidence in their ability to fund premiums for at least fifteen to twenty years. We address this at Everence Wealth by qualifying clients carefully, ensuring surplus income exists beyond emergency funds and qualified retirement contributions, and designing policies with flexible premiums that can be reduced or paused if financial circumstances change. The worst outcome is a lapsed policy after five years—all costs incurred with none of the long-term benefits realized.

About Steven Rosenberg & Everence Wealth

Steven Rosenberg is the Founder and Chief Wealth Strategist at Everence Wealth, a San Francisco-based independent insurance brokerage specializing in tax-efficient Index Strategies and retirement planning for families across all fifty states. As an independent broker with access to seventy-five-plus carrier partnerships, Steven works exclusively in the client's best interest—not for any insurance company, bank, or Wall Street institution. His expertise centers on helping high-income professionals, business owners, and pre-retirees build tax-exempt retirement income through S&P 500-linked Index Strategies with zero-floor protection, eliminating the sequence-of-returns risk and tax time bombs that traditional retirement accounts create. Steven is a licensed insurance professional who has structured Index Strategy solutions for physicians, attorneys, entrepreneurs, and families seeking alternatives to the fee-based Wall Street system. His educational approach focuses on frameworks including Zero is Your Hero (protected compounding from a guaranteed floor), the Three Tax Buckets (diversifying tax exposure across taxable, tax-deferred, and tax-exempt accounts), and Cash Flow Over Net Worth (prioritizing sustainable retirement income streams over paper asset accumulation). Everence Wealth serves clients nationwide, providing comprehensive Financial Needs Assessments that stress-test retirement strategies against market volatility, tax exposure, and longevity risk—identifying gaps traditional advisors often overlook and designing solutions that protect principal while capturing market-linked growth.

Taking the Next Step: Evaluating If Index Strategies Fit Your Plan

If you've read this far, you likely recognize that Indexed Universal Life insurance represents a fundamentally different approach to retirement planning than the 401(k)-centric model Wall Street and human resources departments have promoted for the past forty years. The question isn't whether Index Strategies are objectively better or worse than traditional investments—it's whether they solve specific problems in your unique financial situation that other vehicles cannot address as effectively.

Start by honestly assessing your current retirement trajectory. Have you maximized contributions to employer retirement plans and Roth IRAs? Do you have substantial assets concentrated in tax-deferred accounts that will generate massive required minimum distributions and tax bills in retirement? Are you within fifteen years of retirement and concerned about market volatility eroding your account exactly when you need it most? Do you own a business or practice that exposes you to liability risks, making asset protection a priority? Are you a high-income earner who has exhausted traditional tax-advantaged savings options and needs additional vehicles for wealth accumulation? If you answered yes to multiple questions, Index Strategies deserve serious consideration as part of your comprehensive plan.

Next, recognize that not all IUL policies are created equal—carrier selection, policy design, crediting methods, and fee structures vary significantly across the seventy-five-plus carriers independent brokers can access. This is why working with an independent broker rather than a captive agent matters enormously. Captive agents represent a single insurance company and can only offer that company's products regardless of whether they're the best fit for your situation. Independent brokers like Everence Wealth can evaluate your specific goals, compare solutions across dozens of carriers, and design a policy optimized for your tax situation, risk tolerance, retirement timeline, and legacy objectives. We don't have conflicts of interest pushing you toward products that generate higher commissions—we have access to wholesale pricing and carrier competition that drives better client outcomes.

The Financial Needs Assessment we conduct at Everence Wealth goes far beyond product selection. We analyze your complete financial picture—income sources, tax exposure across all three tax buckets, current investment allocation, risk tolerance, retirement income needs, estate planning goals, and protection gaps that could devastate your family if disability or premature death occurs. We stress-test your current strategy against historical market scenarios including the 2000-2002 bear market, the 2008 financial crisis, and the 2020 pandemic crash to show you how sequence-of-returns risk could impact your actual retirement date and sustainable withdrawal rate. Then we model Index Strategy integration—showing how protected accumulation with tax-free access changes your retirement income security, reduces tax exposure, and eliminates the forced-distribution requirements that trigger so many unintended consequences for retirees.

This assessment doesn't obligate you to purchase anything. It's an educational process designed to give you clarity about where your current trajectory leads, what risks you're exposed to, and what alternatives exist beyond the limited menu your employer's 401(k) or local bank branch offers. Many families discover they're on track and need only minor adjustments. Others realize they've built a retirement plan on a foundation of tax-deferred accounts and volatile equities that could collapse if markets crash during the critical five-year window before and after retirement. Both outcomes provide value—either confirmation you're structured correctly or identification of problems while you still have time to address them.

Schedule Your Personalized Financial Needs Assessment

Everence Wealth provides comprehensive Financial Needs Assessments for families serious about building tax-efficient, volatility-protected retirement income through Index Strategies and integrated planning. During your assessment, we'll analyze your current retirement trajectory, identify tax exposure across your three tax buckets, stress-test your portfolio against historical market crashes, and model how Index Strategies with S&P 500-linked growth and zero-floor protection could enhance your retirement security. As an independent broker with seventy-five-plus carrier partnerships, we'll design solutions tailored specifically to your situation—not limited to a single company's product menu. Whether you're a high-income professional who has maxed out traditional retirement accounts, a business owner seeking asset protection and tax efficiency, or a pre-retiree concerned about market volatility during your transition to retirement, we'll provide clarity on how Index Strategies fit within your comprehensive plan. Schedule your assessment today and discover why thousands of families have chosen the independent broker advantage over the retail financial system Wall Street promotes.

Schedule Your Financial Needs AssessmentThis content is for educational purposes only and does not constitute financial, tax, or legal advice. Indexed Universal Life insurance policies involve costs, limitations, and restrictions including caps on credited interest, mortality charges, and surrender periods. Policy performance depends on index crediting rates which vary annually and are not guaranteed. Consult a licensed insurance professional and tax advisor to determine if Index Strategies are appropriate for your specific situation before making any financial decisions.