Indexed Universal Life (IUL) is a permanent life insurance policy that links cash value growth to a market index like the S&P 500, offering downside protection with a zero percent floor while capping upside potential. Everence Wealth specializes in Index Strategies that use the S&P 500 vs Index Strategy framework—you participate in market growth while your principal is protected from loss. Zero is Your Hero.

Most Americans have been taught the same financial playbook: max out your 401k, hope the market cooperates, and pray taxes don't eat your retirement alive. But what if there was a strategy that combined life insurance protection with tax-advantaged growth linked to the S&P 500—without the devastating losses that come with market downturns? That's exactly what Indexed Universal Life insurance delivers, and it's why families across the country are reexamining their retirement blueprints.

Traditional retirement vehicles expose you to three silent wealth destroyers: excessive fees, market volatility, and compounding tax liability. Index Strategies, anchored by Indexed Universal Life policies, address all three simultaneously. When structured properly through an independent broker with access to 75+ carrier partnerships, these instruments provide permanent death benefit protection while accumulating cash value that tracks market index performance—with a guaranteed floor that ensures your worst year is zero percent, not a devastating double-digit loss that requires years to recover from.

We've spent decades helping families bridge the retirement gap by diversifying across all Three Tax Buckets—taxable, tax-deferred, and tax-exempt. Index Strategies occupy the tax-exempt bucket, offering policy loans that aren't classified as taxable income and accumulation that grows without triggering annual 1099 reporting. This isn't theory. This is the mathematical reality of how institutional investors and high-net-worth families protect and compound wealth outside the traditional Wall Street retail system.

How Does Indexed Universal Life Insurance Actually Work?

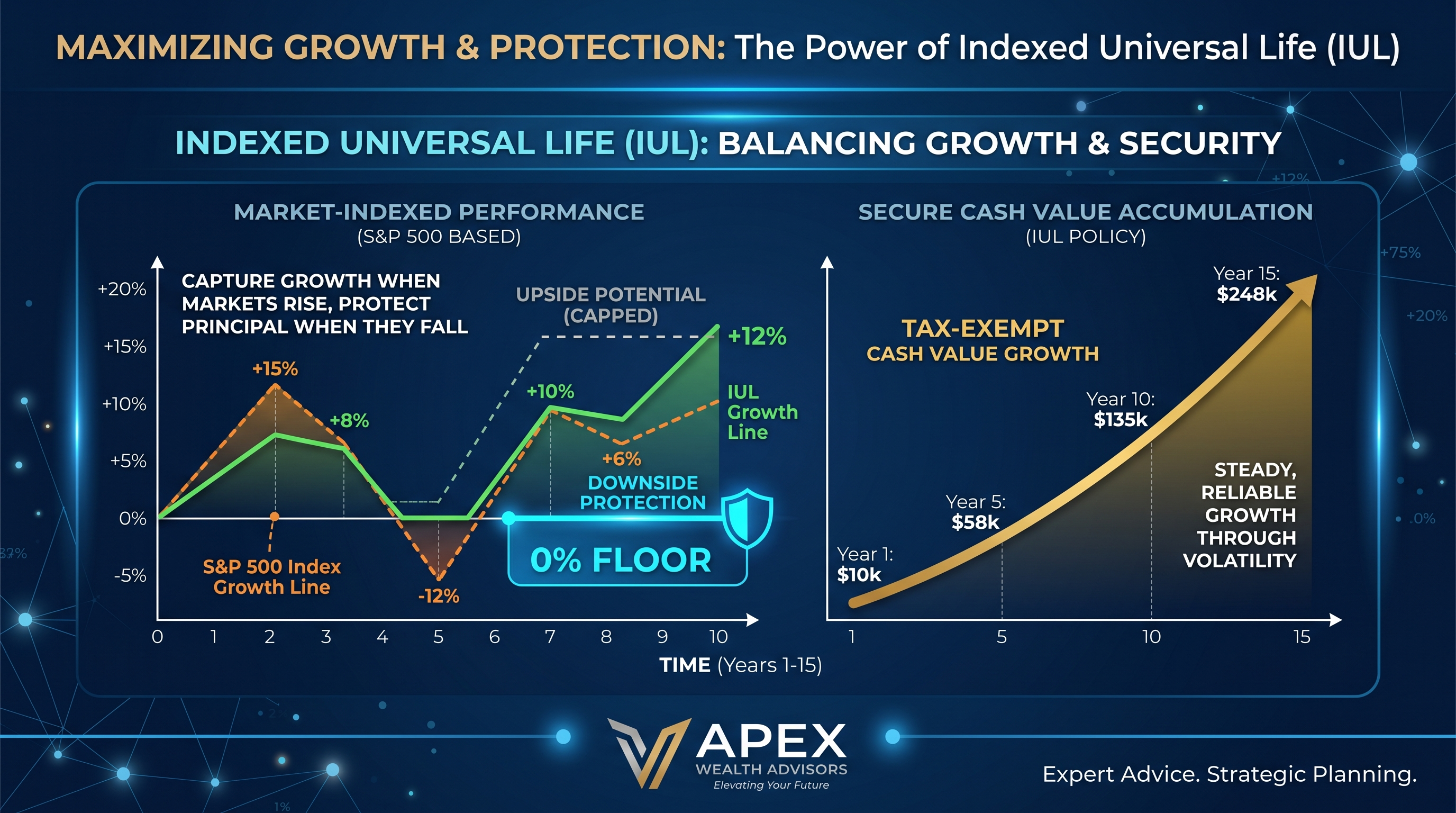

Indexed Universal Life insurance is a permanent life insurance contract that allocates premium payments into two components: cost of insurance (mortality charges, administrative fees, and rider costs) and cash value accumulation. The cash value portion is credited based on the performance of an underlying market index—most commonly the S&P 500—subject to a floor (typically zero percent) and a cap (which varies by carrier, strategy, and current interest rate environment). This structure means you participate in market gains up to the cap rate, but you never experience negative returns when the market drops.

Here's the critical distinction that separates Index Strategies from direct stock market investing: when the S&P 500 falls 30 percent, a traditional investor loses 30 percent of their principal and needs a 43 percent gain just to break even. An Index Strategy investor loses zero percent and captures the next market recovery from their full principal base. This protected compounding is what we call Zero is Your Hero—your account resets annually, locking in gains and protecting your new higher base from future downturns. Over a 30- or 35-year accumulation period, avoiding just two or three major market corrections can dramatically outpace gross returns that include devastating drawdowns.

The mechanics are straightforward but powerful. Each year, the insurance carrier measures index performance from the policy anniversary date. If the index is up 12 percent and your cap is 10 percent, you're credited 10 percent. If the index is down 25 percent, you're credited zero percent—but your principal remains intact. This annual reset mechanism ensures that gains lock in permanently and future crediting starts from a protected floor. Unlike mutual funds or ETFs that can lose value in subsequent years, Index Strategy cash value only moves in one direction: sideways (zero percent) or up.

What Is the S&P 500 vs Index Strategy Framework?

The S&P 500 has historically delivered strong long-term returns—but with full exposure to market losses that can devastate retirement timelines. Index Strategies track S&P 500 performance up to a cap rate, while a guaranteed floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss. This is the fundamental tradeoff that retirees and pre-retirees must understand when comparing accumulation vehicles.

If the S&P 500 drops 30 percent, a traditional investor loses 30 percent and needs a 43 percent gain just to break even. An Index Strategy investor loses zero percent and captures the next market recovery from their full principal base—compounding from a protected base. Over a full market cycle that includes both bull runs and corrections, the mathematical advantage of avoiding losses often surpasses the benefit of unlimited upside, especially when you factor in sequence-of-returns risk during the retirement distribution phase.

This framework is especially critical for individuals within ten years of retirement. A single major correction at the wrong time can delay retirement by five to seven years or force permanent reductions in lifestyle. Index Strategies eliminate sequence-of-returns risk by ensuring that no matter what the market does, your cash value never declines due to market performance. You still have mortality and expense charges, but those are predictable and disclosed—not the hidden, unpredictable destruction caused by a market crash at age 62.

S&P 500 vs Index Strategy: Protected Participation

The S&P 500 has historically delivered strong long-term returns—but with full exposure to market losses. Index Strategies track S&P 500 performance up to a cap rate, while a guaranteed floor ensures you never lose principal when the market drops. You participate in the growth. You are protected from the loss. If the S&P 500 drops 30 percent, a traditional investor loses 30 percent and needs a 43 percent gain just to break even. An Index Strategy investor loses zero percent and captures the next market recovery from their full principal base—compounding from a protected base. This is what we call Zero is Your Hero. Your worst year is always zero percent, never negative, and that single feature transforms long-term wealth accumulation by eliminating the mathematical devastation of recovery periods that consume years of compounding opportunity.

What Are the Core Benefits of Indexed Universal Life Insurance?

The primary benefit of Indexed Universal Life is permanent death benefit protection combined with tax-advantaged cash value accumulation. Unlike term life insurance, which expires after a set period, IUL policies remain in force for your entire lifetime as long as premiums are paid or cash value is sufficient to cover costs. This permanent coverage provides estate planning certainty, ensuring your beneficiaries receive a tax-free death benefit regardless of when you pass away—whether that's next year or in four decades.

The cash value component grows on a tax-deferred basis, meaning you don't pay annual taxes on credited gains. More importantly, policy loans and withdrawals can be structured to avoid taxable income entirely. When you borrow against your cash value, the IRS does not classify that loan as income—it's a loan against your own asset, similar to a home equity line of credit. This creates a tax-exempt income stream during retirement that doesn't trigger higher Medicare premiums, Social Security taxation thresholds, or adjusted gross income increases that phase out deductions.

Index Strategies also offer flexibility that qualified retirement plans cannot match. There are no contribution limits like the $23,000 annual cap on 401k deferrals or the $7,000 Roth IRA limit. High-income earners who are phased out of Roth contributions can fund Index Strategies with six-figure annual premiums if underwriting and policy design support it. There are no required minimum distributions at age 73, no penalties for accessing funds before age 59½, and no mandatory tax reporting unless you surrender the policy for a gain. This makes Index Strategies uniquely suited for individuals who have maxed out qualified plan contributions and need additional tax-advantaged accumulation capacity.

How Do Index Strategies Address the Three Silent Killers?

We talk constantly about the Three Silent Killers—fees, volatility, and taxes—because they compound against you over 30 to 35 years and erode more wealth than most investors realize. A 401k with a 1.5 percent annual fee might seem trivial, but compounded over 35 years, that fee consumes more than 40 percent of what your account could have grown to. Use the Rule of 72: divide 72 by your fee percentage to see how long it takes fees to cut your wealth in half. At 1.5 percent, that's 48 years—but over a 35-year working career, you're halfway there. Index Strategies typically have transparent costs—mortality charges, administrative fees, and rider expenses—that are disclosed upfront and often lower than the all-in costs of managed brokerage accounts when you include advisory fees, fund expense ratios, and trading costs.

Volatility is the second silent killer, and it's the one most investors underestimate. A 30 percent loss requires a 43 percent gain to break even. A 40 percent loss requires a 67 percent gain. A 50 percent loss requires a 100 percent gain. The math is brutal, and it's why two investors with identical average returns can end up with vastly different account balances depending on the sequence and magnitude of their losses. Index Strategies eliminate downside volatility entirely with the zero percent floor. Your cash value might grow slowly in low-return years, but it never goes backward due to market performance, which means you're always compounding from your highest previous balance—not recovering from a crater.

Taxes are the third silent killer, and they're the most insidious because they're deferred and therefore ignored. Every dollar in a traditional 401k or IRA is a partnership with the IRS—your balance is pre-tax, and you'll owe ordinary income tax on every distribution. If tax rates rise, your retirement income drops. If Required Minimum Distributions force you into higher brackets, you lose more to taxes. If Social Security becomes taxable because your RMDs push your provisional income over the threshold, you're taxed twice. Index Strategies solve this by living in the tax-exempt bucket—policy loans are not taxable income, and death benefits pass income-tax-free to beneficiaries. This isn't tax evasion; it's tax efficiency using the same strategies that wealthy families and institutions have used for generations.

What Should You Know About Policy Costs and Fees?

Indexed Universal Life policies are not free—no financial instrument is—but the cost structure is transparent and predictable when you work with an independent broker who has access to 75+ carriers and can design policies competitively. The primary costs include cost of insurance (which increases with age), administrative fees (often a flat monthly charge or percentage of premium), and optional rider fees for benefits like chronic illness, critical illness, or disability waiver of premium. These costs are deducted from your cash value, which is why proper policy design and adequate funding are essential to long-term performance.

One of the biggest misconceptions about IUL is that fees make it uncompetitive with mutual funds or ETFs. In reality, when you add up 401k recordkeeping fees, fund expense ratios (often 0.50 to 1.50 percent annually), advisory fees (typically one percent of assets), and the tax drag from annual distributions and rebalancing, the all-in cost of a managed brokerage account frequently exceeds the cost structure of a well-designed Index Strategy—especially when you account for the tax-free policy loan feature that eliminates the tax liability on distributions. The question isn't whether there are costs; the question is whether the costs are justified by the benefits, and in the case of Index Strategies with permanent death benefit protection, tax-exempt income potential, and zero-floor crediting, the answer for many families is yes.

Transparency is critical. When you work with Everence Wealth, we illustrate every fee, charge, and assumption in your policy proposal. You see exactly what the carrier deducts, what gets credited to cash value, and how different funding levels and market scenarios impact long-term performance. This is the difference between working with an independent broker who represents 75+ carriers and working with a captive agent who can only sell one company's products. We have no incentive to sell you the wrong policy—we build strategies that align with your goals, risk tolerance, and tax situation, and we disclose every cost so you can make an informed decision.

How Do Index Strategies Fit Into the Three Tax Buckets Framework?

The Three Tax Buckets framework is the foundation of intelligent retirement planning, and it's how we help families avoid the single-bucket trap that most Americans fall into. The three buckets are: taxable (brokerage accounts, savings accounts, CDs), tax-deferred (401k, 403b, traditional IRA), and tax-exempt (Roth IRA, Roth 401k, HSA, and Index Strategies). Most people overweight the tax-deferred bucket because that's what their employer offers and what traditional financial advisors push. But when you retire, every dollar you pull from a tax-deferred account is taxed as ordinary income, and if tax rates rise—or if you're successful and accumulate a large balance—you can easily find yourself in a higher tax bracket in retirement than you were during your working years.

Index Strategies live in the tax-exempt bucket, and they're one of the few vehicles that allow unlimited contributions without income phase-outs or annual caps. Roth IRAs are fantastic, but you can only contribute $7,000 per year (or $8,000 if you're over 50), and if you earn too much, you're phased out entirely. Roth 401k contributions count against your $23,000 annual deferral limit. Health Savings Accounts are capped at $4,150 for individuals or $8,300 for families. Index Strategies have no statutory contribution limits—your funding level is determined by policy design, underwriting, and IRS guidelines for life insurance qualification, but it's not uncommon for business owners and high earners to fund policies with $50,000, $100,000, or more annually. This makes Index Strategies the only scalable tax-exempt accumulation vehicle for individuals who have maximized qualified plan contributions and need additional tax diversification.

Diversifying across all three buckets gives you control over your tax liability in retirement. If tax rates are low, you pull from tax-deferred accounts and pay the tax. If tax rates are high, you pull from tax-exempt accounts and pay nothing. If you need a large lump sum—maybe to buy a vacation home, fund a grandchild's education, or cover a medical expense—you can take a six-figure policy loan without triggering a taxable event, without increasing your adjusted gross income, and without affecting your Medicare premiums or Social Security taxation. This flexibility is the reason Index Strategies are a core component of sophisticated retirement plans for families who understand that tax rates are a variable, not a constant, and that controlling your tax exposure is just as important as accumulating assets.

About Steven Rosenberg & Everence Wealth

Steven Rosenberg is the Founder and Chief Wealth Strategist at Everence Wealth, a San Francisco-based independent insurance brokerage serving families across all 50 states. As an independent broker with 75+ carrier partnerships, Steven works exclusively in the client's best interest—not for any insurance company, bank, or Wall Street institution. His expertise centers on Index Strategies, tax-efficient retirement planning, and helping families bridge the retirement gap using the S&P 500 vs Index Strategy framework, the Three Tax Buckets approach, and the Zero is Your Hero philosophy. Steven is a licensed insurance professional who specializes in designing Indexed Universal Life policies, analyzing tax exposure across qualified and non-qualified accounts, and building sustainable retirement income strategies that prioritize cash flow over net worth. Everence Wealth's independence allows the firm to compare products across dozens of carriers, negotiate competitive pricing, and design strategies that align with each family's unique risk tolerance, tax situation, and legacy goals. Whether you're a business owner seeking asset protection, a high-income professional phased out of Roth contributions, or a retiree concerned about sequence-of-returns risk, Steven and the Everence Wealth team provide the institutional-grade insight and independent guidance needed to navigate complex financial decisions with confidence.

What Are the Living Benefits Available in Index Strategies?

One of the most underutilized features of Indexed Universal Life policies is the availability of living benefits—riders that allow you to access a portion of your death benefit while you're still alive if you experience a qualifying health event. These riders typically cover chronic illness (inability to perform two or more activities of daily living), critical illness (heart attack, stroke, cancer, organ transplant), and terminal illness (life expectancy of 12 to 24 months or less, depending on the carrier). When you qualify, the carrier advances a percentage of your death benefit—often 50 to 90 percent—to help cover medical expenses, long-term care costs, or income replacement during treatment and recovery.

Living benefits transform life insurance from a death-only product into a comprehensive risk management tool. Long-term care insurance has become prohibitively expensive and increasingly difficult to qualify for as you age. Standalone critical illness or disability policies often have strict definitions, limited benefit periods, and exclusions that render them ineffective when you need them most. Index Strategies with living benefit riders consolidate these protections into a single contract that also provides tax-advantaged accumulation and permanent death benefit coverage. If you never use the riders, your beneficiaries receive the full death benefit. If you do need them, you access funds when your need is greatest—during a health crisis that threatens both your wealth and your family's financial security.

We've seen families avoid Medicaid spend-down requirements, preserve home equity, and maintain dignity during end-of-life care because they had living benefits in place. These aren't abstract insurance concepts; they're real financial tools that protect Human Life Value—the economic value of your future income and the financial stability you provide to your family. Index Strategies with living benefits recognize that your most valuable asset isn't your home or your 401k; it's your ability to earn income and support your family, and any comprehensive financial plan must protect that asset against the catastrophic risks of chronic illness, critical illness, and premature death.

How Should You Structure Policy Funding and Premium Payments?

Policy funding strategy is where most IUL implementations succeed or fail, and it's why working with an experienced independent broker is essential. Indexed Universal Life policies offer flexible premium payments—you can pay the minimum required to keep the policy in force, or you can overfund up to the Modified Endowment Contract (MEC) limit to maximize cash value accumulation. The MEC limit is defined by IRS guidelines and varies based on your age, health, death benefit, and policy structure. Policies funded below the MEC limit retain full tax advantages, including tax-free policy loans. Policies that exceed the MEC limit lose the tax-free loan benefit and are taxed more like annuities.

For cash value accumulation and retirement income purposes, we typically design policies to be funded at or near the MEC limit without crossing it. This maximizes the amount of premium going into cash value relative to the death benefit, which improves long-term performance and creates the largest possible tax-exempt income stream during retirement. The death benefit is set at the minimum level required to qualify the contract as life insurance under IRS Section 7702, which ensures that all growth is tax-deferred and loans are tax-free. This design philosophy prioritizes cash value growth and tax efficiency while still maintaining permanent life insurance protection.

Premium payment duration also matters. Some families prefer to fund policies over 10 to 15 years and then let the cash value grow without additional contributions. Others prefer lifetime pay structures with lower annual premiums. The optimal approach depends on your cash flow, tax situation, and retirement timeline. If you're 50 years old and planning to retire at 65, a 10-pay or 15-pay structure concentrates funding during your peak earning years and allows cash value to compound for a decade or more before you begin taking policy loans. If you're 35 and building long-term wealth, a lifetime pay structure with moderate annual premiums might be more sustainable and allows you to adjust funding based on income fluctuations, business performance, or changing family needs.

Ready to Explore Index Strategies for Your Family?

Understanding Indexed Universal Life insurance is one thing—designing and implementing a strategy tailored to your specific tax situation, risk tolerance, and retirement goals is another. At Everence Wealth, we don't sell products off a shelf. We build custom Index Strategies using our 75+ carrier partnerships to find the most competitive crediting methods, lowest cost structures, and strongest living benefit riders available in the market. Every strategy begins with a comprehensive Financial Needs Assessment where we analyze your current tax exposure across all Three Tax Buckets, stress-test your retirement plan against volatility and longevity risk, and identify gaps in protection that could derail your family's financial security. Whether you're a business owner seeking asset protection, a high-income professional looking to diversify beyond maxed-out 401k contributions, or a retiree concerned about sequence-of-returns risk and tax liability, we'll show you exactly how Index Strategies can fit into your plan—and we'll run the math so you can make an informed decision with full transparency.

Schedule Your Financial Needs AssessmentFrequently Asked Questions About Indexed Universal Life Insurance

What is the difference between IUL and whole life insurance?

Indexed Universal Life offers flexible premiums and cash value growth linked to market index performance with a zero percent floor, while whole life insurance provides fixed premiums, guaranteed cash value growth, and dividends from the insurance company's general account. IUL allows for higher potential growth tied to the S&P 500 with downside protection, whereas whole life provides stable, predictable growth with less upside potential. Both are permanent life insurance contracts, but IUL is better suited for individuals seeking tax-advantaged growth with market participation and protection, while whole life appeals to those who prioritize guarantees, predictability, and dividend income. The choice depends on your risk tolerance, funding capacity, and whether you value growth potential or guaranteed performance.

Can I lose money in an Indexed Universal Life policy?

You cannot lose cash value due to negative market performance because of the zero percent floor, but you can lose money if policy costs exceed cash value or if you surrender the policy early with insufficient growth to cover fees. The zero percent floor protects against market losses—if the S&P 500 drops 30 percent, you're credited zero percent, not negative 30 percent. However, mortality charges, administrative fees, and rider costs are deducted from cash value, so if you underfund the policy or stop paying premiums, cash value can decline and the policy can lapse. Proper policy design, adequate funding, and long-term commitment are essential to ensuring that Index Strategies perform as intended and that costs are more than offset by tax-advantaged growth and death benefit protection.

How much does an Indexed Universal Life policy cost?

The cost of an Indexed Universal Life policy depends on your age, health, gender, death benefit amount, riders selected, and funding level, with annual premiums typically ranging from a few thousand dollars to six figures for high-net-worth individuals seeking maximum cash value accumulation. A healthy 40-year-old male might pay $10,000 to $15,000 annually for a policy designed to accumulate $500,000 to $1 million in cash value over 25 years, while a 50-year-old might pay $20,000 to $30,000 for similar results due to higher mortality costs. Costs include mortality charges that increase with age, administrative fees, and optional rider fees for living benefits, but these are disclosed upfront in the policy illustration so you know exactly what you're paying and how funding levels impact long-term performance and cash value growth.

When can I access cash value in my IUL policy?

You can access cash value through policy loans or withdrawals at any time once sufficient cash value has accumulated, typically after three to seven years of funding depending on premium levels and policy performance. Policy loans are not taxable income and do not trigger early withdrawal penalties like 401k or IRA distributions before age 59½, making IUL one of the most flexible accumulation vehicles for accessing funds during emergencies, opportunities, or planned retirement income. Loans accrue interest—usually a wash loan or low-net-cost structure where the interest charged is offset by continued crediting on the loaned amount—and they reduce the death benefit if not repaid, but they never trigger tax liability as long as the policy remains in force and does not lapse with outstanding loans exceeding basis.

Is IUL better than a 401k for retirement?

IUL is not a replacement for a 401k but a complement that addresses weaknesses in tax-deferred retirement accounts, particularly tax liability, required minimum distributions, and lack of downside protection. A 401k offers an employer match, higher annual contribution limits, and immediate tax deduction, making it the first priority for most workers, but once you've captured the match and maximized contributions, Index Strategies provide tax-exempt income, no required minimum distributions, and zero-floor protection that 401k participants don't receive. The optimal strategy is to diversify across both—fund your 401k to capture the employer match and max out contributions, then use Index Strategies to build tax-exempt cash value that provides income flexibility, estate planning benefits, and protection against future tax rate increases that erode tax-deferred account values.

What happens to my IUL policy if I stop paying premiums?

If you stop paying premiums, the policy will continue in force as long as cash value is sufficient to cover mortality and administrative costs, but if cash value is depleted, the policy will lapse and terminate unless you resume payments or elect a reduced paid-up death benefit option. Indexed Universal Life policies are flexible—there is no strict premium requirement as long as the policy has enough cash value to cover internal costs, which is why proper funding during the early years is critical to building a cash value cushion that sustains the policy during periods of low crediting or premium interruption. If the policy does lapse, you may owe taxes on any gain above your cost basis, and you lose the death benefit protection, which is why most independent brokers design policies with adequate funding buffers and monitor policy performance annually to prevent unexpected lapses.

Can I have multiple Indexed Universal Life policies?

Yes, you can own multiple Indexed Universal Life policies, and many high-net-worth families do so to diversify across carriers, access different crediting methods, and increase total death benefit and cash value accumulation beyond what a single policy can provide. Multiple policies also allow you to stagger funding timelines, test different index strategies, and segment policies for different purposes—one for retirement income, one for estate planning, one for legacy gifting. Working with an independent broker who represents 75+ carriers allows you to compare policy performance, crediting options, and cost structures across multiple companies and design a portfolio of Index Strategies that aligns with your comprehensive financial plan rather than being limited to a single carrier's products and features.

How does the annual reset feature work in IUL policies?

The annual reset feature locks in index gains at each policy anniversary and protects your new higher cash value from future market downturns, ensuring that once gains are credited, they become your new permanent floor and cannot be lost in subsequent years. If the S&P 500 is up 12 percent and you're credited 10 percent due to your cap, that 10 percent gain is locked in permanently, and the following year's crediting starts from that new higher balance with the same zero percent floor protection. This means you're always compounding from your highest previous balance, never recovering from a loss, which is the mathematical advantage that allows Index Strategies to deliver competitive long-term returns with dramatically lower risk than direct equity exposure and why Zero is Your Hero is the foundational principle of protected wealth accumulation.

This content is for educational purposes only and does not constitute financial, tax, or legal advice. Consult a licensed professional before making any financial decisions. Policy performance depends on funding levels, carrier crediting rates, market index performance, and policy costs. Past performance does not guarantee future results.